MIAX IPO: When an Exchange Lists Itself

The Inflation Beneficiaries Hiding in Plain Sight - A rare early entry into the gate-keepers of Stock markets.

“Miami is the place in the United States where the future has come first.”

— Joan Didion

Literally in the case of the recent IPO of Miami International Holdings Inc. who’s recent IPO brings with it access to its proprietary futures trading contracts.

Premium subscribers know I’ve held MIAX shares indirectly through a privately held partnership, shares in which can in turn be purchased via what I still consider to be the number one investment I own - outlined in this piece:

I was super excited upon the completion of the IPO as it crystallises a massive valuation re-rating for the indirect shares I’ve held in the company.

The Uncommon Occurrence of Exchange IPOs

Exchange companies themselves undertaking an initial public offering (IPO) is quite uncommon. In the last 15 years there has only been two other IPOs of traditional exchange businesses being: CBOE in 2010 and BATS in 2016 - which was later acquired by CBOE. (Coinbase’s entry to the public markets in 2021 was technically a direct listing).

Financial exchanges should be thought of as in the grand architecture of stock market transactions. I consider them financial infrastructure, akin to the role played by the house in a casino.

Their assets are regulatory licenses, technological rails and participant networks that, once built, tend to harden into semi-permanent tollbooths.

For that reason, when a privately held exchange operator goes public, the wise investor should pause and reflect.

A Brief History

MIAX’s was formed in 2007, with a vision to create a modern exchange at a time when incumbents still held near-total dominance. The founders bet that superior technology i.e: faster matching engines, lower latency, and cost efficiency could carve out a place even in a crowded market.

MIAX secured its first exchange license in 2012, a milestone that allowed it to operate in U.S. options, which proved to be key. From there, growth was incremental but steady:

2017: Acquired the Minneapolis Grain Exchange, later rebranded as the MIAX Futures Exchange.

2019–2021: Launched additional options venues, building redundancy and choice for market participants.

2020: Added MIAX Pearl Equities, entering the U.S. equities market.

2022: Extended internationally through ownership of the Bermuda Stock Exchange and The International Stock Exchange (TISE).

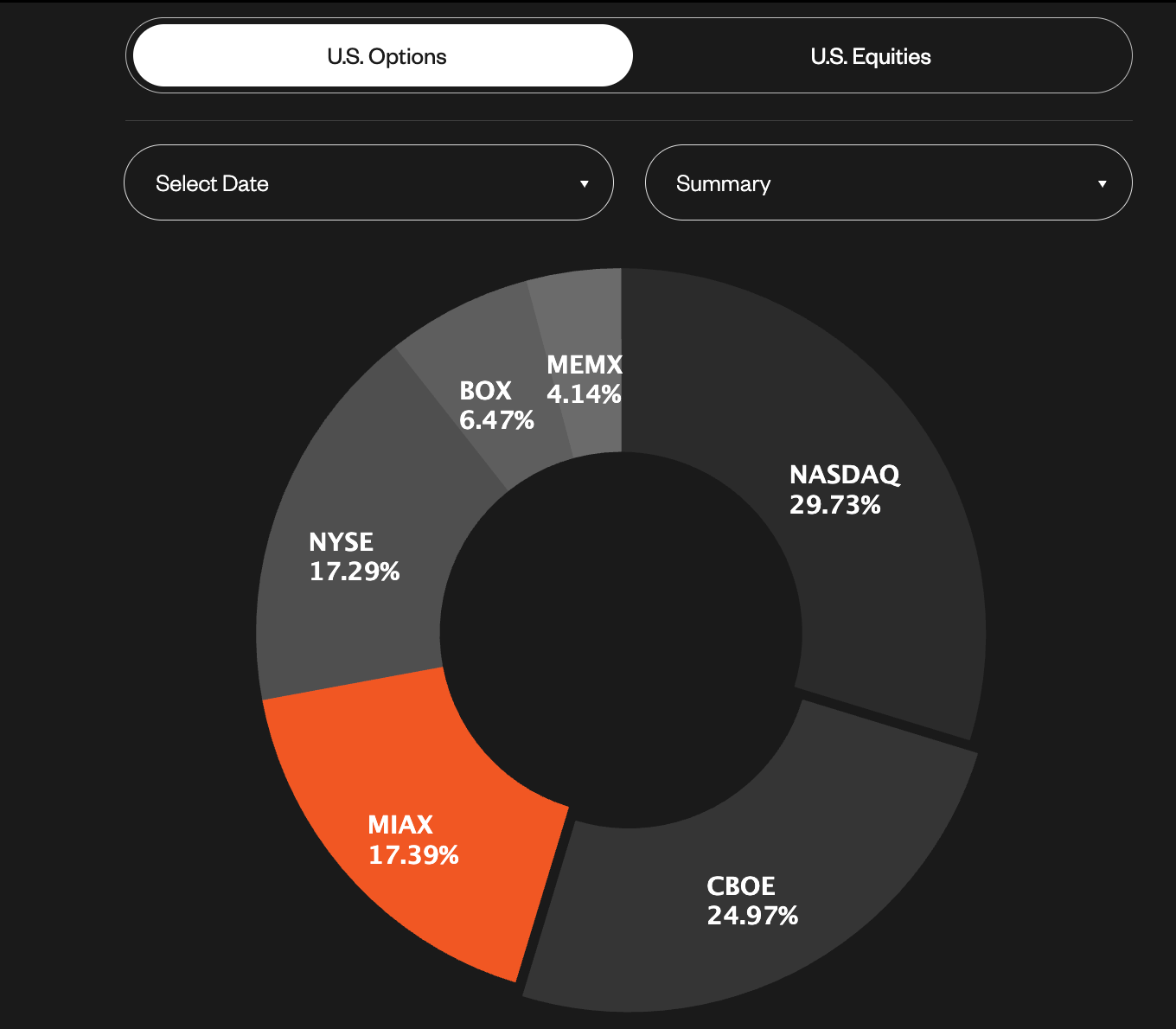

Its share of total U.S. options trading now sits around 17%, a not inconsiderable portion of the market, and one that has been steadily climbing. In the first half of 2025, MIAX’s options venues cleared an average of 8.7 million contracts per day, up from 6.5 million the year prior.

Readers will be familiar with my fondness for options as they are the foundation of my location-independent income business. You can learn more about by joining the list below:

The Options Income Mastermind

I’m opening up a small, private community for those ready to turn options into location-independent income and design a life of real freedom. Inside, you’ll get weekly calls, live trade reviews, and access to my full Options Income framework — plus guest speakers and a network of serious peers. Spots will be strictly limited, and the waitlist is the only way to get early access and priority pricing.

The IPO

The IPO raised $345 million in fresh capital through the sale of 15 million shares at $23 each, a price above the marketed range of $19–21. This placed MIAX’s valuation in the vicinity of $2.3–2.5 billion.

Investors paid up for the structure of MIAX’s business which is a royalty-like compounding machine.

