How Rick Rule Taught Me To Find Net-Nets

Here are my notes from running the playbook he taught me.

“A cash flow positive net-net is a gift from God. It's like a bond with a negative cost."

—Rick Rule

Yesterday I enjoyed another insightful conversation with a mentor of mine, the legendary Rick Rule. In my podcasts I always aspire to provide novel themes and questions for my guest as I see no purpose in rehashing the basic themes that have already been asked of them - the internet abounds with this sort of content, which imho is more designed to eek out views thanks to the guest’s name rather than elicit truly meaningful insights.

I humbly believe I may have elucidated some themes which, to my knowledge, are not available in any of the many publicly available conversations Rick has generously agree to partake in. One standout segment in particular is where Rick teaches me step-by-step how to embark on a screening process to find a cashflow positive net-nets.

A net-net stock is a company valued by the market at less than its Net Current Asset Value (NCAV), or current assets minus total liabilities. Net-Net investing was pioneered by Benjamin Graham — the father of modern value investing— who was a mentor to Warren Buffet and looked for opportunities trading for <2/3 their NCAV.

As such, in today’s piece I’m running the playbook taught to me first hand by ‘Uncle Rick’ and sharing my notes with you fine folk.

If you haven’t listened to our conversation yet - see the link below, the feedback so far has been pleasing.

Firstly, some brief notes on my history investing in net-nets (and those discount-to-liquidation-value type plays):

$GEO group - Prison/REIT traded at large discount to replacement cost throughout 2023 when I bought shares in the $7 range. Catalyst was a change in corporate structure (from REIT to corporation) which ceased the dividend but allowed them to pay down debt. The stock price reached a high of $35.10 in 2025.

Transocean, Valaris et. al. Not all true net-nets for the sticklers would say the balance sheet would have disqualified them as such. Nonetheless they traded at ridiculous discounts to book value and has ample liquidity. I was vocal (and likely obnoxious) in my announcements of buying LEAPS on RIG coming out of covid in 2021 with the stock <$2. VAL in the $20s was obvious, although it tested everyone’s patience.

NNDM - Disaster! Here I learned that at least when people rob you on the streets there exists some kind of recourse. Unfortunately in the stock market not so much. NNDM raised over $1Billion throughout the 2020-21 period as a SPAC ostensibly to roll up 3D printing and tech firms. The stock had something like $300 mm more in negative EV i.e; more cash than the price of the company, yet here I learned firsthand that bad management can derail even net-net opportunities. I sold at a ~30% loss a few years ago and, out of curiosity, I see that today it trades lower still; it’s still at a negative EV, with $400mm in cash yet in 2025 off a revenue of $100mm and I note with horror that management saw fit for SGA expenses to be $80 mm!!

You can avoid a similar experience by remembering the following from Rick in the podcast:

"It isn't enough just to do net nets. You have to do net nets that are either cash flow positive, which is to say they aren't declining, they aren't decreasing one net, or else are or about to be in liquidation so that you could realize it before they cannibalize themselves.”

Now just in case you’re wondering — no, I’m not changing the focus of this publication to net-nets— precious few exist in markets these days with the exception of perhaps Japan.

"If I wasn't 73 years of age, if you dialled me back to a 20 or 21 year old securities analyst working for Peter Cundill, he almost certainly would have assigned me to Japan and Korea."

So today I’m going to run the instructions from Uncle Rick for those who don’t have access to a Bloomberg terminal.

So, let’s begin.

“Anybody in your audience who has access to S&P Intelligence or Bloomberg can run a screen. Negative working capital plus free cashflow. You won't have to go looking for those companies, they'll pop up. Once you get your shopping list, what Bloomberg and S&P won't do for you is point out the unexploded bombs on their balance sheet. You'll have to do that for yourself.”

Using my TIKR terminal, I screened for the following across Korea/Japan:

Market Cap < 0.67 × NCAV + MC >$15mm USD

FCF (TTM) > 0

Bomb Defusal (manual review - sorry - no shortcut)

Many names came up, not all of which were viable and I’ll leave it to you to peruse the list, but let’s take one such example and review it - just for fun.

