A Barrel in the Hand

Eastern liquidity rolls over, oil floating storage halves, and the case for leveraged royalty exposure sharpens. | Crown Compendium X

The Crown Compendia; An informal dispatch on markets, money and my musings. For those who want to go deeper, the links are at the bottom.

Market Musings

Gold

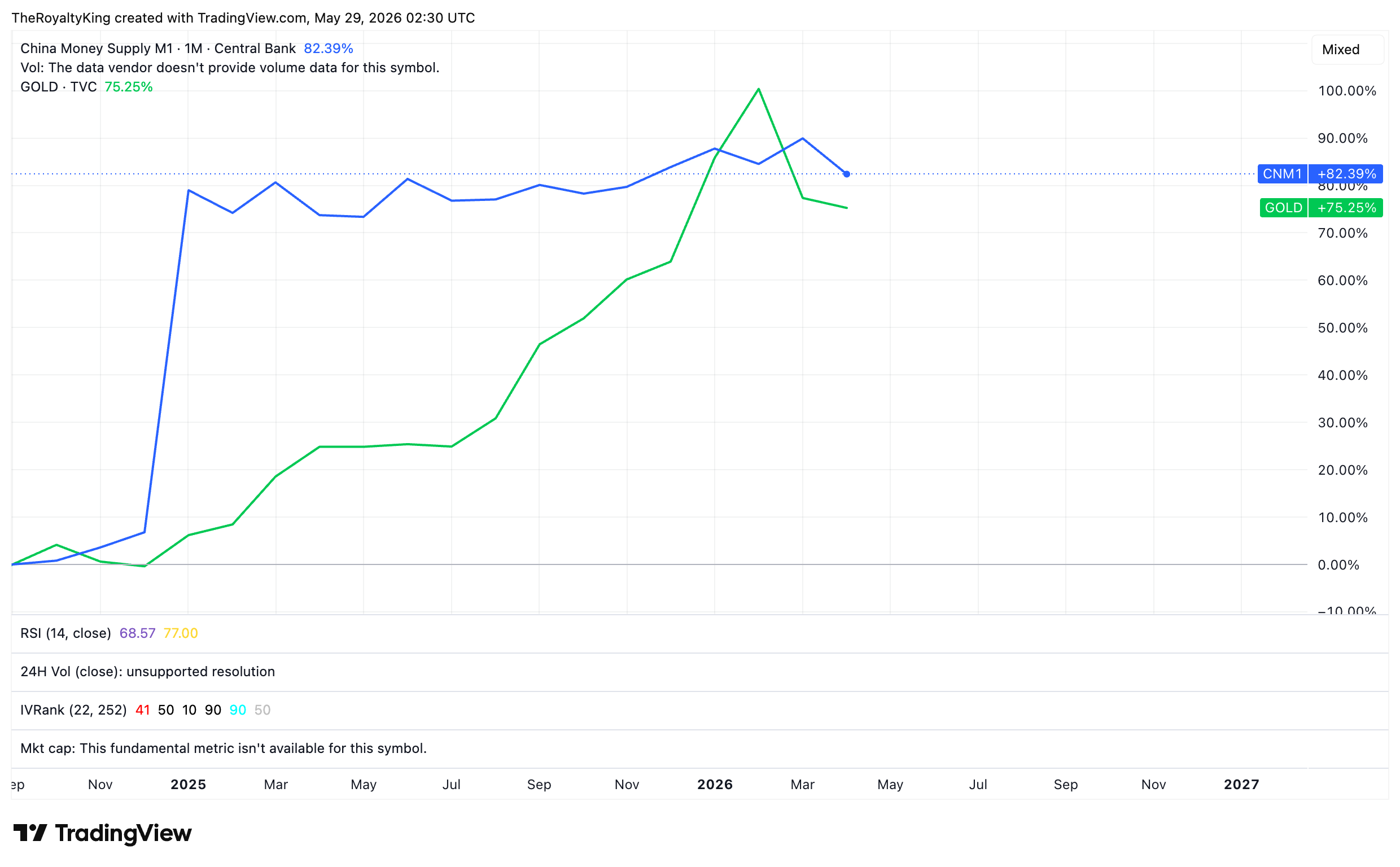

As I wrote in compendium VIII in March - It’s all about liquids and liquidity- the west appears to be experiencing liquidity pressure. Now it appears the Chinese may also be reducing the rate at which they are allowing liquidity to expand inside their economy.