Exchanges Resemble Royalties

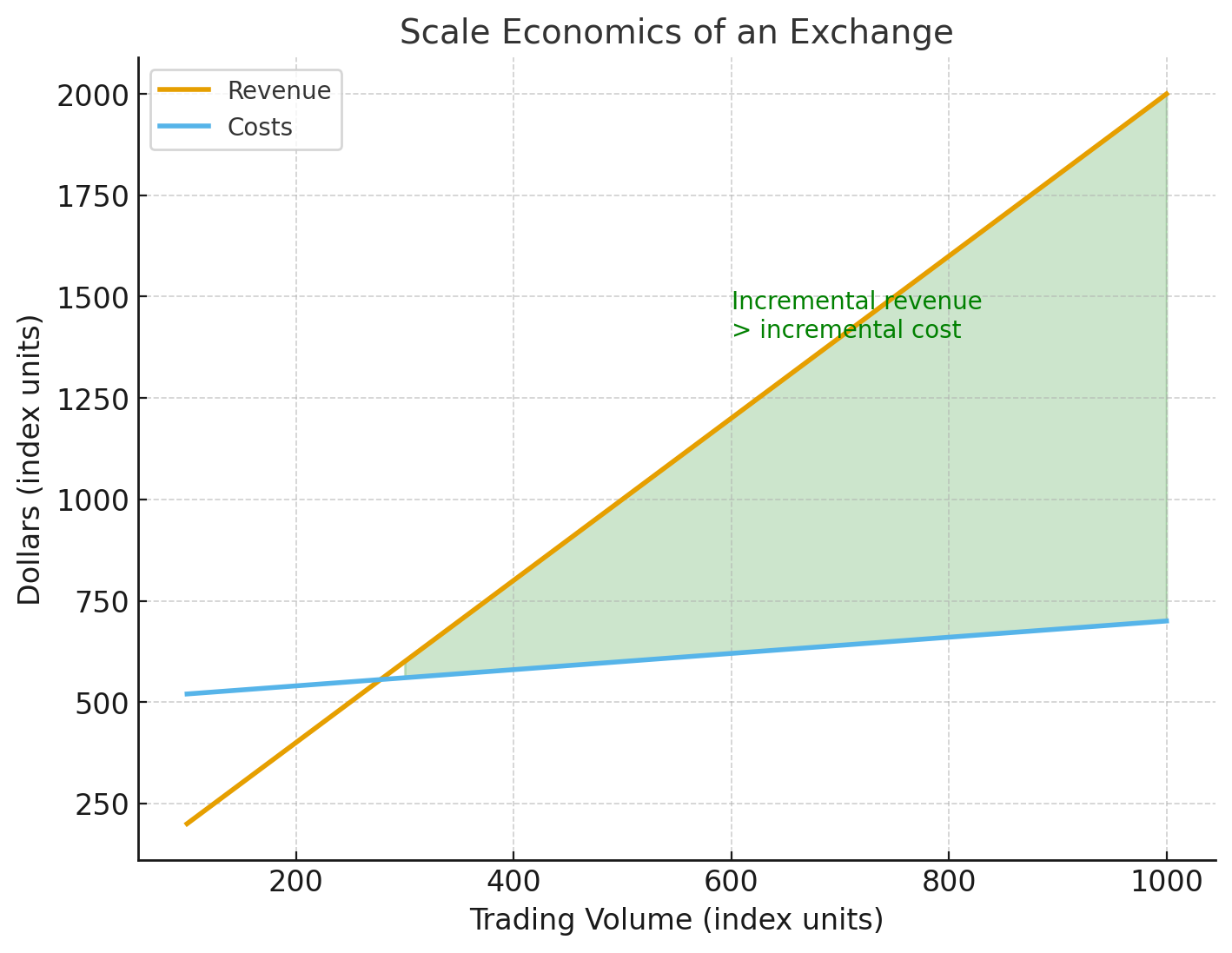

A royalty company, such as Franco Nevada, extracts value by taking a slice of production without incurring the heavy burden of reinvestment. Its revenues rise with rises in volume or price or both.

Exchanges function in a similar way. Once the core infrastructure is in place, incremental volume flows through the system without commensurate rises in expenses.

That is why a 1% increase in trading volume can translate into far more than a 1% increase in revenue. The cost base is largely fixed, so scale economics work in favour of the shareholder.

It is also why the IPO of an exchange deserves attention from those of us attuned to royalty economics. These are scarce assets. They resemble toll roads laid across the highways of capital market transactions.

Risks

Of course, every business model has risks.

Competition: Exchanges are oligopolies, but not monopolies. CME, CBOE, Nasdaq, and ICE each have established positions. Gaining share requires technology that is faster, cheaper, or differentiated. However rather than viewing MIAX’s market share, my eye is more on the total volumes flowing through its products given it’s already shown an ability to proliferate its proprietary products.

Cyclicality: Trading volumes are not linear. They swell in periods of volatility and contract in tranquil times. Ironically making exchanges most profitable when broader markets are under stress. In a way, they possess what I like to call crisis optionality.

War & Conflict: The biggest risk by far, although it is unlikely, is the risk of a large-scale global conflict reaching such a point where capital markets are forced to closed and hence an exchange would stop operating. Apart from a few 1-2 day closures, the last major closure of an exchange was from Jul 1914–Jan 1915 when the London Stock Exchange was closed after the outbreak of World War 1.

Macro Musings, Capital Scarcity and Market Infrastructure

In my recent writings I’ve emphasised a paradox of modern capital allocation: trillions have flown into speculative tech and AI, which rely on enormous amounts of electrical power generation. While sectors and companies involved in supplying that which the power generation requires, are so sparsely represented in the broad indices such as the S&P500 that I can’t help but imagine a sector rotation being potential violent and sudden.

