The Gas Market’s Best Kept Secret

The Gas royalty Wall Street is sleeping on could 3x as drilling ramps and distributions return.

“The big money’s not in the buying and the selling but in the waiting”

-Charlie Munger

At the time of writing the equity markets appear to be assigned very generous valuations broadly while most hard commodities trade at or above their marginal cost of production.

Ergo, apart from a few select sectors such as pharmaceutical royalties and emerging-market utilities, I take the view that there’s not an awful lot of buying to do. Current conditions instead bode well for revisiting past theses.

I find myself content — sitting back and reviewing the investments made over the last two years, most notably in precious metals royalties.

My landholders with royalty and water rights initially rocketed upwards, before pulling back since Q4 last year. Still, my table-bagging across the royalty sector has paid off handsomely — not a single royalty or streaming position sits at a loss (so far).

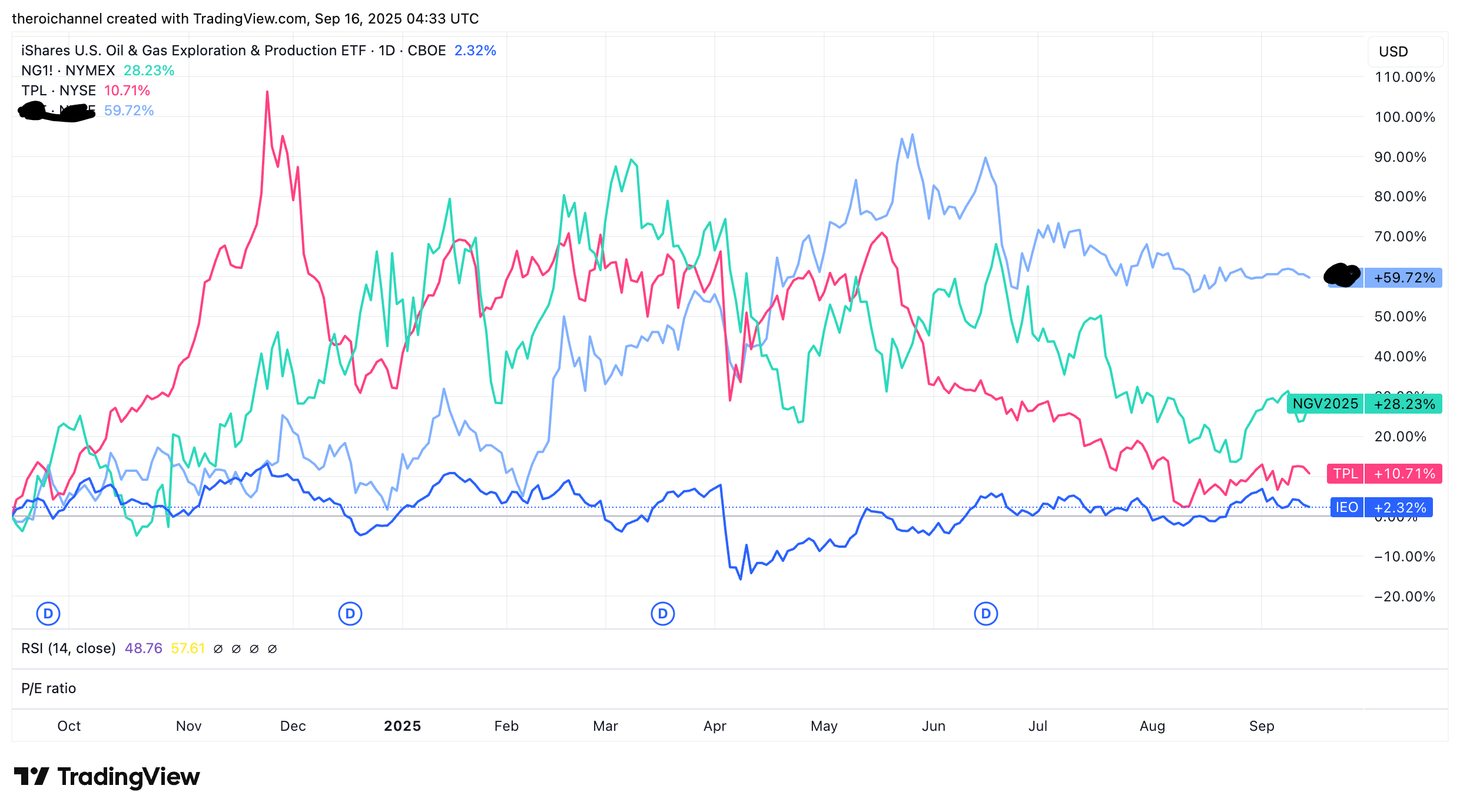

Energy continues to disappoint most investors (outside uranium equities) with WTI and US natgas trading at $63.17 and $3 respectively at time of reference.

Despite people being bored with US Nat gas, its price is up 28% over 1 year from an admittedly absurdly low trough in 2024.

US oil and gas producers are barely above water yoy while the quintessential royalty in the space, TPL has managed double-digit returns - albeit from an initial 100% rise on the back of its inclusion in the SP500 at the end of 2024.

One of my more obscure royalty picks, however, has quietly outperformed them all — up 60% and consolidating for what looks like a further breakout.

This brings me to the point: the expected convergence of US gas (Henry Hub) with global prices has yet to occur — and maybe won’t be the sound-and-light show many, myself included, once expected.

That’s exactly why I prefer royalty and streaming models. They deliver robustness when your macro expectations take longer to play out — or don’t at all. And when chosen carefully, they offer asymmetric participation in the upside.

This is why I prefer to invest in the royalty and streamers whose business models provide a robustness when you’re initial expectations take longer to play out than expected (or not at all).

Which makes now the right time to revisit one of my key ideas: