It’s Elemental: The Royalty Merger That Changes the Game

Inside the EMX–Elemental merger and why Tether’s $100 million bet signals a new chapter in royalty economics

The landscape of the precious metals royalties has changed considerably over the last 12 months.

In July of last year I wrote that there was a

“Vast chasm in valuation between the biggest and the smallest and the gap closes via either via re-rating or takeover”

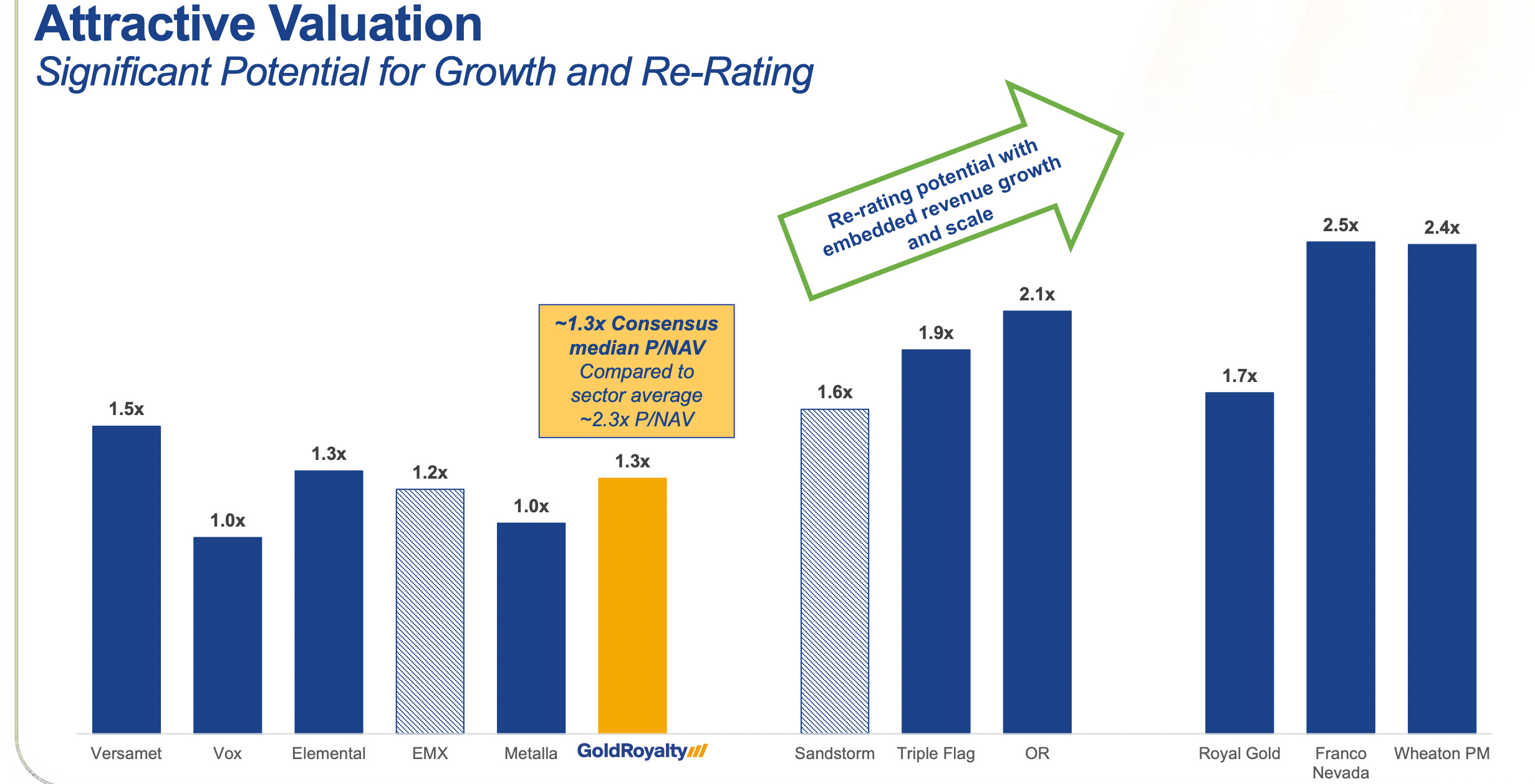

The below chart illustrates just how bifurcated the royalty space was in terms of the multiples paid for the larger caps Vs smaller caps.

What was lacking at the time was an attractive, solid option in the middle-ground, say, $1Billion+ in Market Cap.

Since then we have witnessed a significant uptick in M&A in the space, one of which will be the focus of today’s piece given it involves one of my investments - Elemental Altus, TSX: ELE.

A Quiet Consolidation

On September 4, 2025, ELE announced a merger with EMX Royalty Corporation (EMX) with the pro forma company to go under the name Elemental Royalty Corp.

Upon the necessary approvals, ELE will acquire all of the share of EMX with the help of a $100 million placement purchase from its strategic shareholder Tether which will leave the new merger Co. unlevered.

Some key points:

EMX shareholders receive 0.2822 Elemental Altus shares per EMX share (ELE completed a 10-1 share consolidation just prior)

Consideration implies ~US$456M equity value for EMX; premium of ~9.8% vs open market and ~21.5% vs 20-day VWAP at announcement.

Post-close ownership: ~51% Elemental Altus holders / ~49% former EMX holders (inclusive of the Tether placement).

Targeted cloase is Q4 2025 subject to approvals.

The New Pro Forma

As of today the Pro-forma company is estimated to come in at:

Market cap ~US$933M

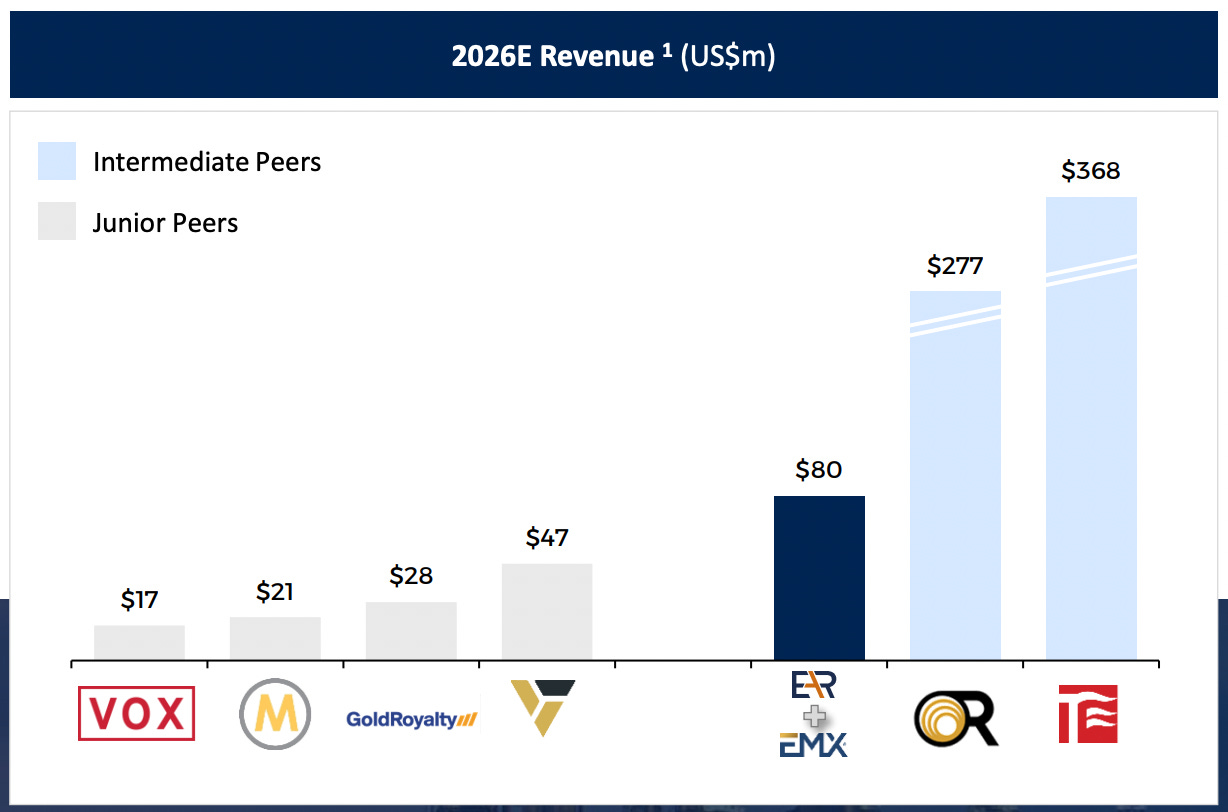

Cash ~US$48M Hence EV ~US$875M, with a run-rate revenue of ~$80 Million.

