The Immortal Asset: Water Economics in The Permian Basin

The cost to handle water in the Permian has quadrupled and the profits flow to those who own the pipes rather than the wells.

Those who know me best know that I am in awe of the writings of Jorge Luis Borges.

So much so, that I have recently duplicated my collection of his works by buying the english translations to accompany the original Spanish editions in which I first read his life-changing works.

Borges was obsessed with the English language and actually read more in English than in ‘Castellano’ and preferred to re-read the same volumes rather than read new works.

Re-reading his works - this time in English - strikes me as something that the master himself would do - although he often said that it pained him to read his own works.

The first story of The Aleph - ‘The immortal’ recounts a man’s journey to discover a water source that grants eternal life only to discover that eternity is both a gift and a curse in its endless flow that erases meaning.

Water has always been symbolically associated with perpetuity. It cannot be destroyed, only transformed and as I wrote about in the piece below, it is one of only two commodities that is a true inflation beneficiary - the rest tend lower in terms of real pricing over time.

In the Permian Basin, this same element that sustains life has become the lifeblood of industry, circulating endlessly through rock, pipe, and profit.

Yet, as is fast being realised in the Permian Basin, its eternal presence is now also becoming a curse as the produced water as a byproduct of hydrocarbon fracturing is now a serious issue affecting the region which has become 46% of American oil production.

The following is an overview meant to explore the historical trend in produced-water generation and handling in the most prolific hydrocarbon basin of the United States which today, in times of resource nationalism and geo-political uncertainty is expected by some to become the swing producer to the world.

