Mind the Gap: Strong Setup, Sour Sentiment

Exchanges outperform - and get sold off! | Crown Compendium XI

The Crown Compendia; An informal dispatch on markets, money and my musings. For those who want to go deeper, the links are at the bottom.

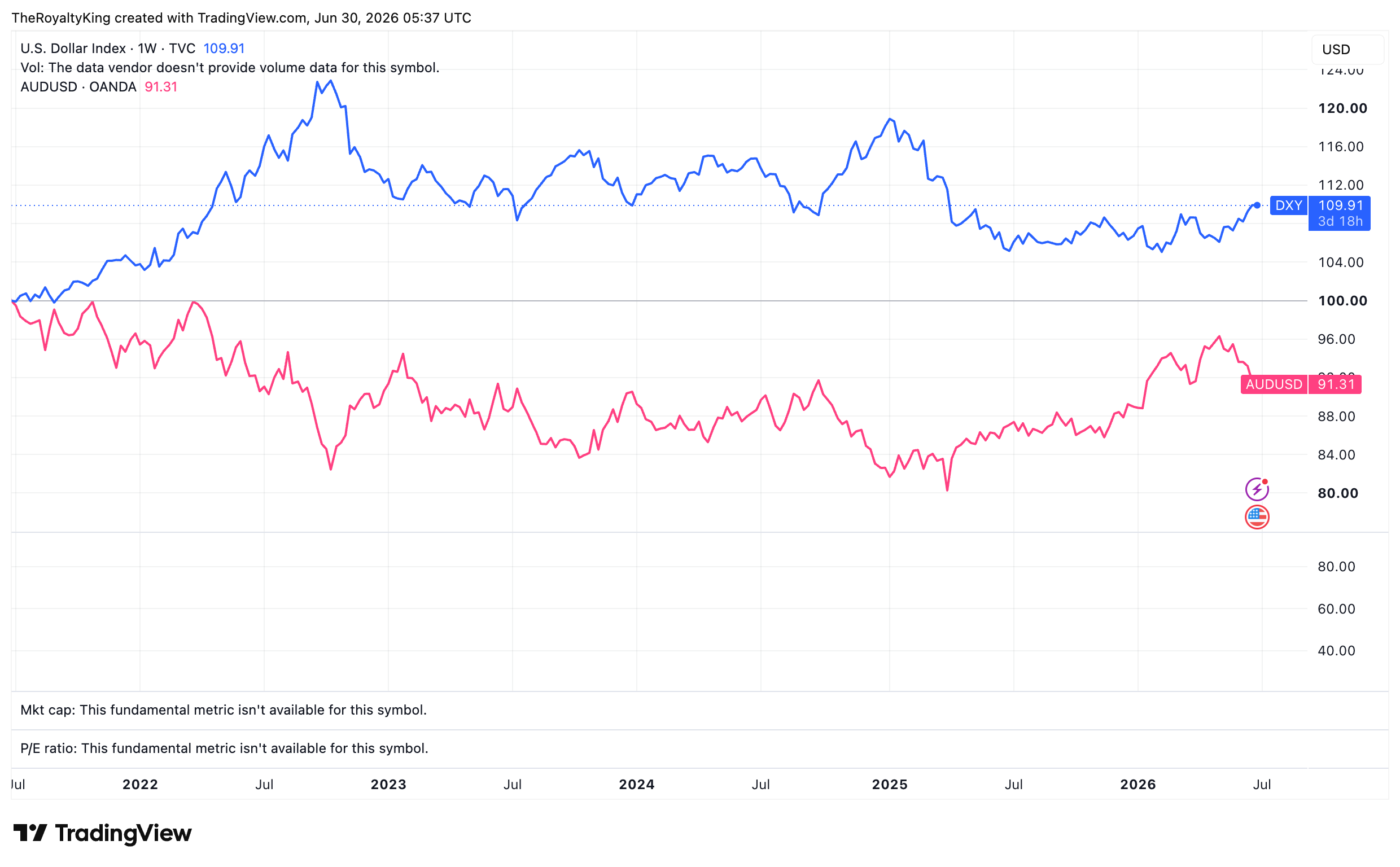

The US Dollar

A rising dollar has taken away much of the mirth felt in market sentiment at the start of the year. A rising dollar acts as a sponge soaking liquidity out of global capital markets and softens demand for commodities all things being equal. I remember the FED’s aggressive rate hiking from a low base effect in 2022 coming out of COVID cause the DXY to spike circa 20% in quick succession, which lead to severe stress on broad indices like the SP500 and the foreign exchange markets, particularly emerging nations with US denominated debt — 2023, the following year was the year to travel to peso-countries!

I recommend this video from Santiago Capital for further explanation to the mechanics of the above:

Gold.

Much ado about Gold’s recent price slump, down 1.8% YTD, yet the fact that it’s up 21% over 12 months YoY (June 30 2025 – June 30 2026) seems lost on many market pundits.

My base case is that Gold has, at most, 10% downside from here before continuing its march upwards and to the right. This is most likely a cyclical downturn in a secular bull market. The dollar is being blamed, but I think China’s stemming of liquidity injections to slow its domestic oil consumption has been more influential in Gold’s price weakness (and that of Oil).

Energy

Oil (both WTI & Brent are basically on par) up ~21% YTD, yet despite the most significant threat of a supply shock in 50 years, a barrel sells for only 9% more than at this time last year, while Nat gas is down 5–8% over the same period and -18% YTD

A better advertisement than the above for owning businesses whose pecuniary interests in the commodities above are expressed through a capital-light structure more attuned to volume rather than price could not be made. Royalties & Streamers and the associated land owners continue to be my preferred investment exposure to these fields.

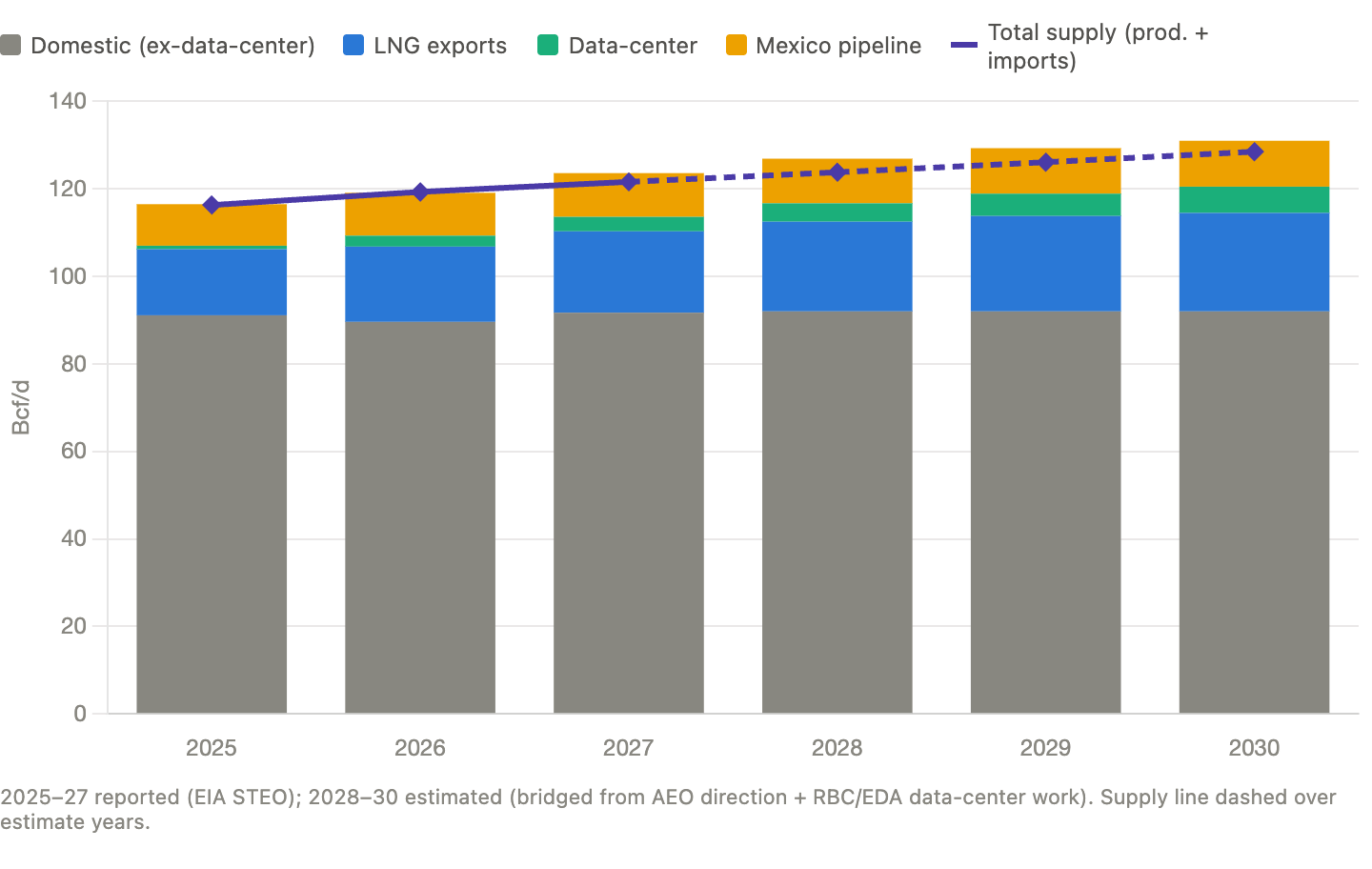

On Natgas: important to note that the market is not really pricing in / believing the estimated additional sources of demand coming online over the next 2 years.

Data centres have made the news here, but the numbers show this is immediately an LNG export story: 5 Bcf of added demand by ‘28, with the expected 4–8 Bcf additional annual demand from DC slated towards 2030.

Here’s my back of the envelope economics as of today, using a blend of the Energy International Association’s (EIA) STEO (Short term energy outlook) and its Annual energy outlook (AEO).

For the more verbal among us:

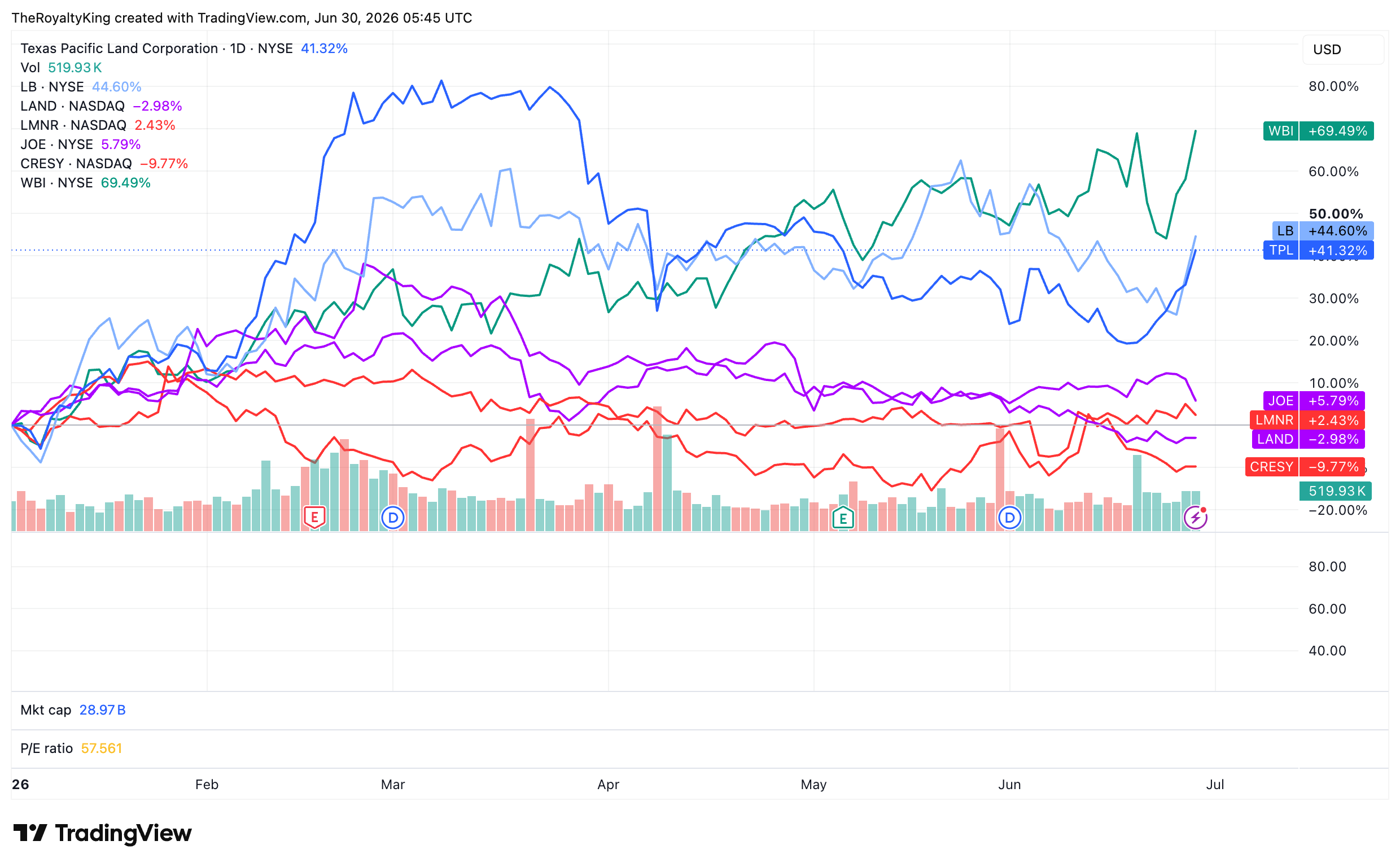

Land & Water

The best performing of my 4 pillars of investment themes so far this year. Including but not limited to the names shown below:

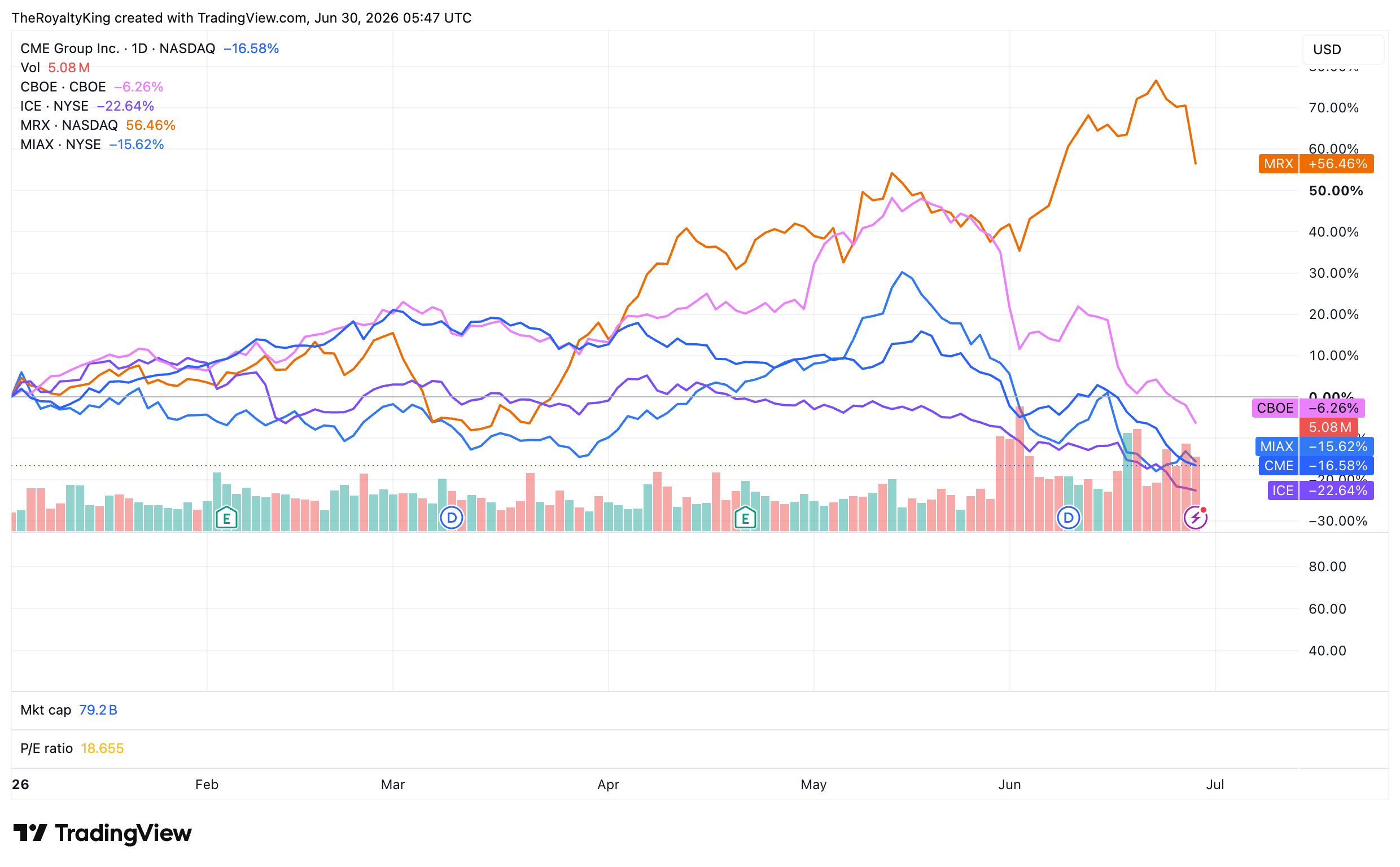

Exchanges & Croupiers

By far the most controversial pillar of my themes so far this year, with bell weathers having drawn down in the double digits YTD on the back of fears of perpetual contracts disrupting their futures and derivatives franchise.

I repeat my view that ‘perps’ are not a serious threat to large institutional capital who need a deep, liquid and regulated exchange through which to place their future hedging needs for currencies, interest rates, energy etc. A contract without an expiration date is of little use for hedging purposes and no sovereign wealth fund is likely to be foolish enough to entrust its capital to an unregulated exchange.

Personally I am using the opportunity to add to my croupiers: especially those exchanges and asset managers trading at double digit free cashflow yields — traditionally an anomaly and amusing that such a price decline would occur after many of them just reported record revenues.

Media

ICYMI — I really enjoyed this video with Mickey Maini. A pioneer in the field of econo-physics and family office investor. He explains his models and how we are likely on the verge of a new monetary system incoming over the next 3-5 years.

Any questions?

DM me or comment and I’ll address them.

Take Care out there.

Benjamin

In Proud partnership with The Solstice Laboratory — the physics of markets, quantified. Read The Entropy Trap to discover what physics knows the economics doesn’t.

How are you measuring

double digit cash flow yields? I don’t believe the routine sources bc 10Q states there are deposits in cash flow statements that don’t belong to the exchanges ( CBOE for example). Do you know a way to adjust these numbers? I think they are too cheap. I just don’t know how cheap.