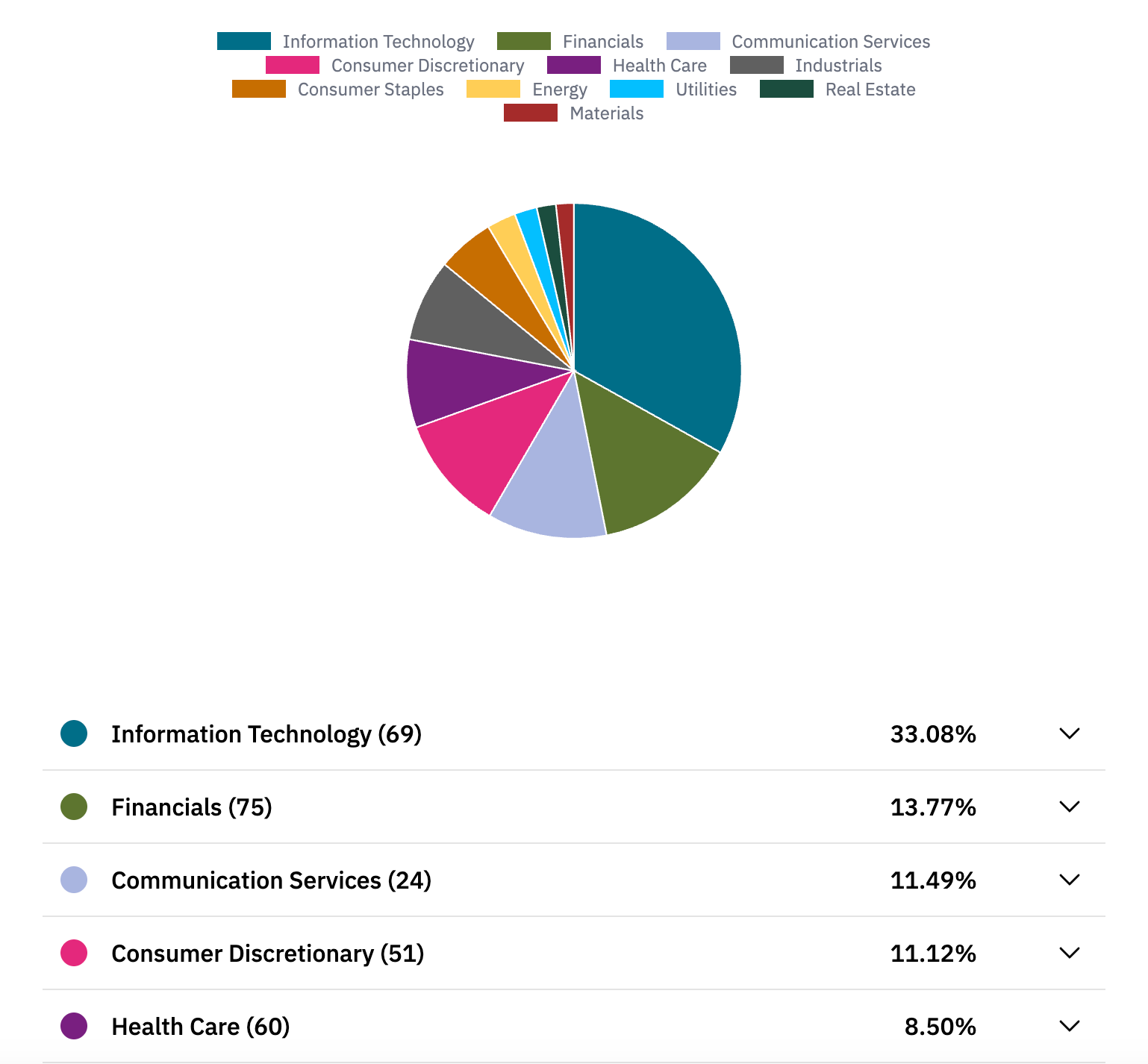

For context, as of today, the market cap of the SP500 is $55.85 Trillion, with roughly 33% of that being made up of tech stocks - which are all fighting madly to out-spend each other in developing AI models.

Meanwhile, only 2.8% of the index is represented by the energy sector which supplies the necessary ingredients to power the data centres that make AI possible. Furthermore, the most represented energy company is Exxon mobile XOM and forms 0.80% of the entire index whilst Texas Pacific Land TPL holds only a 0.03% weighting.

In the event the broader market’s view converged with my own and investor capital were to flow away from the CAPEX spenders in the top third of the SP500 and flow towards the CAPEX receivers like TPL, not only would I be ecstatic with what that would mean for my position in TPL, but it would also be a boon for the exchanges as they are agnostic to the direction of markets or sector rotations and simply clip transaction fees - in this case potentially on tens of trillions of dollars’ worth of sell orders out of the MAG 7 and buy orders on wherever that capital decides to flow.

Capital Scarcity

In contrast to the craze of capital chasing the MAG 7, consider that over the past two decades, the combined IPO valuations of four energy companies that eventually entered the S&P 500: Targa Resources, Kinder Morgan, Diamondback Energy, and Concho Resources, amounted to just $23.5 billion at listing.

Yet in 2024 alone, the technology giants spent well over $175 billion on AI-driven capital expenditure, and in 2025 that figure is on track to exceed $320 billion.

In other words, the total capital that Wall Street assigned to an entire generation of new energy listings over twenty years is less than what the hyper scalers are now spending in a single quarter on data centres.

Exchanges like MIAX sit on the opposite side of that equation. They are capital-light enablers of liquidity. In a world where capital is scarce, the infrastructure that allocates and circulates capital becomes disproportionately valuable.

That is why I expect that rectifying the dearth of necessary capital investment in the energy and materials space over the last two decades might also involve an uptick in IPOs in the energy and materials space in addition to the sector rotation of capital described above.

Exchanges such as MIAX stand to benefit from all of the above and more which is why I’ll be writing more about them in the weeks to come.

The structural economics of MIAX’s business suggest it could become a long-duration compounding asset - a financial royalty on the very act of trading itself.

Disclaimer: This publication is intended solely for documenting my personal journey with trading and investments for income and travel purposes. I am not a certified financial advisor nor am I a financial professional and none of the content provided should be construed as investment advice. It is essential to conduct your own thorough research and consult a registered financial service provider for appropriate guidance. I cannot guarantee the accuracy or completeness of the information presented. Any actions taken based on the information shared in any of my work are done at your own risk and discretion.