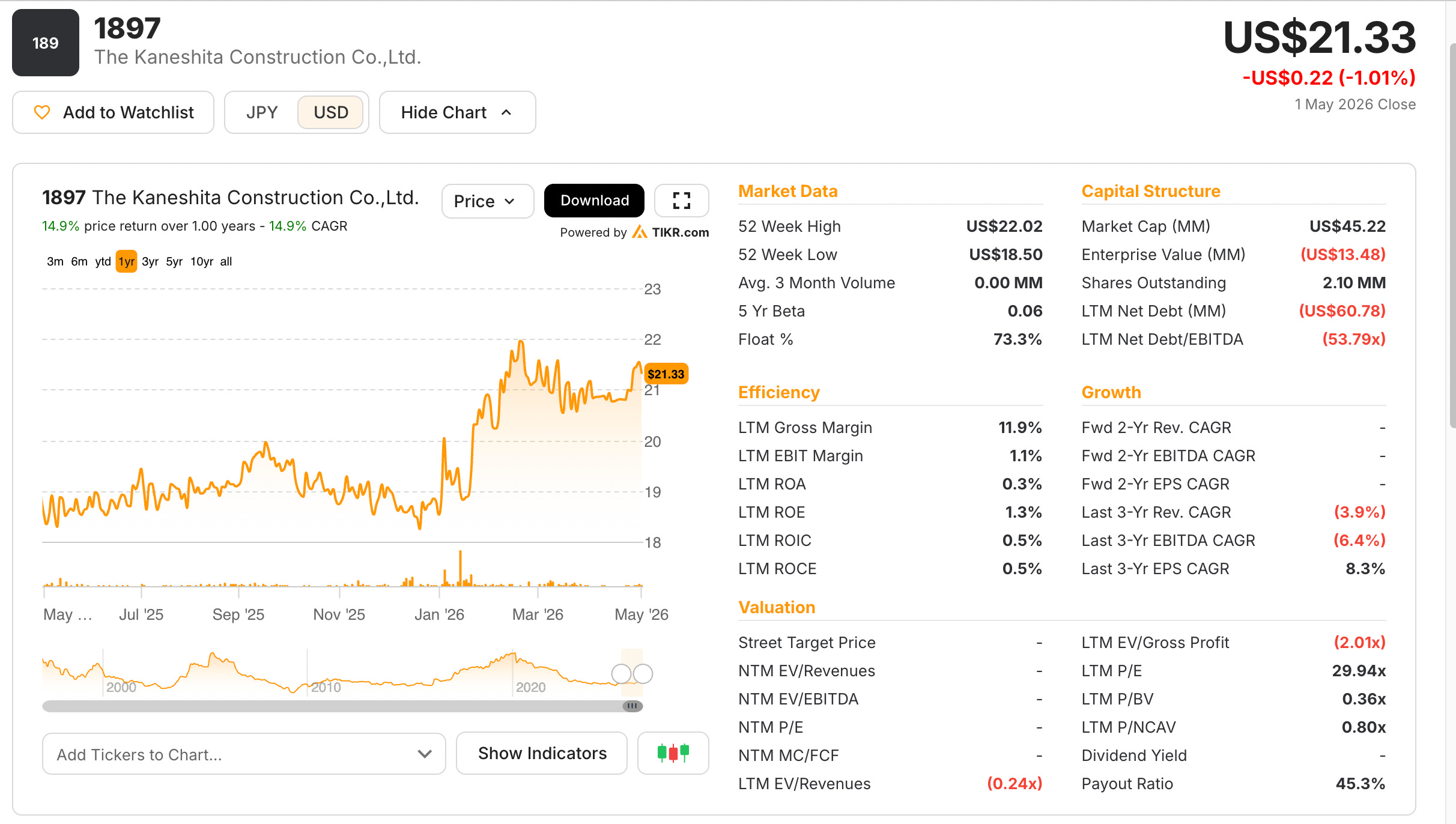

The Kaneshita Construction Co. Ltd. TSE: 1897

Executive Summary: The Kaneshita Construction Co.,Ltd. provides design, planning, survey, supervision, investigation, and construction civil engineering and architectural works in Japan. The company undertakes civil engineering works, including roads, tunnels, bridges, rivers, and water and sewage facilities, as well as road pavement, erosion control, port construction, and landscaping and construction works.

Why it passes: Kaneshita is a textbook net-net. The market has priced in permanent operating failure as the stock trades at 0.36× BV with a negative enterprise value of −¥11.5B. If one acquires the business at its market cap today, one immediately holds more than twice the cash you paid. The 5-year average FCF yield of ~9% satisfies the cash consideration. Zero debt satisfies the balance sheet question. A century of operating history suggests the "death by incompetence" scenario is unlikely, although they made a terrible unforced error in attempting to enter the restaurant business around COVID. This type of style-drift is something to keep an eye on, hopefully the lesson was learned.

Bombs to defuse: (1) Management quality (2) Insider/friendly shareholder control at 40–50% reduces involuntary delisting risk but also reduces pressure for capital returns. (3) Construction company balance sheets carry large receivables tied to progress payments. Those invoices better be reliable. (4) Land on books the most interesting aspect in my eyes, accounted for at historical cost (pre-1935) and likely substantially undervalued, which is a bonus, but who’s to say they realise this value?

