Bakkt Holdings (BKKT): The Digital Asset Infrastructure Play Few Are Watching

Multi-bagging within a week.. My most volatile holding to date

In every technological shift, there are those directly involved and the more indirect infrastructure providers who build the rails for everyone else.

Bakkt Holdings (NYSE: BKKT), originally incubated by another holding of mine, Intercontinental Exchange (ICE), sits squarely in that second category. While most attention in the crypto world flows toward the tokens themselves, Bakkt’s business is focused on the infrastructure layer: custody, trading, settlement, and the software APIs that connect financial institutions and fintechs to the emerging digital-asset economy.

In essence, Bakkt aims to be the regulated bridge between traditional finance and the world of tokenised assets. After years of restructuring and strategic pivots (mistakes) including divesting its consumer loyalty business, the company is now more streamlined, focused, and institution-oriented than ever before. Yet its price volatility remains extreme.

Executive Summary

Bakkt Holdings, Inc. offers software as a service and application programming interface solutions for crypto trading capabilities. The company operates Bakkt Crypto, a trading platform to purchase, sell, store, deposit, and withdraw approved crypto assets, as well as transfer supported crypto assets between a custodial wallet maintained by Bakkt Crypto and external wallets; and BakktX, an order matching technology for smart order routing for trade matching.

Business Model:

Bakkt operates as a digital-asset infrastructure platform, providing institutions and enterprises with access to crypto trading, custody, and wallet functionality through white-label API integrations. Its platform allows banks, brokers, and fintechs to embed digital-asset services without building the regulatory and technical stack from scratch.

Strategic Pivot:

The company has exited its non-core loyalty and rewards operations to concentrate on its core infrastructure and custody business (a good idea IMHO). This streamlining aligns Bakkt with a structural tailwind - the institutionalisation of crypto and the rise of tokenised assets while removing the distraction of low-margin consumer ventures.

Financials & Positioning:

While still operating at a net loss, Bakkt’s revenues have grown meaningfully as institutional volumes increase and new enterprise integrations come online. With ICE as a key shareholder and regulatory credibility built into its DNA, Bakkt is one of the few listed players positioned to capture the enterprise-grade adoption wave in digital assets.

Investment Case:

If digital assets continue their march toward mainstream financial integration from tokenised treasuries to stablecoin settlement, platforms like Bakkt stand to benefit disproportionately. The market’s current valuation reflects little confidence in that outcome, creating a potential asymmetric setup: downside limited by ICE’s involvement and regulatory moat, clean balance sheet and upside tied to the next leg of digital-asset adoption.

