Pipelines to Waterways: WES Buys ARIS

Western Midstream’s acquisition of Aris Water isn’t just another Permian asset grab—it’s a bet on the future of fee-based infrastructure, ESG alignment, and cash flow visibility.

Well my intuition is spot on it seems.

Recently I have been eyeing off the midstream players in the US hydrocarbon space, in particular Western midstream partners WES 0.00%↑ .

However there are only so many hours in the day, so on returning from the USA I had prioritised an update on ARIS since my original piece here:

James Davolos recently told me he read the piece and therefore we made it a feature of our recent podcast.

Prior to this week, ARIS’s stock price was actually down ~ 20% since I first wrote about it. This got me very excited and I began to size up my position via equity and options thinking I was clever and that in 1-2 years I was likely looking at a multi-bagger.

Then yesterday I woke up this message from our friends at Six Bravo:

Immediately I began to look for a place to unleash my rage..

I must say, I would prefer to own ARIS outright as a standalone company, however given that I was looking at WES’ stock anyway let’s break down the deal.

The Deal at a Glance

Western Midstream Partners (WES) is to acquire Aris Water Solutions (ARIS) in a $1.5 billion cash + stock transaction, expanding WES’ reach into produced water gathering, disposal, and recycling. They also gather and transport Oil and Gas in the midstream part of the value chain for hydrocarbon extraction.

Deal Terms: $25/share in cash (up to $415mm total consideration) and/or 0.625 WES units per ARIS share

Implied EV: $2B including ARIS net debt which will be assumed by WES.

Expected Close: Q4 2025

Acquirer’s Multiple ~7x

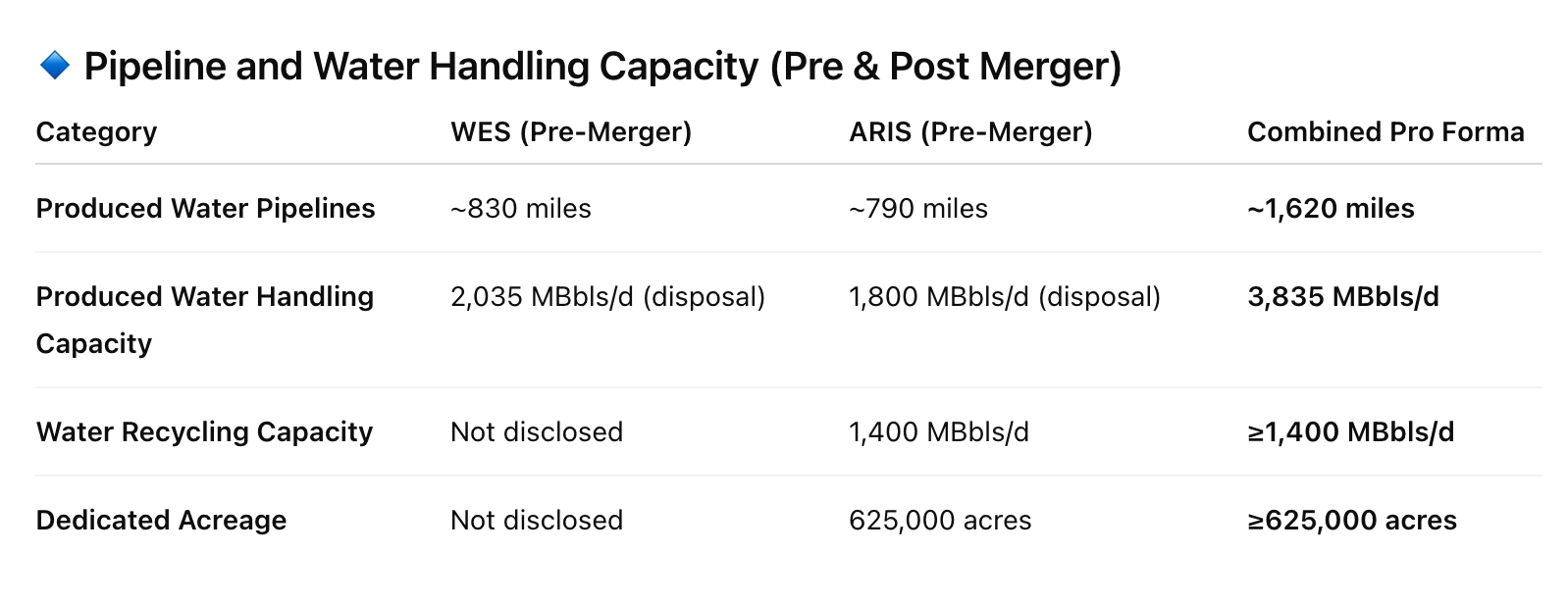

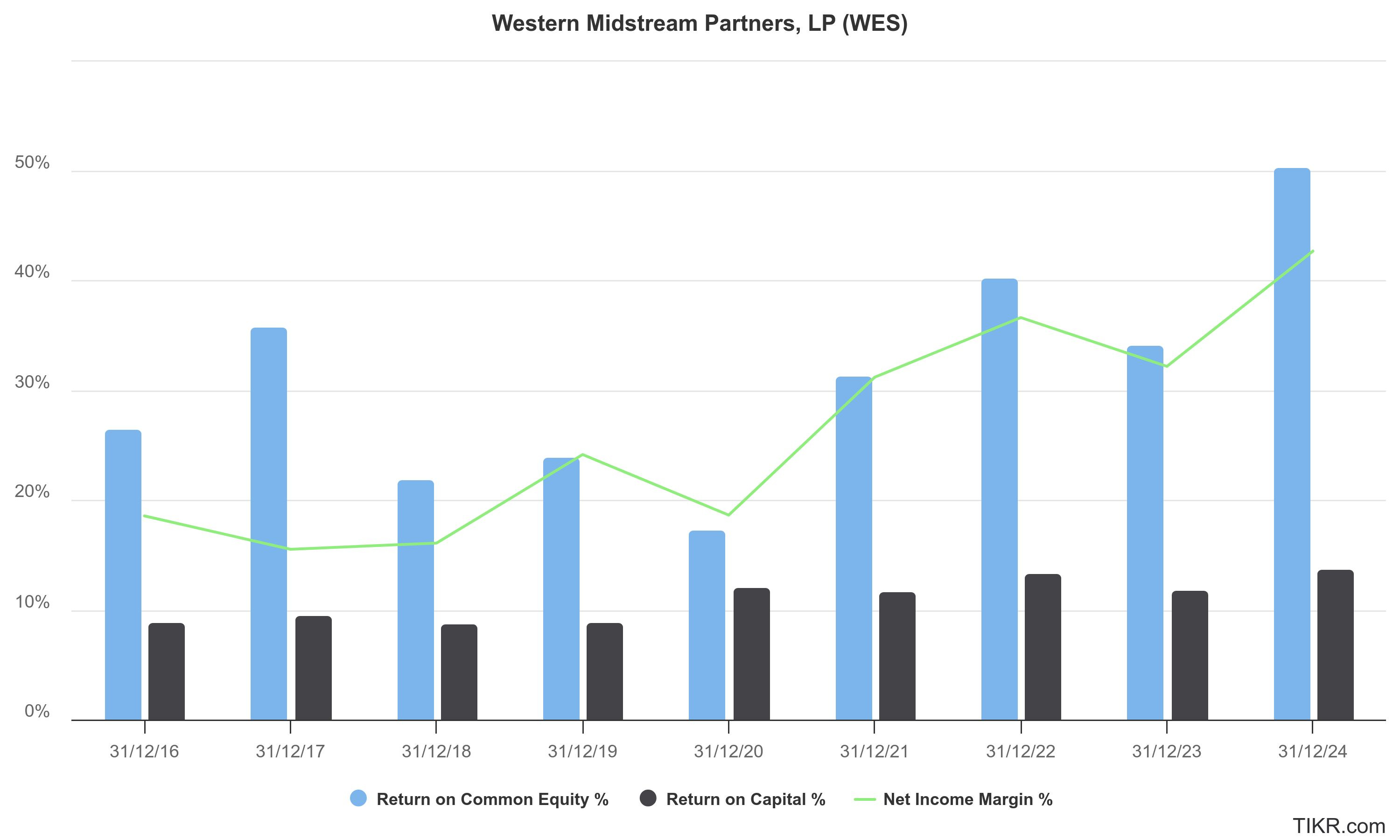

My take: WES got a GREAT deal here, makes a ton of sense for them, less so for ARIS as I saw it as a genuine multi-bagger ramping up to its full capacity, albeit this fast-tracks their growth somewhat. They now get access to the hydrocarbon gathering and increased reach of WES. Let me show you how I see the new pro forma company and then provide some valuation insights.

The transaction implies a $/acre value of $3,200 which I would consider fairly cheap given that it isn’t just empty land being acquired but rather it includes the physical infrastructure of ARIS’ pipelines, which were yet to hit full capacity + water treatment technology which was allowing them to make ever more money per barrel of water handled.

Pro Forma Valuation

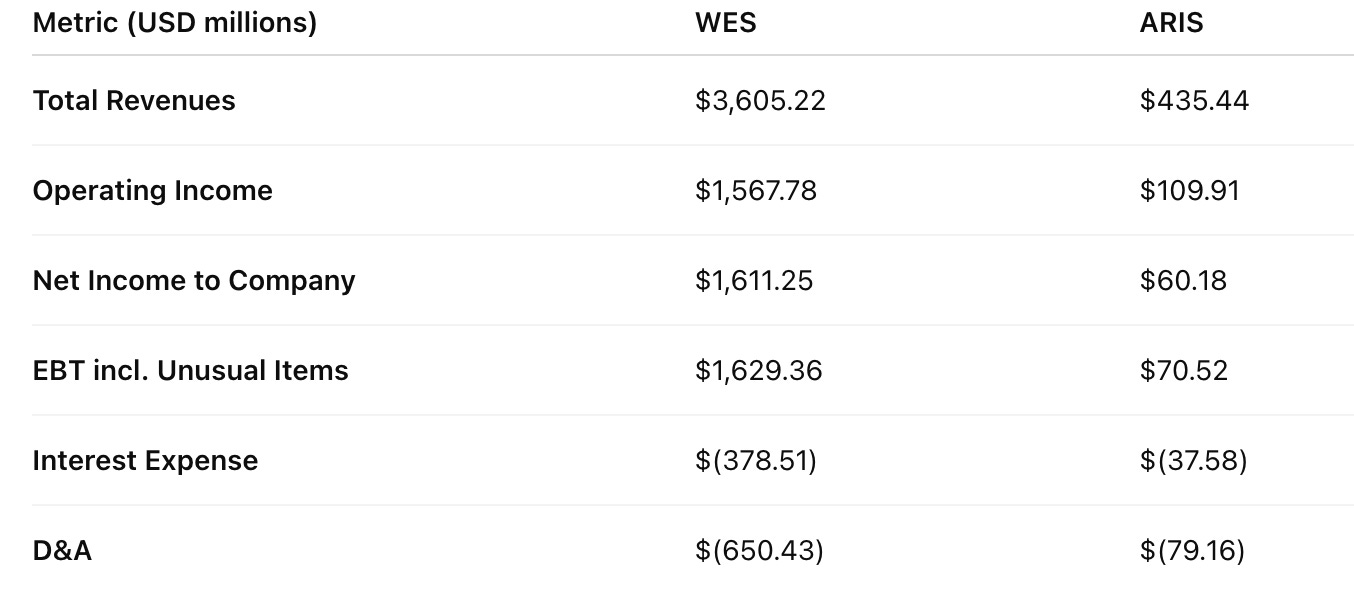

I’m going to take the most recent annual figures as announced by both companies and perform a rough, back of the envelope calculation for the new pro forma looking forward.

EBITDA ≈ Operating Income + D&A + interest Ergo (Rounded)

WES EBITDA 2024 ≈ $2,597mm

ARIS EBITDA 2024 ≈ $226 mm

Pro forma EBITDA = $2,823 mm before further synergies (estimated at $40mm PA)