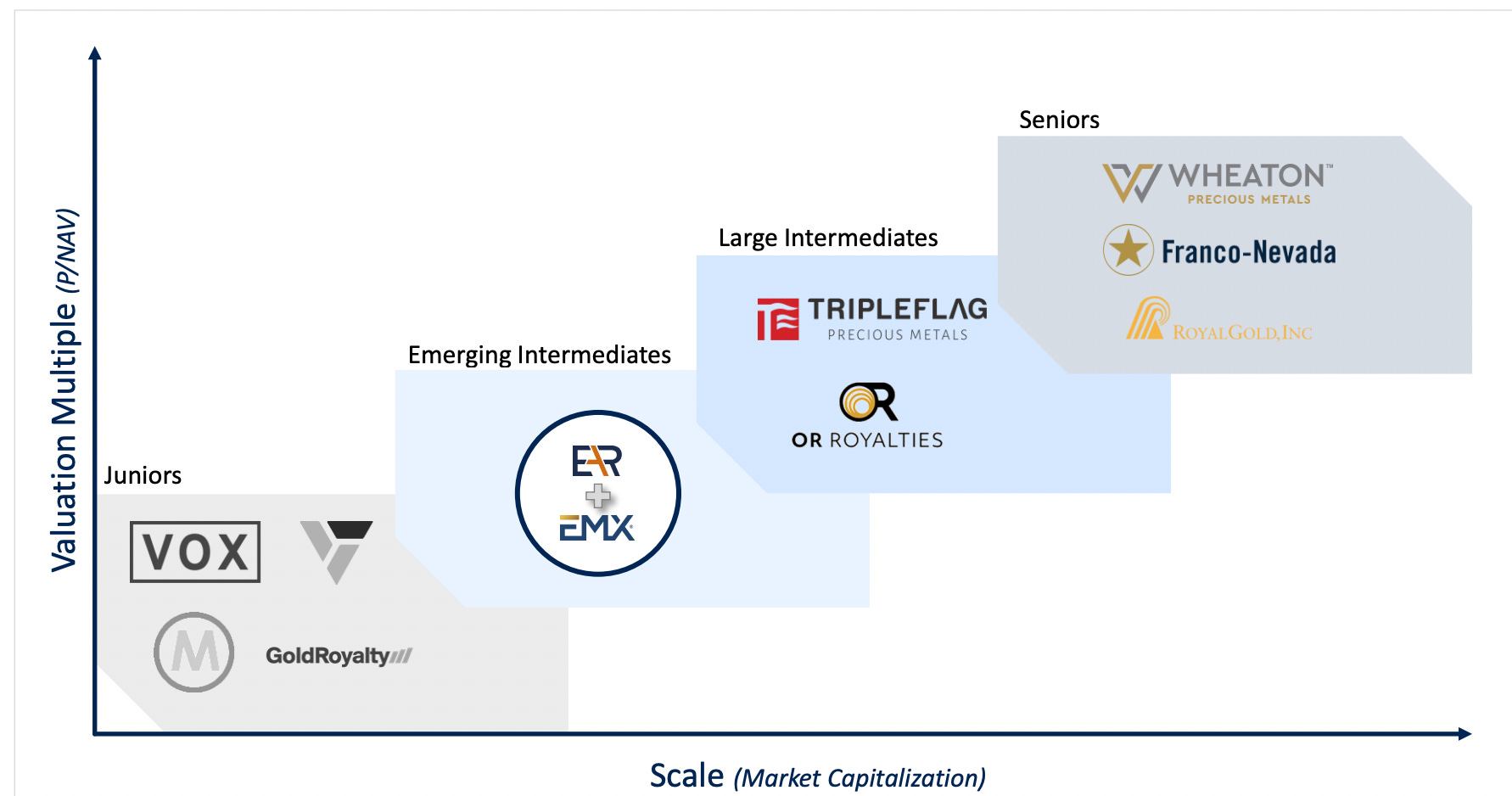

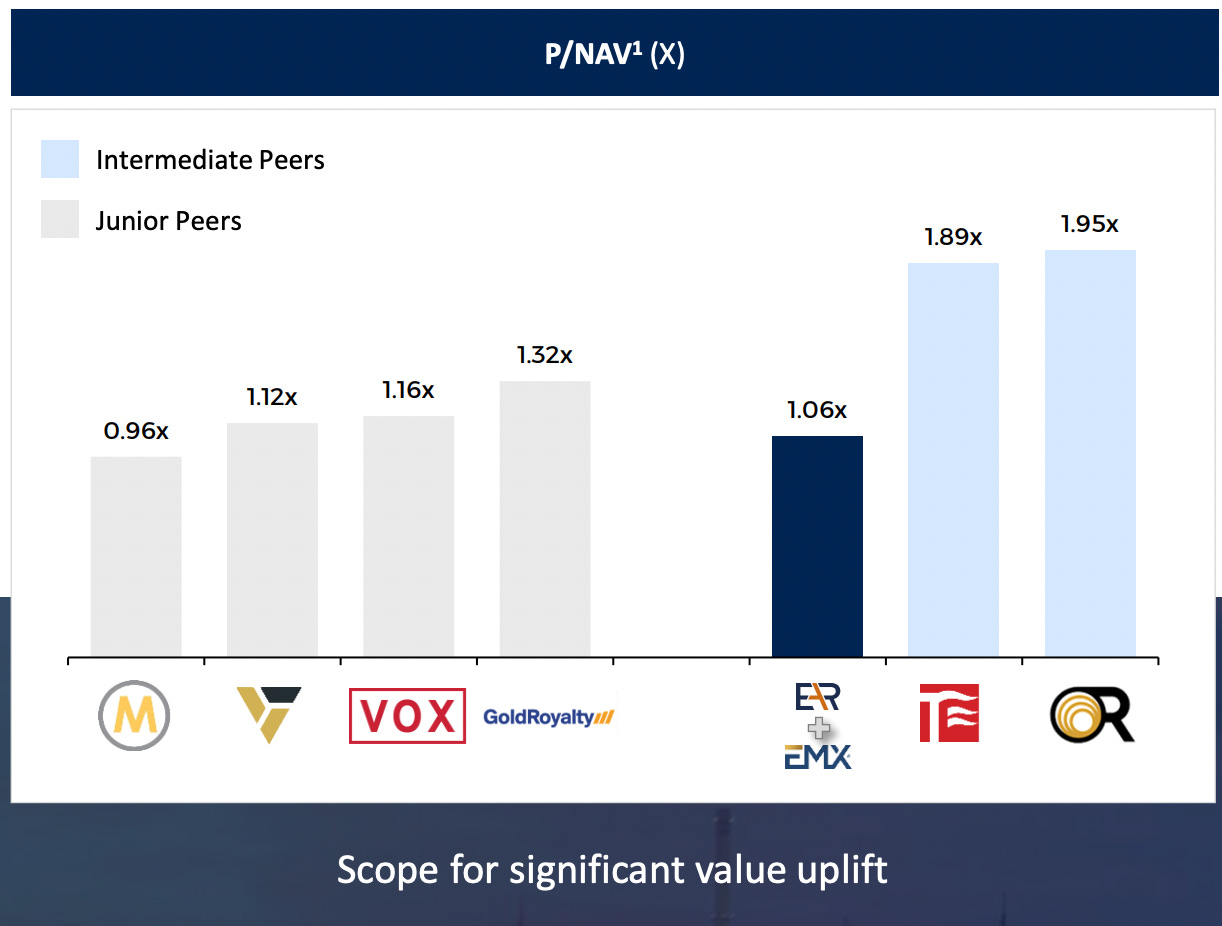

You can see from the below how this catapults the combine into the next tier of the Royalty & Streaming space.

