The Last Cheap Royalty

Copper & Tin in a Royalty Wrapper. The Royalty King Research Report | Evolve Royalties (CSE: EVR) | April 2026

Don’t forget to grab your ticket to the Rule Symposium below.

In the winter of 2024 I became aggressively bullish and, I daresay, rather vocal on a sub-sector of the market that exhibited the unusual circumstance of quality assets trading at extreme discounts to book value. Junior royalty companies were changing hands at sub-0.5× BV. One in particular; Gold Royalty Corp, had reached approximately 0.3× book, which inspired me to write several pieces and build it into a high-conviction position. Hindsight is 20/20, but this really was a lay-up. The stock re-rated to above 1× BV, from $1.20 to $5.18 in little more than a year.

Since then I have lamented two things with regards to the natural resource markets: an absence of no-brainer-book-value-cheap royalty companies, and a dearth of quality exposure to base metals — copper in particular.

Today’s focus company addresses both criteria simultaneously.

I’ve taken a starting position in a relatively unknown royalty Co. with interests in copper and tin and is also likely to be the only royalty co. still trading at a discount to its book value.

Executive Summary

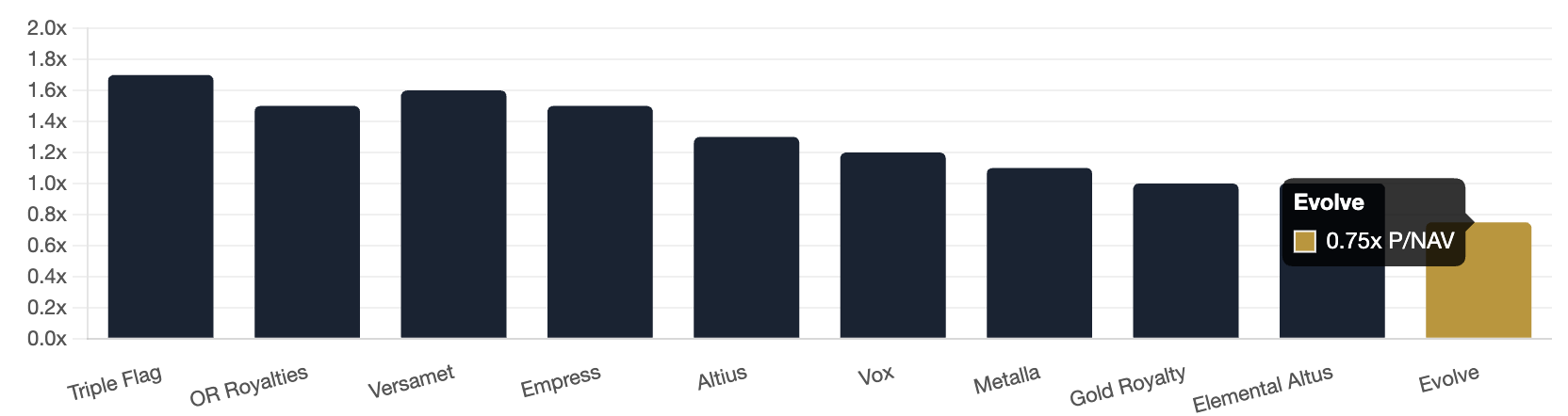

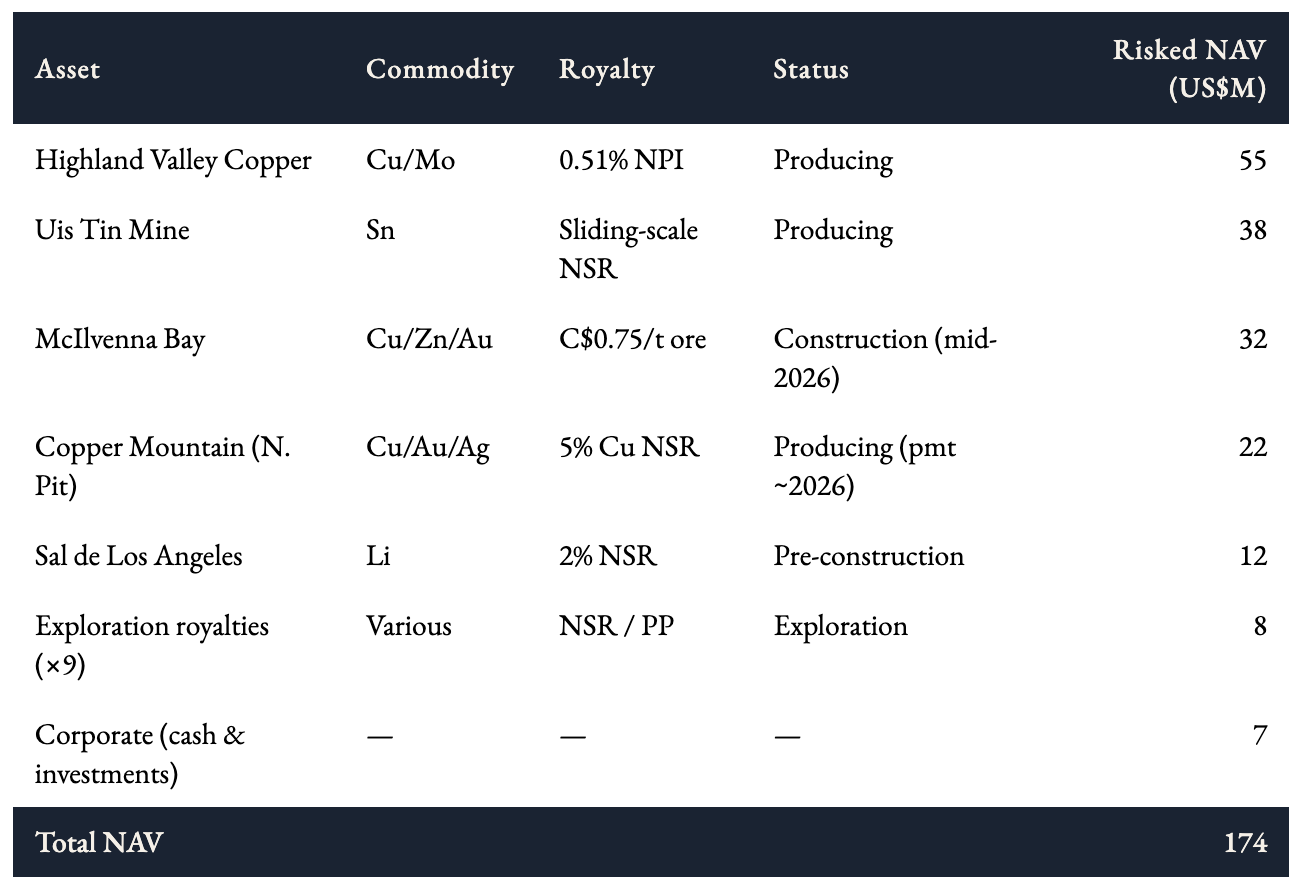

Evolve Royalties (CSE: EVR) is a royalty and streaming company with interests in copper, tin, lithium, and gold. At C$3.21 per share, the company trades at approximately 0.75× my current NAV estimate and is the lowest P/NAV multiple in the junior royalty peer group by a material margin. It is the only royalty vehicle simultaneously offering exposure to: Canada's largest copper mine, Canada's newest copper mine and a producing tin royalty generating US$4–4.5M in annual cash flow.

Remarks On Valuation & Context

A technical note on royalty valuation first.

Although from time to time I take a slice of the Royalty’s expected cashflow runway and perform a 5-10 yr Net present value (NPV), the ‘correct’ approach is to evaluate each royalty individually and perform a bottom-up Net Asset Value calculation. This provides an estimate that is a snapshot in time and while useful directionally, fragile to point-in-time commodity assumptions and almost always understates the optionality embedded in future production which, thanks to the business model, is a free call option with an investor today doesn’t have to pay to hold. The market is notoriously clueless in appreciating this.

My philosophy is that it is far more important to be approximately and directionally right, with a solid base case and a range of free call options embedded in the structure, than to attempt precision and be precisely wrong.

With that caveat stated, today’s NAV of US$174M is conservatively calculated and presents Evolve as an attractive opportunity on a relative valuation.

The junior royalty peer group trades at 1.0–1.6× NAV.

Gold Royalty and Elemental Altus trade at or above 1.0×. Triple Flag and Versamet sit at 1.5–1.7×. Thus the NAV discount applied to Evolve is not subtle.

The natural question is: why?

The answer: size. Evolve is small, listed on the CSE rather than the TSX or NYSE and has not yet accumulated the institutional following that re-rates these vehicles. The exact same setup was witnessed in the junior gold royalty sector less than 18 months ago; it is stunning how short-term the market’s focus is. What is lagging is recognition and recognition, in small-cap royalty land, is a function of time and demonstrated cashflow.

Portfolio Snapshot

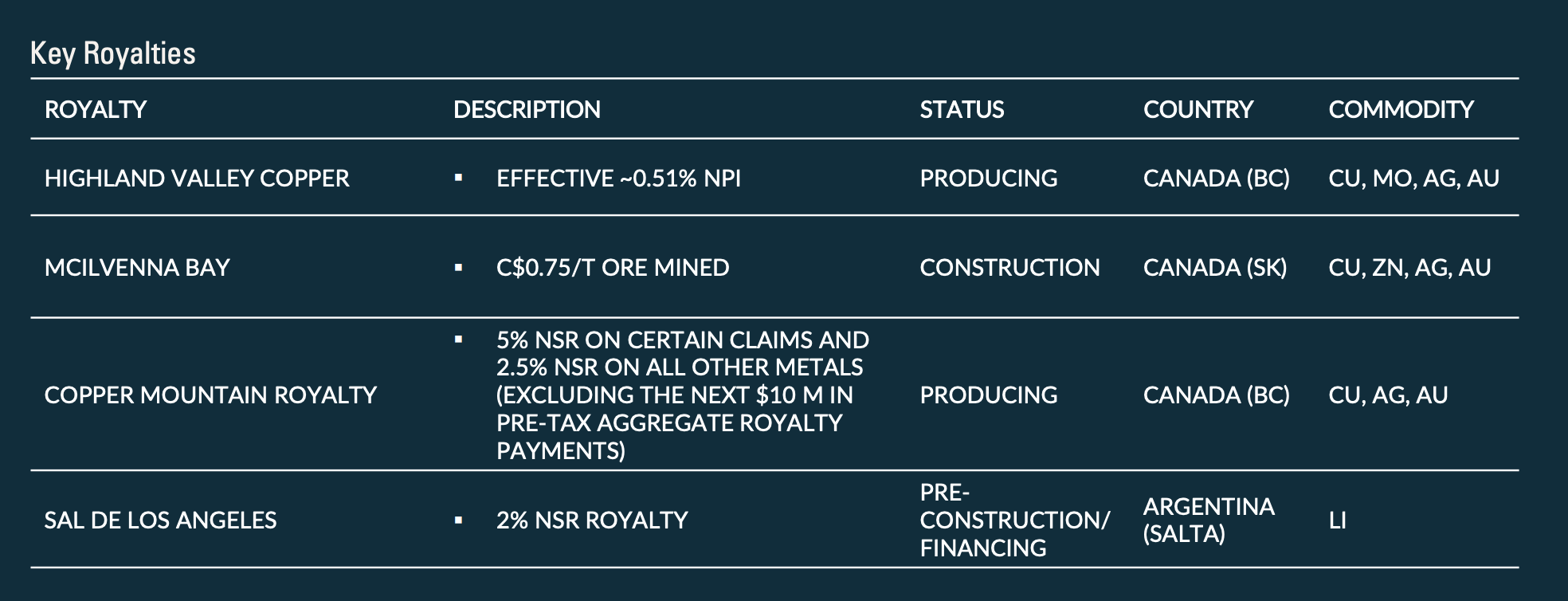

The cornerstone asset is a 0.51% Net Profit Interest (NPI - A weaker type of royalty) on Highland Valley Copper in British Columbia and is Canada’s largest open pit copper mine, operated by Teck Resources since 1962. In 2025 HVC produced 127,100 tonnes of copper. In July of that year, Teck sanctioned a Mine Life Extension program that extends the mine’s operating life from 2028 through to 2046, at an average annual copper production of 132,000 tonnes.

The NPI structure concentrates approximately 32% of our NAV estimate in a single asset which is a concentration that warrants disclosure. An NPI is more leveraged to copper prices than an NSR: it only pays when the mine is profitable above Teck’s reported cost base and Teck controls those inputs. In a sustained low-copper-price environment this structure may underperform a simple royalty.

This as the primary risk to monitor.

Highland Valley Copper | 0.51% Net Profits Interest | NAV: US$55M

The second producing asset is where the story gets interesting.

On February 24th of this year, Evolve entered into a definitive agreement to acquire a cash-flowing sliding-scale royalty on the Uis Tin-Tantalum Mine in Namibia for US$32.5 million. It produced 1,071.6 tonnes of contained tin in 2025, achieving nameplate capacity for the first time. It is expected to produce between 1,000 and 1,100 tonnes in 2026. The mine life exceeds 40 years, with significant additional resource on proximal pegmatites and active lithium development studies running concurrently.

Given there were really only 2 prior tin-based names available to investors previously and both were miners in Banana republics (Congo and Australia) the advent of a tin-royalty is highly attractive to this author.

The royalty generates US$4–4.5 million per year at current tin prices and provides a payment schedule already in motion.

Uis Tin Mine | Sliding-Scale NSR | NAV: US$38M + huge right tails

I share the entire NAV model with premium members below.