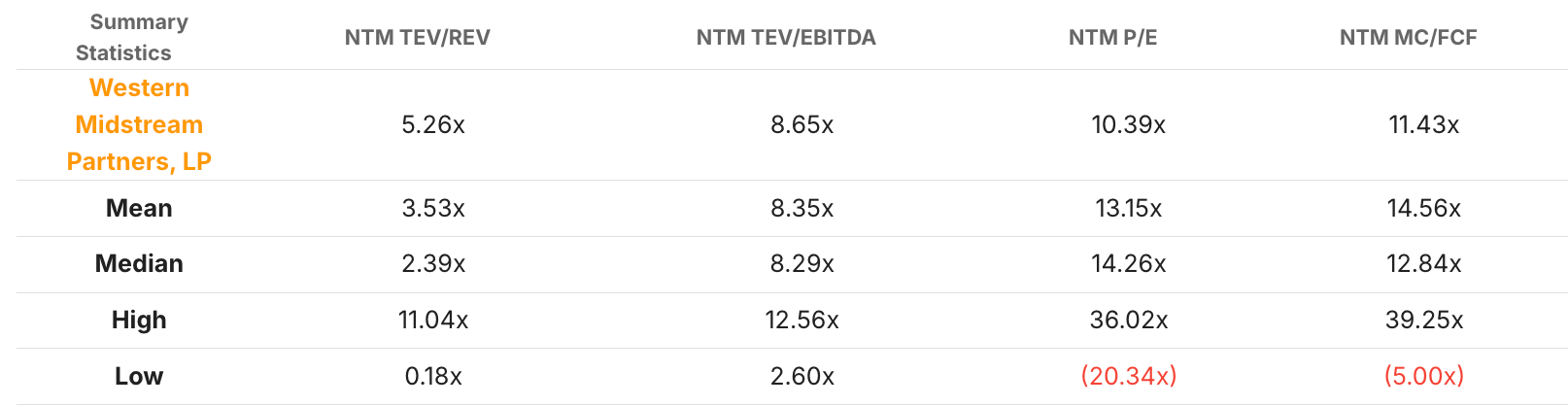

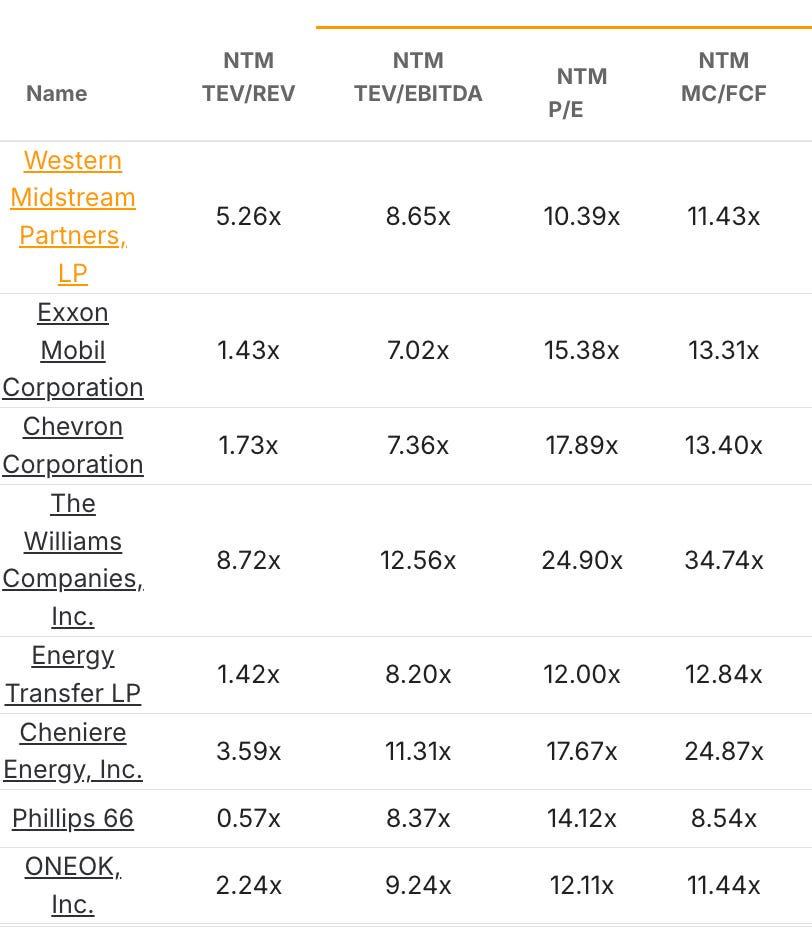

What multiple should a midstream Co. fetch?

When comparing WES to its peers it appears that 8-10X is the going rate.

But wait a minute!

How many of their peers really have a decent amount of their business focused in the handling and treatment of produced water?

It is here where I believe WES has an advantage and therefore merits a higher multiple.

Additionally, their capital efficiency has been excellent for the industry.

So taking $2.8 B in pro forma EBITDA and expecting 10% growth YOY seems like a reasonable notion and therefore I think they can clear $3 Billion in EBITDA in 2026 off the back of this acquisition.

I’m happy to underwrite that using a 12x EV/EBITDA multiple for my simple, drive-by valuation to arrive at a $36 Billion Enterprise value for 2026 Vs the $23.5 Billion EV for the pro forma Co.

This implies a 53% upside from here within a year which is enough to make me feel like there’s value here before delving into the long term potential.

But, where’s the real upside here?

What might this thing be worth when its water handling operations reach full capacity?

Let’s take a look.