I’ll be attending the Rule Symposium (online) this year.

If you’re serious about commodities, capital cycles, and long-duration thinking, this is where the real conversations happen.

The Australian Securities Exchange (ASX: ASX) is the only practical venue through which Australian equities can be cleared and settled. It holds a function so systemically critical that its regulator has described its stable operation as essential to the integrity of the entire Australian financial system . Curiously however, it is currently priced as though that monopoly were in question. It is not.

Today’s article hits close to home, given the antipodean roots of this author having spent most of his childhood in Terra Australis.

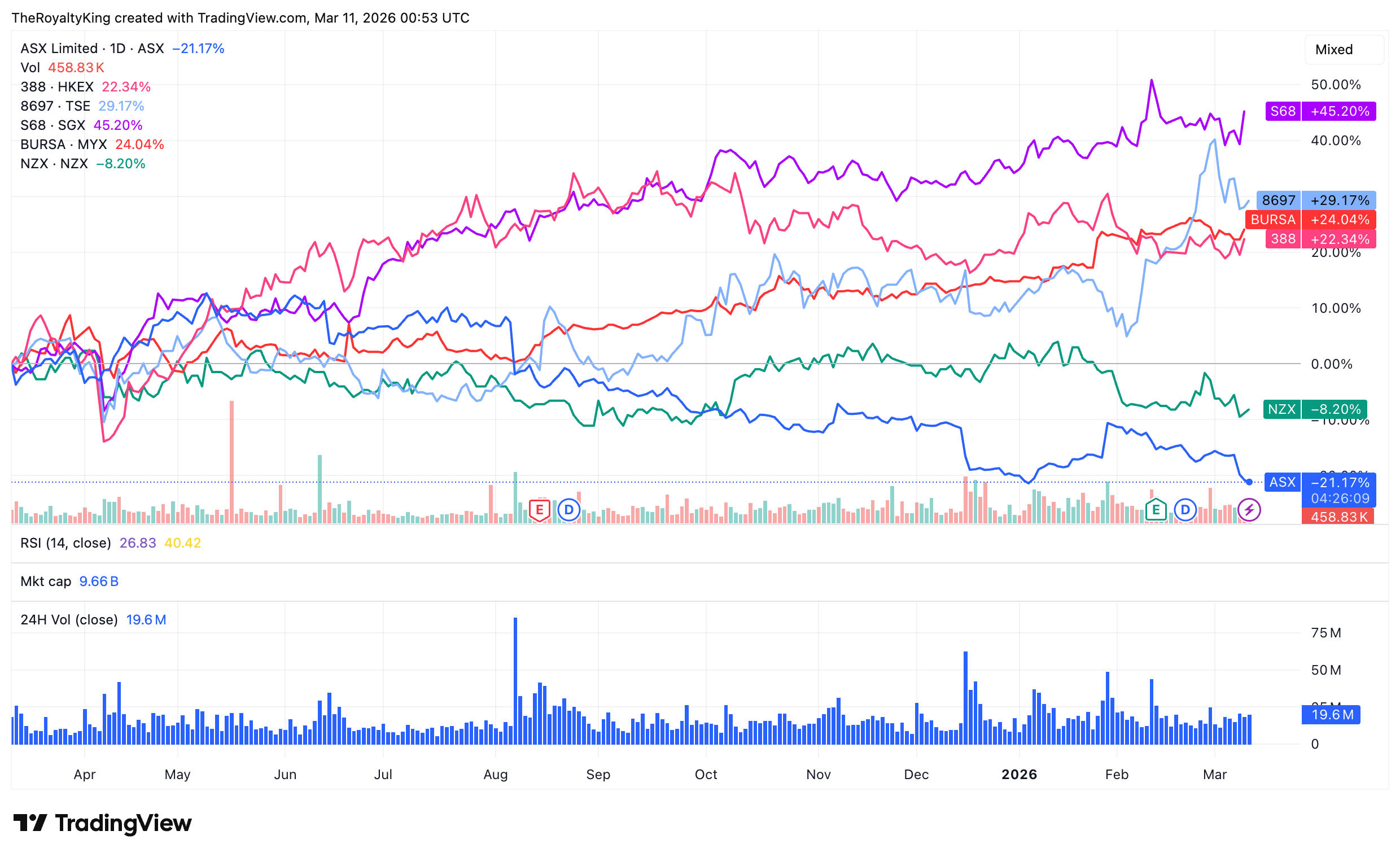

It’s often easy to miss the opportunities closest to us and as evidence I was surprised to learn upon my perusing of global exchanges, that one of the worst performance stock exchanges globally (and the worst in south east Asia) is none other than the ASX, The Australia Stock Exchange. I mean, stone the crows, even the bloody kiwis are doing better! (NZX).

It’s not very often that an investor can form a buy thesis on an exchange and frame it as a ‘turn around, or special situation’ yet it appears that is in fact the case here which, given the enviable business model that exchanges nejoy, might provide a discounted entry into the monopoly toll road on the Australian economy. An economy which stands to benefit greatly from an anticipated boom in natural resources.

Exchanges occupy a rare position in capitalism. They are toll collectors on financial activity. Every trade, listing, capital raise, hedge, or margin requirement passes through their infrastructure. The marginal cost of processing an additional transaction is close to zero, while the fees are recurring and difficult for market participants to avoid. This results in a business model characterised by:

• network effects

• regulatory moats

• low capital intensity

• very high operating margins

Few industries possess all four simultaneously.