Interesting, the merger so far has not improved the market multiple for the bigger entity which may signal opportunity.

Valuation

So how am I viewing the pro forma through a value lens?

For Royalties I’m certainly a ‘NAV’ guy but before I get to my preferred method using a production estimate/price matrix let me humour some of the spreadsheeters.

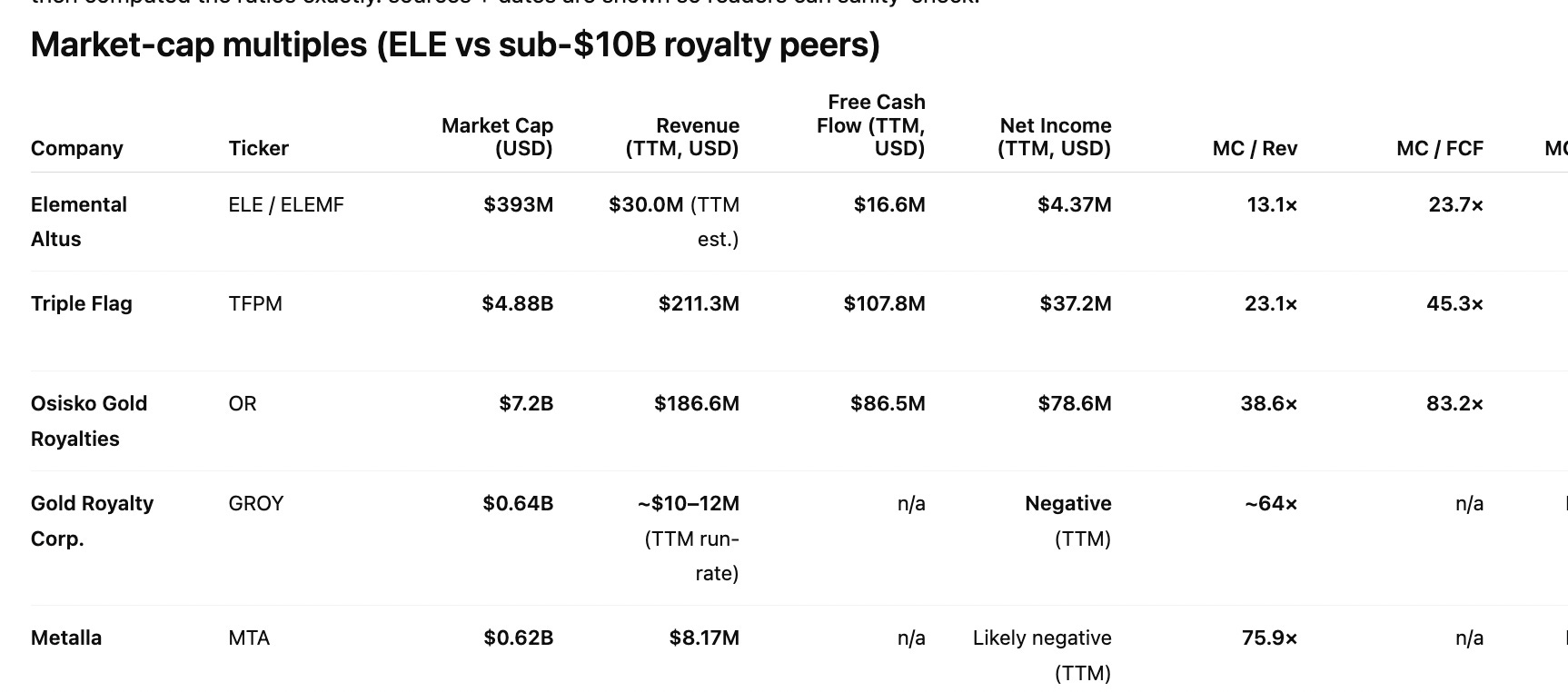

Using the numbers above we have confidence of a Market Cap to Revenue multiple of 11.6x. For Royalties this is actually fairly low.

Let’s consider the peer group:

Triple Flag trades at 15x and 25x Free cash flow (FCF) while OR Royalties trades at 20x Revenue and 29x FCF. Mind you, this is using analysts’ NTW estimates and they are usually far more conservative in their underwriting of expected commodity prices than I.

In terms of pipeline OR holds 195 Royalty contracts on its books, 21 of which are producing which to me is not a particularly compelling reason for it to trade at more than 6x the Market Cap of the new Elemental Royalty Corp albeit they hold an enviable royalty on Canadian Malartic.

Elemental Royalty now also has a more expansive global footprint.

Looking out to 2026 and applying a very reasonable 65% free cashflow margin to its expected $80 million in revenue implies $52 million in free cash flow and ergo an investor today is paying an EV/FCF ‘26 of <17x.

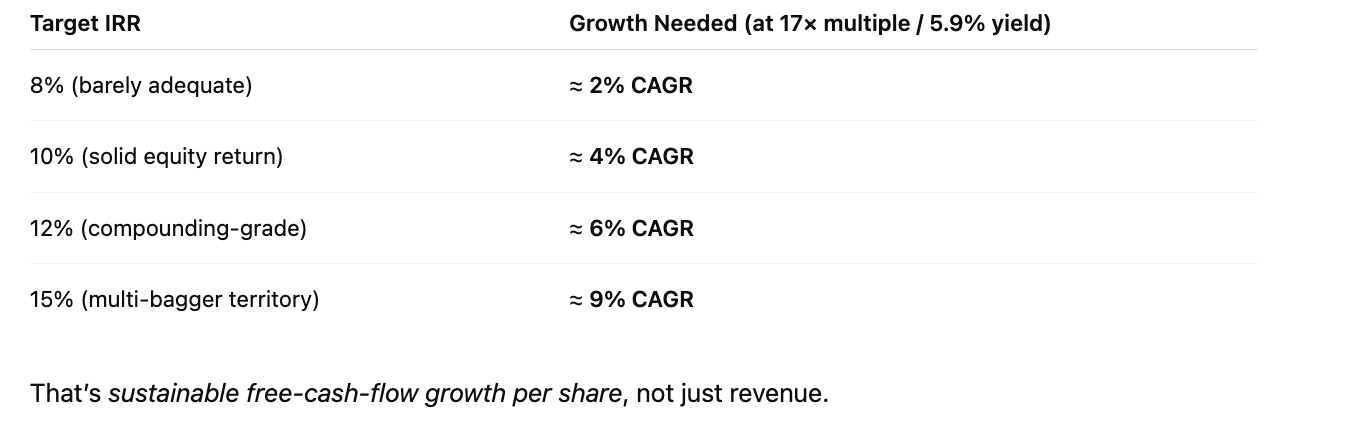

So, before going any further, it might be worth pondering the arithmetic around what kind of compounded annual growth rate (CAGR) might be needed to justify such a price.

Each investor will have varying return requirements (IRR), typically acceptable IRRs have been outlined below, along with their respective required growth rates in the company’s cash flows in order to satisfy the desired return.

Paying 17× EV/FCF gives you a 5.9% starting yield. To earn an attractive equity-style return, you need at least ~6–9% annual FCF/share growth, or a rerating catalyst.

So are the growth rates required reasonable?

According to form - Absolutely!