This is important as I share Michael Howell’s view that eastern, not western, debasement has been doing the heavy lifting of the gold price over the past year. I won’t share any of Mike’s charts as I’m not sure what is or isn’t behind the paywall, but I encourage readers to subscribe to his work where you will see two things: The gold price following measures of Chinese liquidity and said liquidity growth now tapering after an explosive growth rate in the last 12 month.

A very crude and imperfect proxy is supplied below using Chinese M1 growth and gold bullion

Energy/Oil.

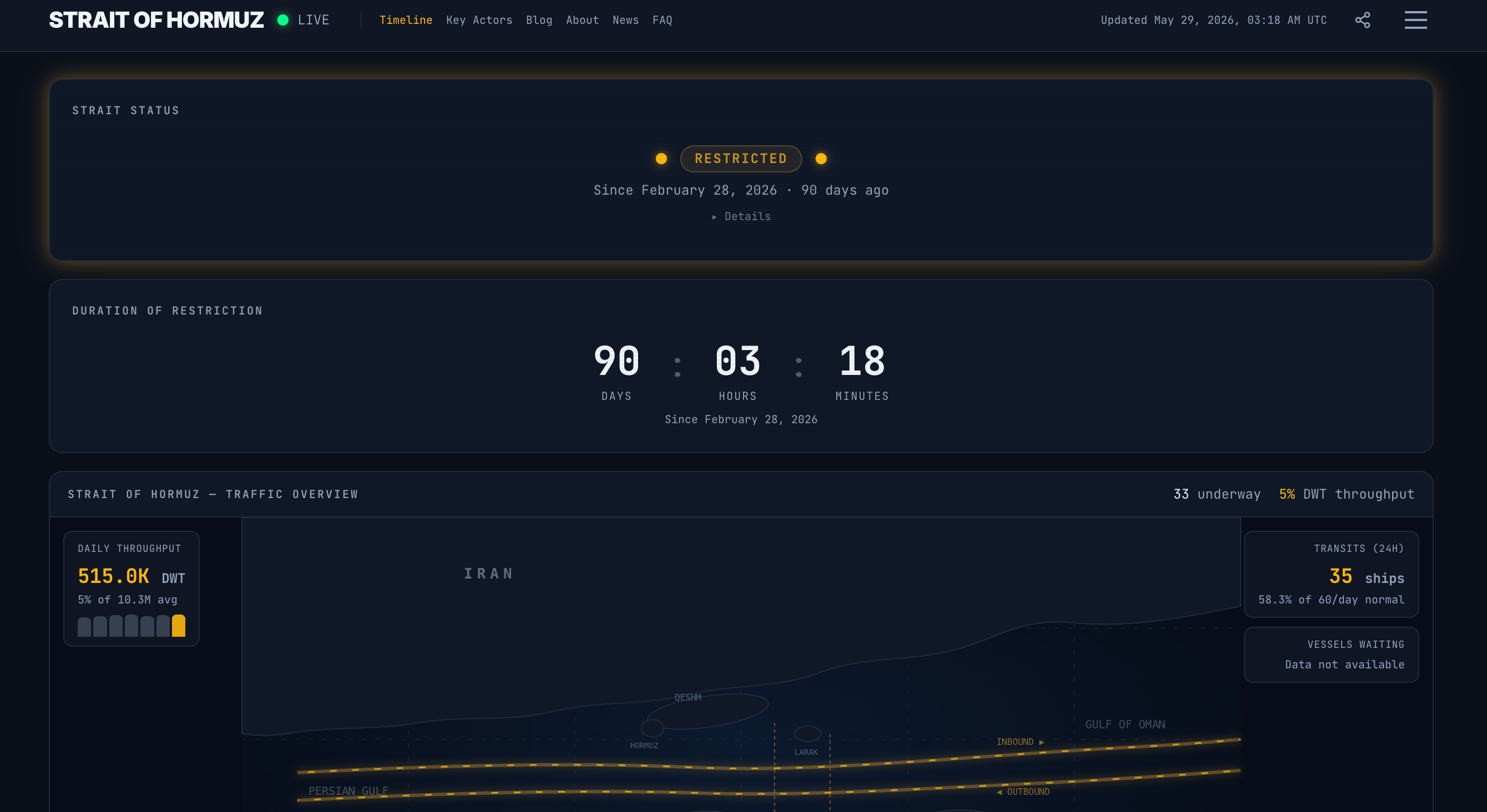

I remain astonished at the complacency of markets and the everyday citizens with regards to the potential for an energy crisis given the complete mis-match of acceptable outcomes on the lists of the three main parties involved in the current conflict in the Permian Gulf.

Assuming the below is accurate, traffic flows are currently at ~5% of normal flows. Pre-conflict flows were responsible for an estimated 20 mm BBls/day of total oil exports or circa 25% of the maritime oil trade globally.

Pre-crisis, the IEA had global oil supply at 107.4 mb/d in December 2025, with world supply projected to rise by 2.5 mb/d this year to 108.7 mb/d.

The EIA now assesses that Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively shut in 10.5 million barrels per day of crude oil production in April, and they expect shut-ins to peak at nearly 10.8 million b/d in May as storage levels reach maximum limits.

Ergo my take is that effective global production right now is roughly 97–98 mb/d compared to to 104 mb/d of demand consumption.