For a primer on the exchange’s business model and why it might be the best in the history of publicly traded markets see the below white paper.

The Australian Economy — What The Conventional Misses

The conventional view of Australia is not wrong, it is just incomplete. Australia is a resources-heavy economy with significant China exposure, a relatively small domestic population of 27 million and a history of commodity cycles that have provided sensitivity for government finances and corporate balance sheets.

The ASX 200 index is roughly 30% financials and 20% materials. Simply put, when iron ore falls, the index falls. When the banks get in trouble, the index gets in trouble.

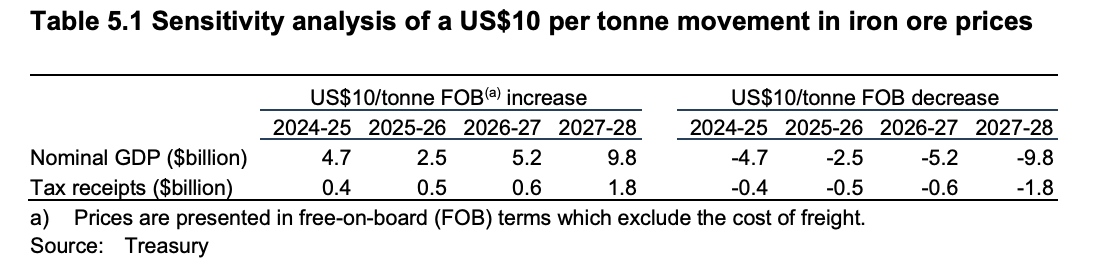

A $10 change in the price of Iron Ore can correspond with a $0.5-$1 Billion swing in associated government revenues and affect GDP to the tune of ~$5.2 Billion. Such an impressive statistic highlights the sensitivity of the Aussie economy to global commodity demand.

The Mining Boom as an Exchange Boom

Current geopolitical re-arrangements have led to a new type of ‘arms race’ in that governments globally are now intent on adjusting their supply chains and engaging in a high stakes scavenger hunt in order to secure the raw inputs need for the manufacturing of goods which underpin the economies, militaries and technology development of developed nations.

Such a circumstance necessarily means a new breath of life (and more importantly, an awful lot of capital expenditure) into developing critical mineral deposits, something which Australia has in abundance.

In fact, Australia holds the world’s largest reserves of lithium, the second-largest reserves of cobalt, the largest identified deposits of nickel sulphide, and is one of the world’s dominant iron ore and copper producers.

The boom for mining is a boom for ASX listings, IPOs, secondary capital raises, derivatives hedging, data licensing, and clearing volumes. The ASX doesn’t need to pick the winning commodity or the winning miner. It just needs the activity to continue and structural global demand for critical minerals suggests it will, and for a very long time.

There is also the matter of the gold price. Australia is the world’s second-largest gold producer. Gold is at or near all-time highs. Gold companies are raising capital, hedging production, and listing new vehicles and the ASX is the primary venue for all of it.

Blunder Down Under

Given the positive nature of the aforementioned, the reader may be wondering why a business with such a privileged position would sell off so heavily?

This is because, to quote the spider man movie, “With great power comes great responsibility”. Continuing the logic: with great responsibility, comes even greater regulatory scrutiny.

Unfortunately, a failed technological gambit threatened to disrupt trading activity and pushed ASX into the crosshairs of the Australian Securities Investment Commission (ASIC).

A few years ago the ASX attempted to replace the 1994-era CHESS system using distributed ledger technology. The project which began around 2015 was abandoned in November 2022 resulting in a $250 million write-down. ASIC subsequently sued ASX in the Federal Court, alleging that statements made in February 2022 that the project remained “on-track for go-live” and was “progressing well” were misleading and deceptive.

A truly embarrassing error occurred on Christmas Eve 2024 when a group of trades failed due to faulty code in CHESS. Apparently this code contained instructions that had existed since 2014. Not a good look.

A formal inquiry into ASX was launched in 2025 and the results are now known:

ASIC has imposed an additional $150 million capital charge on ASX, to be accumulated by June 2027 and held until remediation milestones are met to ASIC’s satisfaction.

Consequentially, the dividend payout ratio has been cut. Return on equity targets have been trimmed. Attempt 2 at CHESS replacement is underway with a new consultancy team and is targeting a new clearing system by mid-2026 and a settlement system by 2028-29.

Longer term readers will recognise these dynamics, that is: a situation in which a quality business model is experiencing a temporary difficulty and a dividend cut which the market does not have the patience to see through even when a fairly solid timeline is available.

Similar situations can be found in the archive including, but not limited to: $MSB, $HE, $SJT, and so far, as of the time of writing, patience and extending one’s time horizon past the standard calendar year and out towards 2-3 years has paid off.

The opportunity arrives thanks to the market, which is fixated on the ASIC run-in and is pricing this as a tired infrastructure stock. What it actually is, when you strip away the noise, is a royalty on the Australian financial system, backstopped by a compulsory private retirement scheme and an endowment of resources that the is growing more valuable by the day.

The ASX is not losing its position as the central counterparty for Australian equities settlement next year, or the year after.

Now let’s cast an eye over what it might be worth to an investor with a view towards the future.