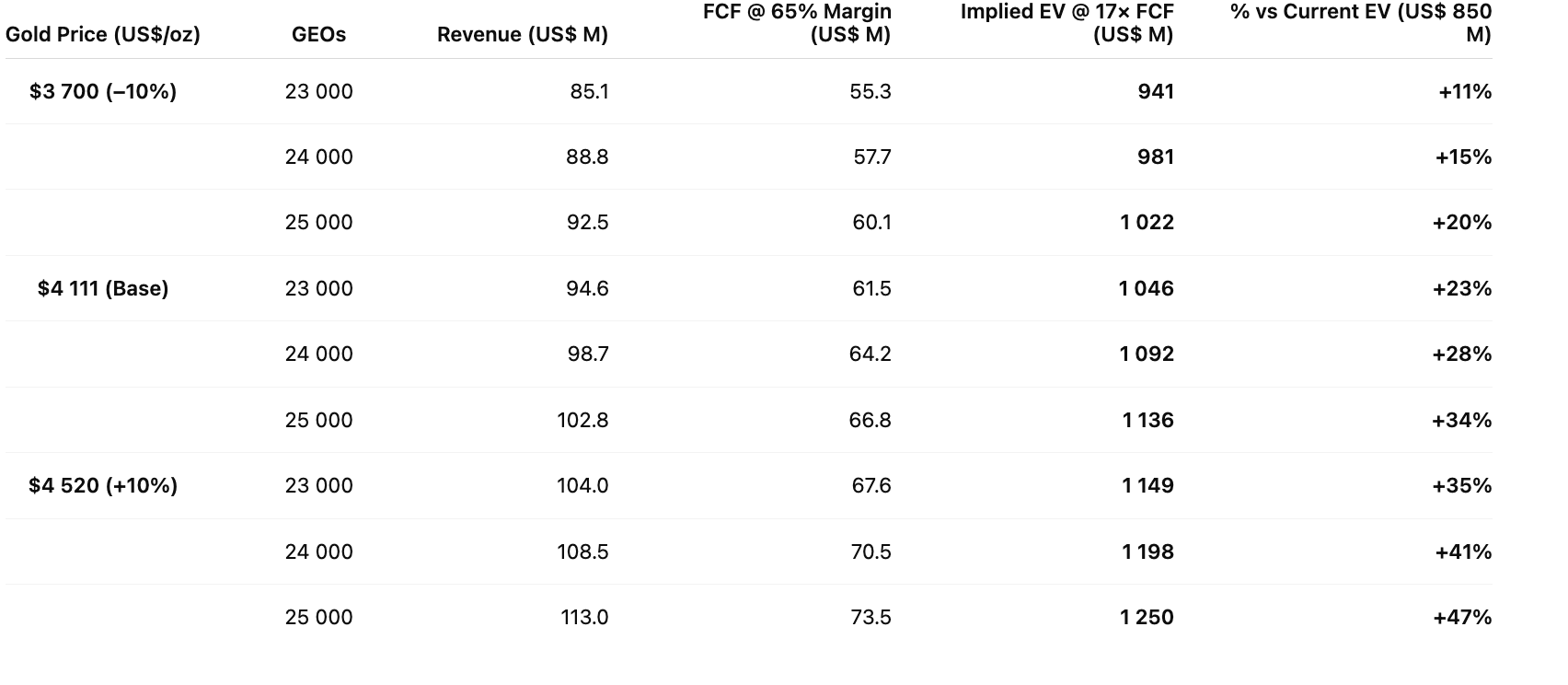

Asset Value & Production Matrix

Joining the two companies production estimates for 2026 suggests ~ 22 - 25,000 GEO.

For context, this compares favourably to one of my favourite companies GROY who aren’t expecting that much for some years yet, however they currently trade at half the Market Cap of the pro forma, which also has more producing projects.

Uncle Rick taught me to be an NPV investor in this space, constructing a matrix of different cases for production, margin and commodity prices. I’ve taken the liberty of providing such an outcome below for 2026 only and comparing it to the pro forma EV to gauge potential upside.

The matrix has obviously been kept condensed for brevity’s sake, but you get the general idea. Analysts and the company itself appears to be underwriting guidance at a gold price that’s currently well under spot. It’s likely I’ve been overly bullish in my FCF margin but as the various projects ramp up it should be no issue as this is a typical margin for the business model.

On the other hand, many major institutions such as JP Morgan et al are forecasting $5k Gold within 12 months so perhaps the margins might arrive sooner rather than later.

This post has been made free in the hope you’ll get enough value to re-stack and consider subscribing.

Thanks a lot.

Until next time,

Take Care.

Benjamin.

Ready to Take Your ROI to the Next Level?

Upgrade to premium membership and gain exclusive access to:

The ROI Club: Dedicated to the art of Return On Investment

My investment research that has delivered multi-baggers returns.

Tired of playing by someone else’s rules?

The Maverick Life Mastermind will show you how I build borderless income, multiple passports, and a sovereign life without bosses, clients, or permission.

I’ll also bring in the brightest minds in international living to showcase how I’ve acquired multiple passports and residencies across 3 continents.

👉 Join the Waitlist Now and make money flow wherever you are 🌍

Generating Location-Independent Income in order to live:

Where you want

When you want

With whom you want

Doing what you want