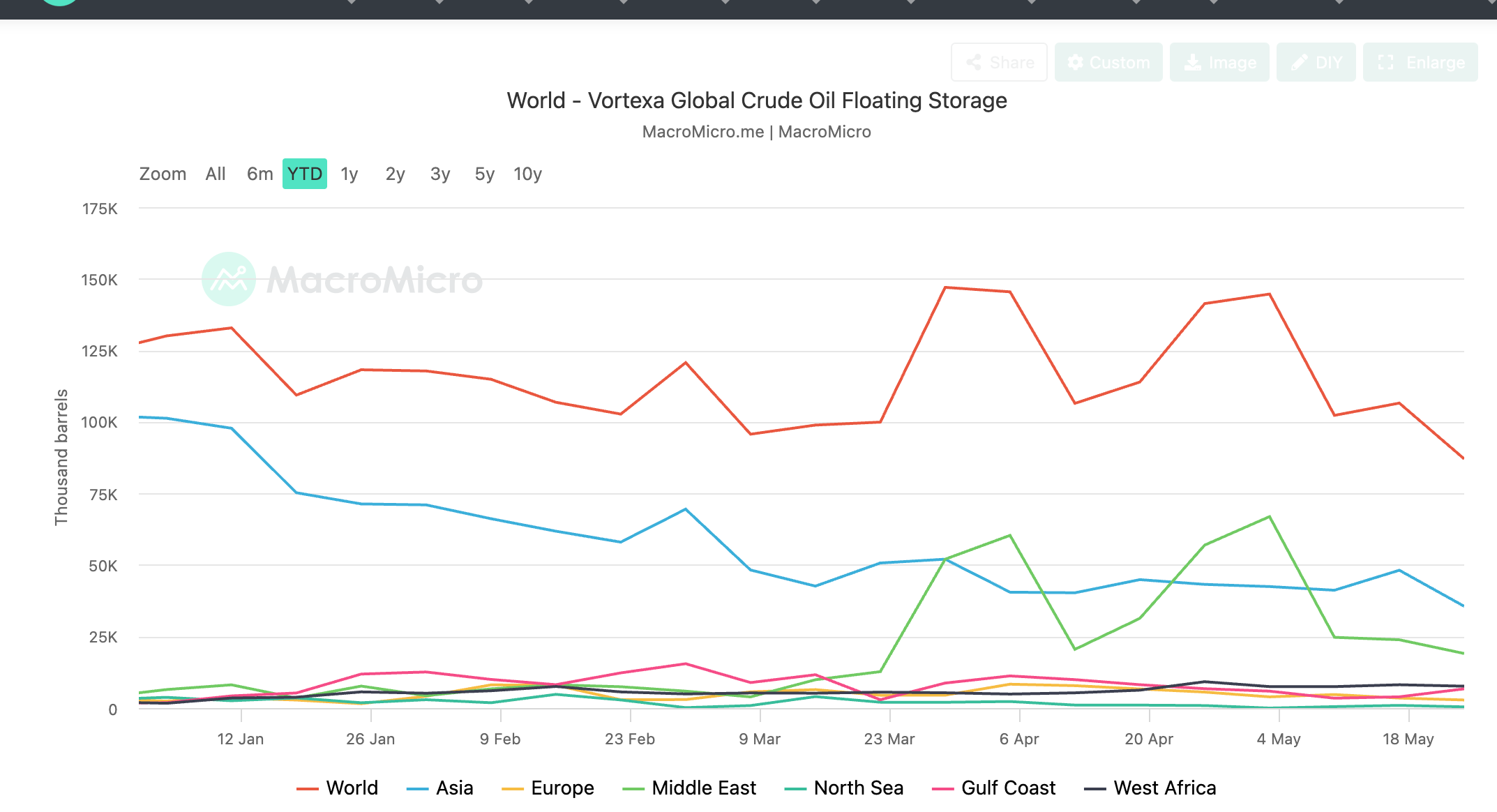

Floating storage inventory numbers appear to validate my view that markets are sleep-walking into a spot of bother given that world floating barrels are down to 87 million from 146 million in March according to the below.

I have a (highly simplified) scorecard that currently reads: ~97–98 mb/d supplied (≈108 baseline less the ~10.5 shut in) against ~102–104 demanded, producing the EIA's ~8.5 mb/d inventory draw. Against that draw, the 8.2bn barrel total stock gives a gross cushion of well over two years (~130+ weeks), but that's misleading as most is unusable working/pipeline volume, so the genuinely drawable surplus is the binding constraint and runs more like a few months before tank-bottoms and operating minimums bite.

This, I suspect is what the EIA is referring to in their below statement.

“We expect global oil inventories will fall by an average of 8.5 million b/d in the second quarter of 2026 (2Q26), keeping Brent prices around $106/b in May and June. As oil production in the Middle East rises, we expect crude oil prices to fall, dropping to an average of $89/b in 4Q26 and $79/b in 2027”.

