Portfolio Construction for a Different World

Royalties, optionality, and income in an era of debasement | Crown Compendium January 2026.

An informal compendium of Market musings trade updates and personal insights

Royalty King’s Remarks

2026 is off to a strong start with markets repricing risk and narratives shifting fast.

Savings

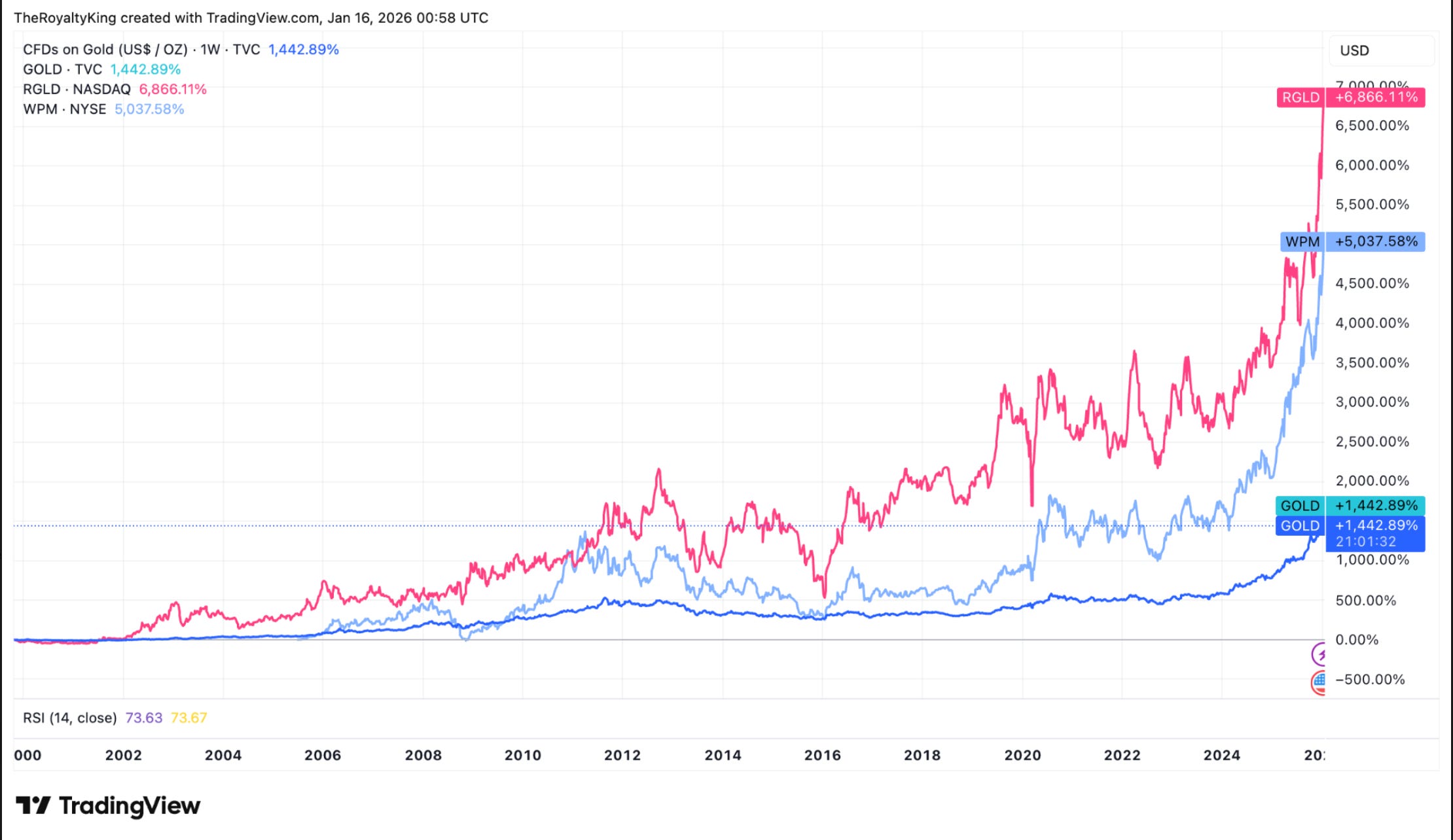

Debasement and the erosion of true purchasing power have long been central concerns of mine, which is why gold and bitcoin serve as my primary savings instruments. I have been vocal in framing gold as the most reliable hurdle rate, operating from the belief that over this cycle, most investors will fail to even keep pace with its performance.