**A major source used in this piece was this report submitted to the US department of Energy in 2022**

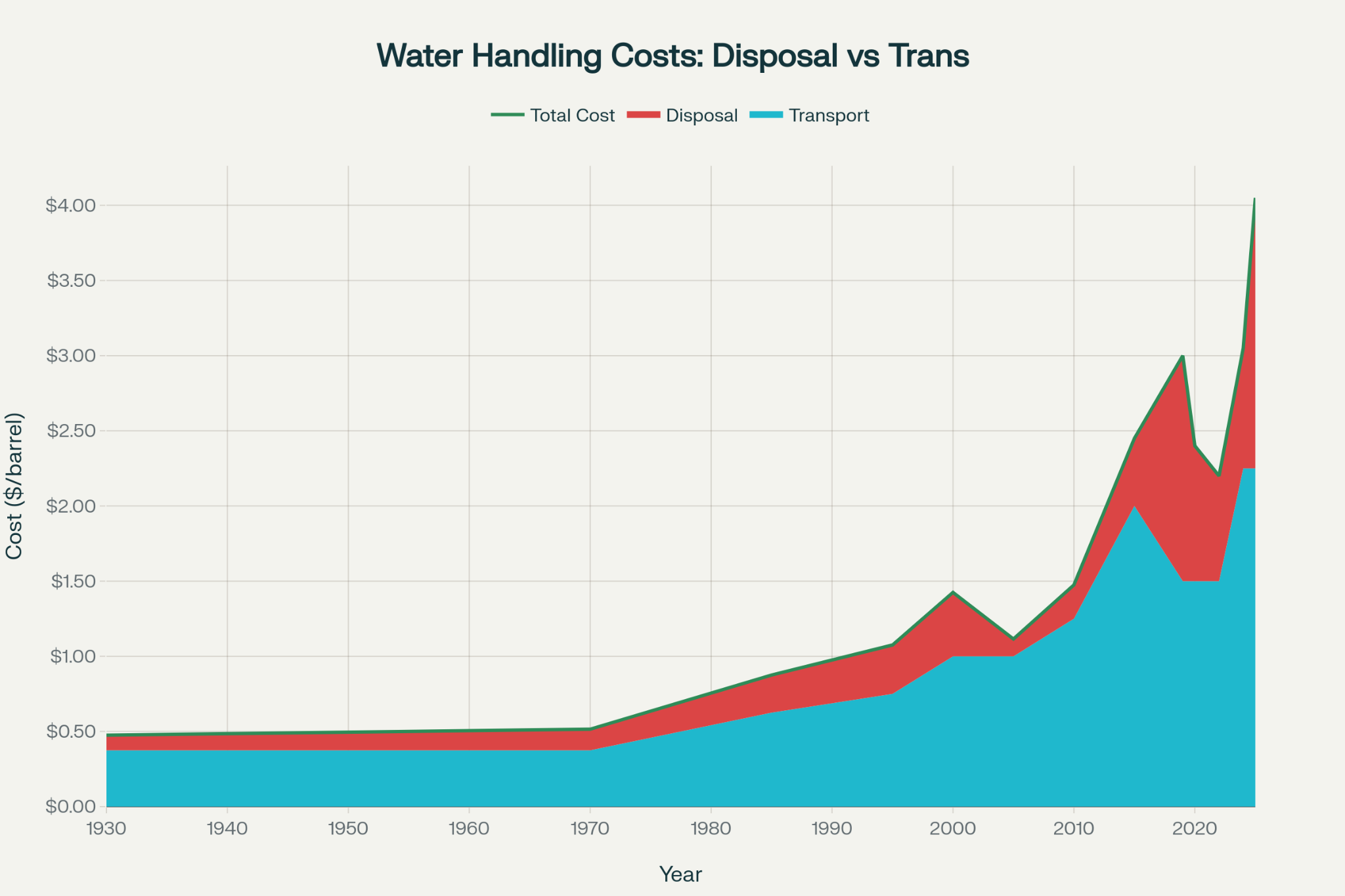

Historical Cost Evolution

The research analysis reveals three distinct eras in produced water cost evolution:

Early Development Era (1930-1970)

Costs remained relatively stable at $0.48-0.52 per barrel total handling cost, with disposal costs of $0.08-0.14/bbl and minimal transportation requirements. Most operations used gravity-flow systems with basic saltwater disposal wells.

Conventional Production Era (1970-2005)

Moderate growth driven by regulatory compliance under the Underground Injection Control (UIC) program. Class II well regulations introduced standardisation, while environmental requirements increased treatment costs. Total handling costs reached $1.11/bbl by 2005.

Shale Revolution Era (2005-Present)

The most important period for my investment thesis, with costs accelerating from $1.11/bbl in 2005 to $4.05/bbl in 2025 - a 3.6x increase in just 20 years. This reflects the massive volume increases from horizontal drilling and hydraulic fracturing as well as drilling of acreage with higher water cuts.

For the more visual of my brethren - here’s a chart I made.

Current Pricing

Average Disposal Cost: $1.80/bbl (44%)

Average Transportation Cost: $2.25/bbl (56%)

Transportation has become the dominant cost component, reflecting infrastructure constraints and the need to move water longer distances to available disposal sites.

This competitively positions pipeline companies with exisiting infrastructure to capture much of the market share over time as producers move away from disposal methods with higher transport costs and enter into agreements with the likes of Waterbridge et al.