— https://www.eia.gov/outlooks/steo/

Positioning

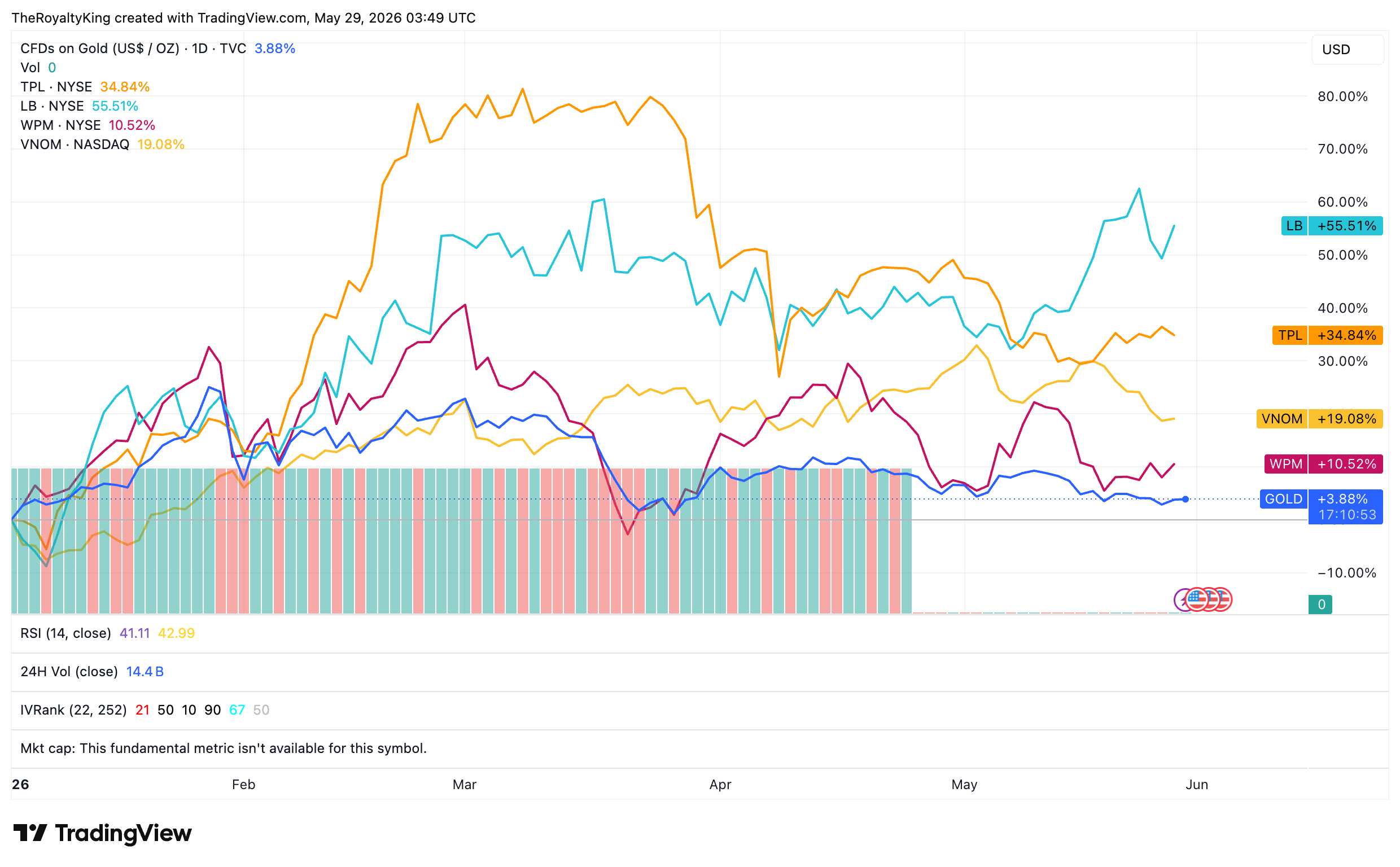

I came into 2026 with ample liquidity and at ~66% cash (which includes bullion). I enjoyed being criticised in the comments on my interview on VRIC, when I stated that I was keeping my profits in bullion and rotating the initial seed capital into more Royalty investments both in metals and energy — readers can judge from the below performance chart as to who was correct.

My main investment themes have not changed, I’m simply adding aggressively towards royalties in metals and energy via options tactics that allow me to get leveraged (sometimes 100x) exposure. Same thing with exchanges.

You can see every trade in Machina Capitalis .

One sector to which I have returned after a few years absent is the Uranium sector. My positions here I consider speculations: BOE, PEN, LOT, ASPI and YCA.

Given they are speculations they are not tracked in the Royalty King nor Croupier Collection Portfolios.

That’s a lot to consider hence I’ll end this compendium here.

Post your questions in the comments section on things you’d like me to review.

Take Care out there.

Benjamin

Great post! Idk about you but this volatility has been great for income writes on VNOM.