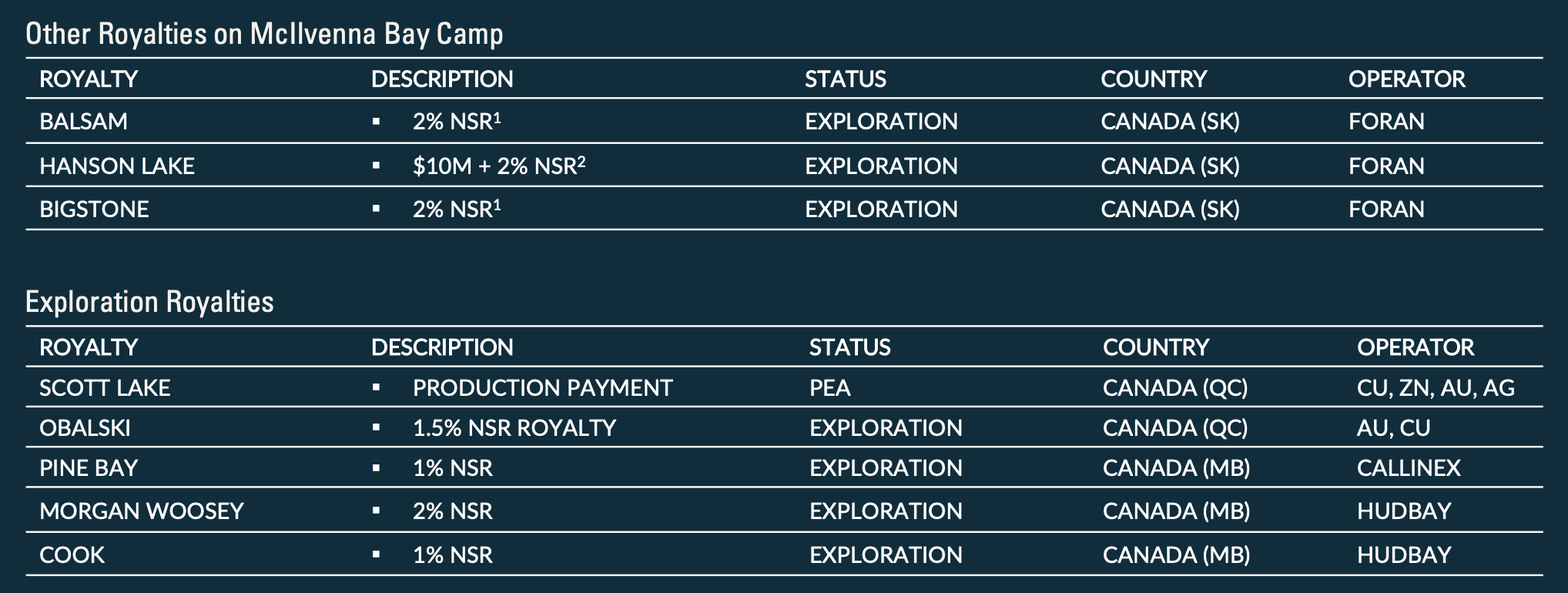

Additionally, the company has added a nice list of contracts that are at various stages of development and provide free call options on a multitude of commodities.

Tin and Copper: The Same Trade

There is a version of this story that positions Evolve purely as a copper royalty play and that version is already compelling on its own merits given that, aside from Altius, there really isn’t another pure-play copper royalty. The structural undersupply of copper + insufficient developments, declining ore grades etc.is among the more well-known themes in resources investing.

But the Uis acquisition adds an intelligent peculiarity: tin.

Tin is a small market with approximately 379,000 tonnes of global demand in 2025. Roughly half of that demand is solder, used in electronics manufacturing. It is, in a real sense, the element that joins copper to everything else: circuit boards, power inverters, EV drivetrains, solar modules, data centre infrastructure etc. Where copper moves electrons, tin connects them. The supply base is heavily concentrated in China, Indonesia, and Myanmar; each is subject to its own catalogue of regulatory and geopolitical risk. The development pipeline is thin and the market is widely expected to enter structural deficit later this decade.

For a royalty investor, the tin angle represents something rare: high quality commodity exposure that is difficult to access and is attached to a mine with a 40-year resource base with a competent operator who restarted it from brownfield in 2022 and hit nameplate capacity within three years.

EVR is, to my knowledge, the only listed royalty vehicle offering simultaneous exposure to copper and tin in a single share. That is not a small distinction.

Synopsis

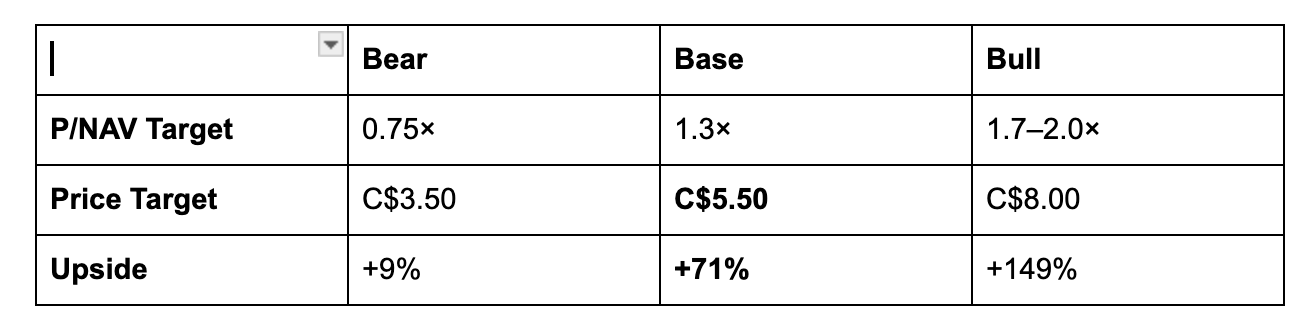

The simplest way to think about this investment thesis in the near-term is to consider a reversion to at least fair value (1xNAV) providing a 25% upside; that’s the no-brainer, low-hanging fruit.

However one does not simply buy a royalty co as a mean-reversion trade and call it a day.

Let’s explore the potential of this most rare of beasts: a copper/tin royalty.

Here’s a fully developed model, with all the numerous and necessary details concisely presented in a Bear/Base/Bull case.