Croupier for sale — 40% off.

The Croupier Collection | Urbana: 3 private exchanges & a stable-coin at 0.6× NAV

In Proud partnership with The Solstice Laboratory — the physics of markets, quantified. Read The Entropy Trap to discover what physics knows the economics doesn’t.

How does a shell company with gold mining claims become a publicly-listed investment fund whose founder enjoyed the “trade of a generation” — witnessing his privately held exchange seats convert into publicly listed shares of some of the most desired assets in the world?

That is the story of URBANA CORP [TSE: URB & URB.A] and its founder and talisman Thomas S. Caldwell. In 2002 Caldwell, the former governor of the Toronto Stock Exchange (TSX) and 2nd largest owner of the New York Stock Exchange (NYSE) turned the shell corp — Macho River Gold Mines Ltd— into a public vehicle. His motive was simple: exchanges were converting from members' clubs into for-profit corporations and were the great toll-booths of modern finance. He rode the demutualisation wave through New York, London, Toronto and Chicago. Two decades on, Urbana no longer just owns exchanges — it builds them.

Side-note: Urbana still owns the original gold mining claims — 44 of them to be exact.

Mr Caldwell remains the chairman of the Canadian Stock Exchange (CSE), the crown jewel & largest holding in Urbana’s enviable list of assets. And if you’ve never heard of the CSE, that’s because its shares are not publicly available — the only way to acquire them is on a look-through basis by buying Urbana’s stock.

Urbana is almost certainly the most interesting and obscure holding in The Croupier Collection.

The Croupier Collection, it will be recalled, is a portfolio I created for long-term investing in financial exchanges, brokerages & asset managers. The underlying rationale is available via the original white paper I wrote alongside Hugo Navarro Navarro here:

Urbana is a rare coincidence of two factors I look for in my investments: owner-operators and a superior underlying business model.

The Caldwells, Thomas & son Brendan, jointly own 55% of the stock and their holdings mainly consist of arguably the greatest business model there is: securities exchanges.

What makes businesses like exchanges and royalties so great as investments?

The market in its myopia routinely overlooks the value of a business with the ability to originate an asset and walk it through a value-accretion process. Even better when this takes place inside a vertically integrated structure the company owns and controls as it can lead to truly superlative returns. In royalty Co.s, this prospect generation; where the royalty company stakes the land, does the early exploration, then sells the deposit to a JV development partner while retaining a Net Smelter Return (NSR) for itself. The company manufactures the royalty rather than buying it.

A constructive example is that of Altius minerals who sold a 1% royalty on Silicon/Merlin to a Franco-Nevada subsidiary for $275M and kept a further 0.5% — implying ~$412M for the whole royalty it had generated for roughly $300,000. That’s ~1,375x, or 106% ARR.

Urbana does a similar thing by incubating exchanges — staking, building and then helping them go public as seen with the likes of MIAX. A prospect generator manufactures royalties; Urbana manufactures exchanges.

It’s easy to overlook Urbana’s ability to develop quality private businesses and bring them up the value chain and most market participants do. Urbana’s track record includes:

CSE (CNSX): ~$14.5M cost → ~$100.7M fair value = ~6.9x

Blue Ocean: ~$13.6M cost → ~$76M fair value = ~5.6x, a ~459% gain

These are the private valuations as agreed by their auditors, yet one can expect further gains from the multiple expansion they occurs when a business goes from private to public.

To give an example of how mis-priced the private assets might be, another holding, TETRA, had its valuation reviewed for financing purposes and as a result was marked up such that its new valuation added 45c worth to the entire stock’s NAV.

Incredibly, such quality is available today for purchase at an estimated 43% discount to its fair value. Upon closer inspection, the discount may be even greater if one is willing to do the valuation work on the potential of the private assets held.

Naturally the question arises: How is it that such quality is available at such a low price?

This is likely due to half of their assets being private and hence analysts are clueless as to how to value them.

Additionally, Urbana is considered — perhaps unfairly — as a passive holding company, with such a stigma often penalizing an investment firm and leading to their stock trading at a discount.

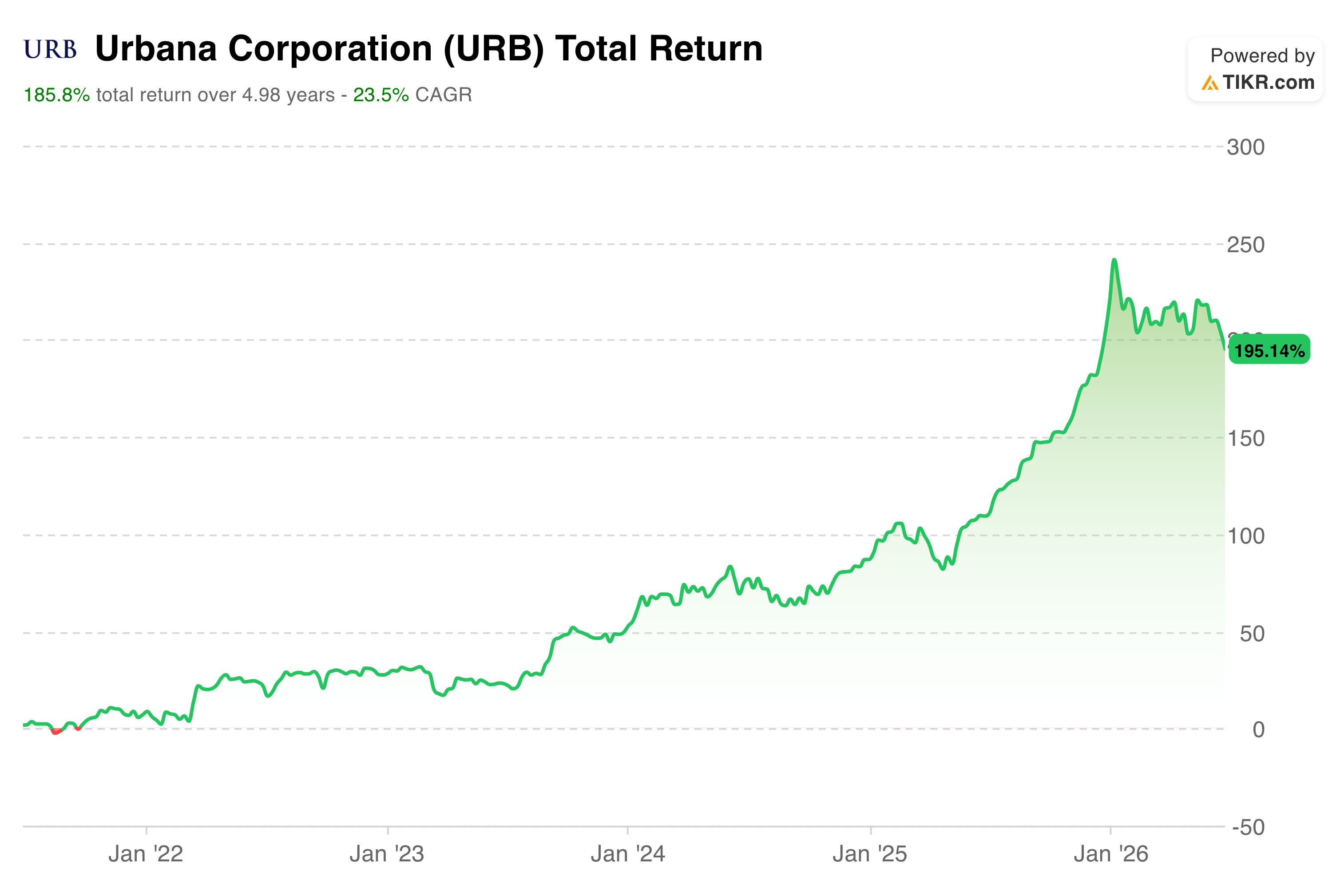

Both the aforementioned factors are likely to lead to Urbana trading at a discount to NAV for as long as it’s considered a closed-ended investment vehicle. However, this doesn’t impact URB’s ability to grow in the slightest as is supported by their 5 year track record of returning investors 23.5% CAGR.

Add in a new buyback program and the chance for several windfall opportunities from the future IPOs of the private holdings and the case for URB becoming the number one holding in the croupier collection is compelling.

So, what’s it worth today? And what could it be worth in the future?

Let’s find out.