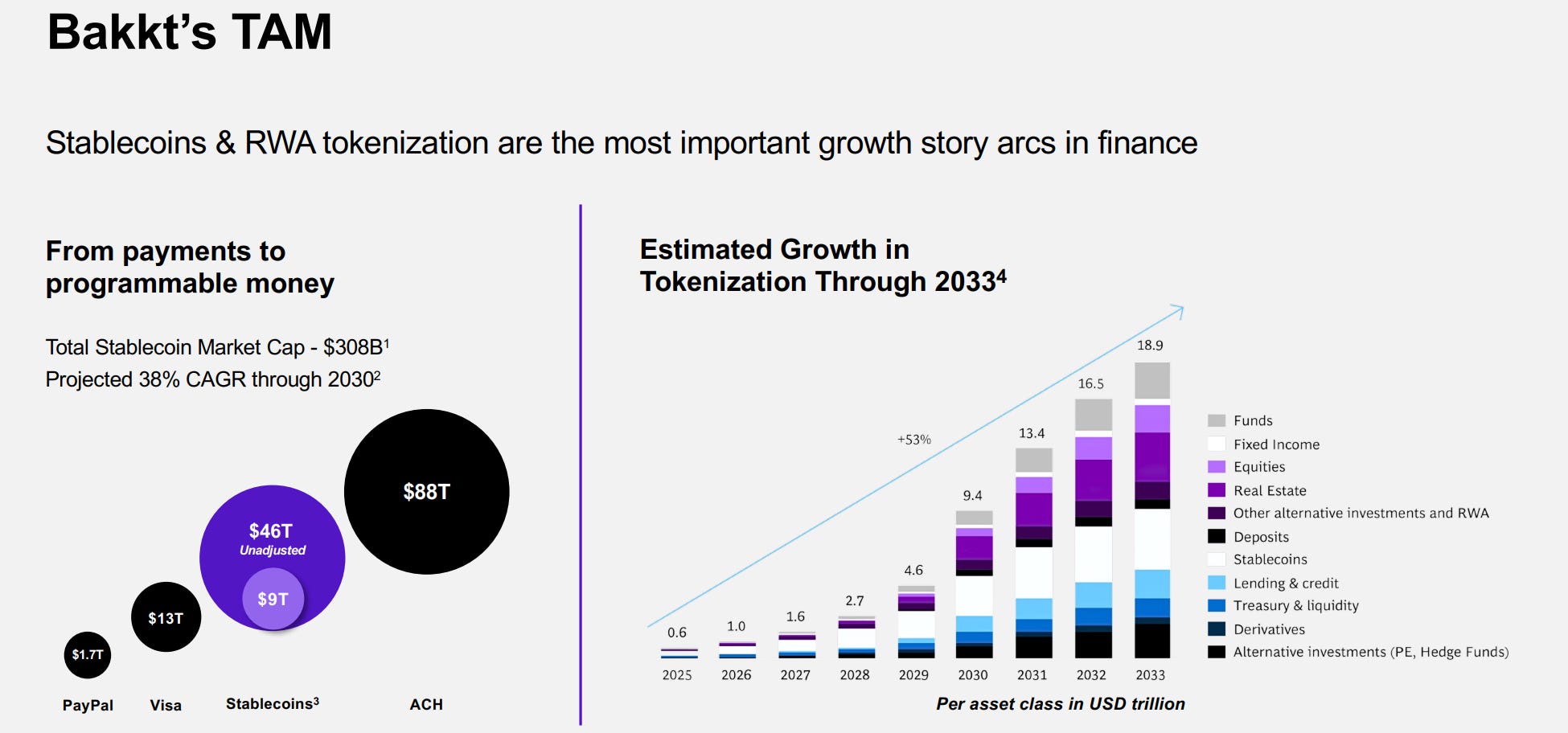

Total Addressable Market:

Bakkt is at the forefront of an entirely new asset class.

Ergo, the uncertainty as to its prospects is obviously high.

Their audacity is to be commended given the size of the prize. Bakkt is going after the tokenisation market which is, in its own way, coming for every market there is.

*Anecdote* Just the other day I received an ad in my newsfeed for funding a construction project in Argentina by buying tokenised promissory notes - I see this as an idea which will grow rapidly as it allows retail investors to invest in income producing assets, tokenised on the blockchain for as little as a $100 minimum investment.

Bkkt is looking to provide the digital infrastructure for such initiatives.

Revenue & Scale

Analysts’ estimates are all over the place for Bkkt.

As a starting point, the quarterly revenue - released yesterday - will be annualised as a starting point with various growth rates applied over a 5 year timeframe in the matrix below.

The key factor concerning the company is: at what point do they hit scale and inflect their net income positively?

Consensus currently puts this at next year, 2026.

Despite the case labels, there’s a strong case to be made that every column in the above matrix is conservative as all analysts estimate net income margins at 30%+ in 2027 and beyond. Nevertheless, this investment has always been treated as a venture investment in a new technology and thus conservative underwriting shall remain.

It’s impressive to note that even the bear case implies an IRR of 21.6% over 5 years.

Risks:

Execution risk remains high. The firm must convert partnerships into recurring transaction volume and reach profitability amid volatile crypto markets and evolving U.S. regulation. Competition from exchanges and custodians with deeper pockets is also a constant pressure, although it’s noted with interest that the Intercontinental Exchange NYSE: ICE owns 7.5% of the public float and c36% of the total shares of Bakkt.

If you missed it at less than $10, I can’t guarantee the price will return there - but I can share with premium readers a strategy that pays you a 95% return on capital to wait, along with the right to effectively buy it at that price.