The Royalty King’s Remarks

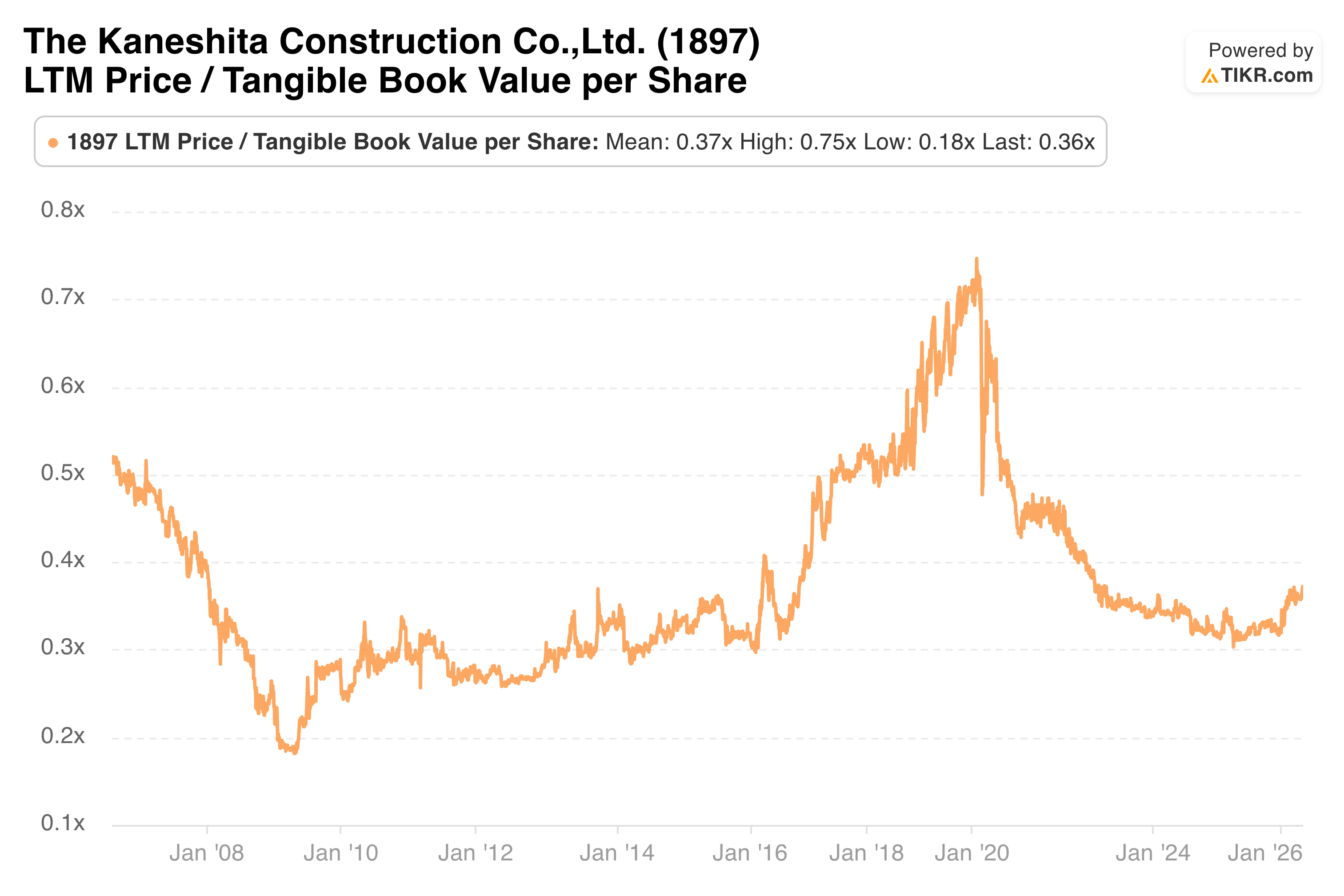

An investor in Kaneshita today, anticipating a re-rating merely to the stated book value is underwriting a potential 3x. That’s easy to grasp. What’s far more difficult is anticipating when Japanese equity multiples will revert to what westerners might consider fair value, say, 1xBV. You see the market multiple for Kaneshita has been this way for over a decade (below). One needs to be confident that the recent changes to Japanese securities law and the cultural incentives being encouraged in Japan for corporate transparency continue to permeate a market that has been dormant for coming on 4 decades. The other side of the coin is that at 9% FCF yield, one can afford to be patient in waiting patiently (and hopefully) for the value to be unlocked. In what would be an incredible plot twist, the hidden asset of the land owned might, for any number of reasons, be realised and drive a massive re-valuation of the balance sheet assets. However given the portion of shares and power held by insiders (and here lies the rub with Japanese equities) there’s little chance for an activist to catalyze such an outcome. At least in the near term.

Hopefully you enjoyed this detour and diversion.

If so, be sure to spread the word.

And before I forget - don’t miss out on Uncle Rick’s symposium for 2026.

All the best.

Benjamin