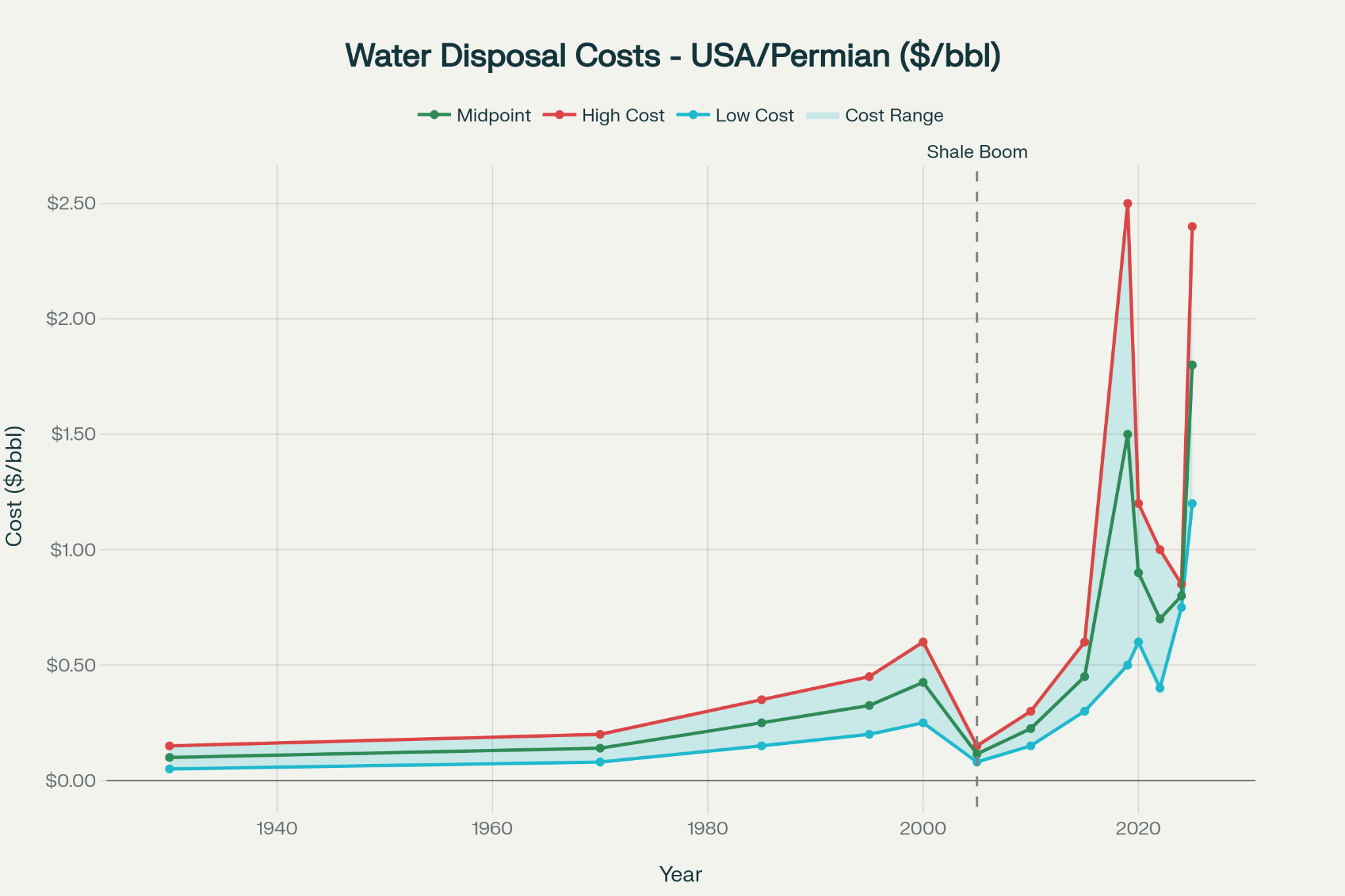

Industry data indicate that on average produced water disposal costs in isolation roughly doubled every five years in the Permian since shale really ramped up. In 2010, disposal ran about $0.15 per barrel rising to $0.30 by 2015, to $0.60 by 2020 and today in 2025 at and ave of ~$1.20 resulting in close to a 15% CAGR in disposal fees.

Side-note: Compared to the circa 3-4% CAGR in the oil price it makes you wonder which is the main commodity behind investing in the permian.

What’s very interesting to note is recycling produced water for reuse (fracturing new wells) has now become cheaper in many cases around $0.15–$0.20 per barrel, which is significantly below typical disposal fees. The issue is that this results in an even higher water-cut (water’s eternal nature again at work) but remains key and why I was upset that ARIS water was bought out so soon by WES.

Volume

Shale dramatically increased produced water volumes in the Permian Basin, driving up the cost of handling (gathering, treatment, and disposal) over the past decade. With each barrel of oil now accompanied by multiple barrels of water (the curse of the perpetual asset). The Permian Basin now produces over 22 million barrels of water daily, with water-to-oil ratios (water cut) averaging 3-4:1, yet some wells reach 12:1. This is a 350% increase in produced water volumes since 2017

For these factors it should impress the reader that the rate of increase in water volume is not linear: as more wells are drilled, cumulative water volumes rise more steeply than oil alone in many cases. Consequentially and somewhat inversely, a temporary decrease in drilling activity in the face of soft commodity prices as suggested by Doomberg will have a subdued effect on water volumes due to the ratio of the water cut.

Subsequently, as water volumes grow disproportionately, the marginal cost of water handling becomes more critical. Those companies that own the infrastructure for disposal, recycling, pipelines, etc. will arguably capture more of the upside in stress cycles.

I see disposal capacity at scale as becoming constrained (others disagree), which means that pricing power and value concentration will increasingly accrue to infrastructure owners in future. Overlaying a capital-light business model with interests in such infrastructure is what has lead me towards companies such as TPL, LB, WBI and ARIS (now part of WES).

If in fact we are in for times of flat energy prices punctuated by upticks it will likely by thanks to the super-majors acting as, as Doomberg suggests, ‘deflation machines’. This will logically require more drilling presence in the Permian and as I’ve outlined above bring with it even more produced water to be handled. I want an investment that does fine in all environments and has free call options stacked to benefit from pockets of inflation or price shocks.

Hopefully you've enjoyed this piece - feel free to re-stack if so.

Until next time - take care and check out the articles in my archives.

Benjamin

PS: By the way - don’t forget to join the waitlist for my upcoming mastermind.

The Maverick Life mastermind is under construction and will document how I live my life with complete freedom by generating borderless cashflow: income I can generate anywhere in the world, without employees, clients, or products.

I’ll also bring in the brightest minds in international living to showcase how I’ve acquired multiple passports and residencies across 3 continents.

👉 Join the Waitlist Now and make money flow wherever you are 🌍