Upon review this view does not appear misplaced.

The proposition of investing is to entertain slightly higher risk than a savings instrument with the aim of a superior return, thus increasing purchasing power over time. As Warren Buffett has long reminded investors when faced with analogous environment :

“Unfortunately, earnings reported in corporate financial statements are no longer the dominant variable that determines whether there are any real earnings for you, the owner. For only gains in purchasing power represent real earnings on investment… High rates of inflation create a tax on capital that makes much corporate investment unwise - at least if measured by the criterion of a positive real investment return to owners. This “hurdle rate” the return on equity that must be achieved by a corporation in order to produce any real return for its individual owners - has increased dramatically in recent years. The average tax-paying investor is now running up a down escalator whose pace has accelerated to the point where his upward progress is nil…”

“As we said last year, Berkshire has no corporate solution to the problem. (We’ll say it again next year, too.) Inflation does not improve our return on equity”

- Warren Buffet’s 1980 letter to shareholders (emphasis mine)

The above requires some serious reflection.

Particularly the last line.

Is there a class of businesses for which inflation enhances, rather than erodes, return on equity?

Long-term readers will recognise the answer immediately. If that’s you, congratulations, you are already ahead of the curve. Such businesses have long been central to the focus of this publication.

Over the past 26 years, gold bullion has compounded at approximately 11% per annum, establishing itself as a benchmark savings instrument for purchasing-power preservation.

Yet the same period reveals a structural advantage available to those willing to move one layer up the value chain. Royalty and streaming businesses tied to precious metals compounded at 16–18% annually converting gold exposure into equity returns.

For many investors, the simplest way to outperform the benchmark savings asset was not leverage, timing, or speculation, but ownership of the royalty & streaming Co.s.

On The Interview With Doomberg

Whilst I agree with many of the points made by Doomberg , I do not share his contention that gold is not a commodity, but rather money. Every good, that is: gold, you, and I for that, matter, money can be consider a commodity through an economic lens in that it adheres to a supply and demand dynamic. Gold behaves idiosyncratically due to its demand being mainly as a form of storage (money), leading to large stock levels. Its supply is relatively difficult to come by hence its inherently low stock to flow ratio, which in turn solidifies its main use case as being money.

However, history has shown that it is in fact possible to have hyperinflation even in societies on a gold standard when circumstances result in a dramatic new supply of gold entering into an economy. The flood of New World gold into Spain following the conquests of the sixteenth century produced precisely such an outcome whose consequences, according to many economic historians, echoed for generations

The more legally inclined reader might prefer considering whether gold conforms to the following definition of a commodity

Commodity:

“an economic good, such as a raw material, that is interchangeable with other goods of the same type.”

Source: Merriam-Webster

Gold clearly fits the definition.

FAQ

What is your view on Royal Gold Corp (RGLD)?

In brief: I own RGLD and continue to hold it. It might be the cheapest precious metals royalties in the above $20 Billion Market Cap space.

Which commodities Are You Most Bullish on in 2026?

Land & Water. I have been buying land which has water rights and energy royalties for some years now and I believe the party is only getting started.

Consulting

An increasing number of clients are seeking consulting input on portfolio structuring for retirement. In many cases, this involves the integration of royalty-style business models alongside options-based digital income strategies. Enquiries can be directed via private message on Substack.

For non-Platinum members, this service is provided on a pay-as-you-go basis.

Exotic Trades

Updates on two exotic trades, the first of which might be the single best risk–reward combination of 2025, delivering both appreciation and recurring monthly income from an appreciating asset. With the trade having now come home, I am, for the time being, leaving my gold exposure unhedged.

The next trade was closed early as the stop loss level was reached. A small loss, improbable, yet was incurred as per the rules of the trade.

The expected value of its consistent application over time remains positive.

Wishing you all the best.

— Benjamin

The Royalty King

Excellent thread thank you