The Only True Bitcoin Treasuries?

The Purest BTC-per-Share Compounding Machines are 2 Small Caps Nobody Knows

“The Debasement Trade” Is a term which has recently taken on immense popularity.

It refers to a simple observation that governments the world over have chosen the path of fiscal expansion without restraint. The cumulative consequence of endless deficits, unbalanced budgets, and the growing political taboo around austerity is that the currency must be the adjustment variable.

Fiat money, in essence, is the residual claim on all promises a state cannot fulfil. Ergo by necessity, it will be devalued.

I’ve been writing and obsessing about it for years as you can see from the articles in the archives where my contention is that in a world where the rate of fiat currencies’ debasement is picking up steam, outperforming of the denominator that represents real money (gold or Bitcoin) will be quite a difficult task.

In recent weeks, major banks like JPMorgan have explicitly labeled Bitcoin and gold as expressions of this trade.

Labels aside, what matters is the mechanism: money creation has outpaced productive output, and rational capital seeks refuge in the ‘unprintable’.

If the debasement trade is officially in vogue, then the question becomes: which instruments capture it most purely and defensibly?

Bitcoin is the only commodity with an immutable supply protocol in which its price is almost completely irrelevant.

Yet not all “Bitcoin exposure” is equal.

Early this year I had the privilege of chatting with Randy Smallwood of Wheaton Precious Metals. His focus on creating value on a per share basis is what has lead to WPM becoming the world’s preeminent precious metals streaming company.

This philosophy is foundational in my approach to screening potential investments in bitcoin-companies.

If an investor wants exposure to Bitcoin there are really only 3 ways to get it:

Buy BTC directly on an exchange and hold it privately

Buy shares of a BTC ETF such as: Greyscale or IBIT etc

Buy shares in a company that acquires bitcoin - either via mining or a ‘Bitcoin treasury Co. Almost all of which raise equity continuously to buy bitcoin, which is by definition dilutive.

BTC per Share: The Forgotten Metric

If you wish to hedge debasement, your goal is to own something whose unit of account strengthens over time.

In an operating company, that would be one whose earnings per share (EPS) rise faster than inflation.

In the digital monetary era, it might be viewed as growing Bitcoin per share (BPS) rather than dollar denominated EPS.

It astonishes me that so few seem to care about this.

The proper test of any “Bitcoin treasury” company is not how many coins it holds in aggregate, nor the dollar value of those coins.

The key metric is how many coins per share the entity controls and whether that figure can be sustainably grown over time.

If BPS increases, you are compounding an unprintable asset internally.

If it declines, you are being debased somewhat debased even if in Bitcoin.

The Problem With the ETFs

Consider the widely expanding BTC ETFs. They are efficient, regulated, optionable, convenient and thus attractive to institutional capital but they cannot possibly be accretive in terms of BPS.

Each must sell small portions of Bitcoin to pay the sponsor’s fee and operating expenses, de minimis though they may be.

That is structural dilution.

Ergo, over time, an ETF’s BPS must decline.

The Problem With (Most) Miners/Treasuries

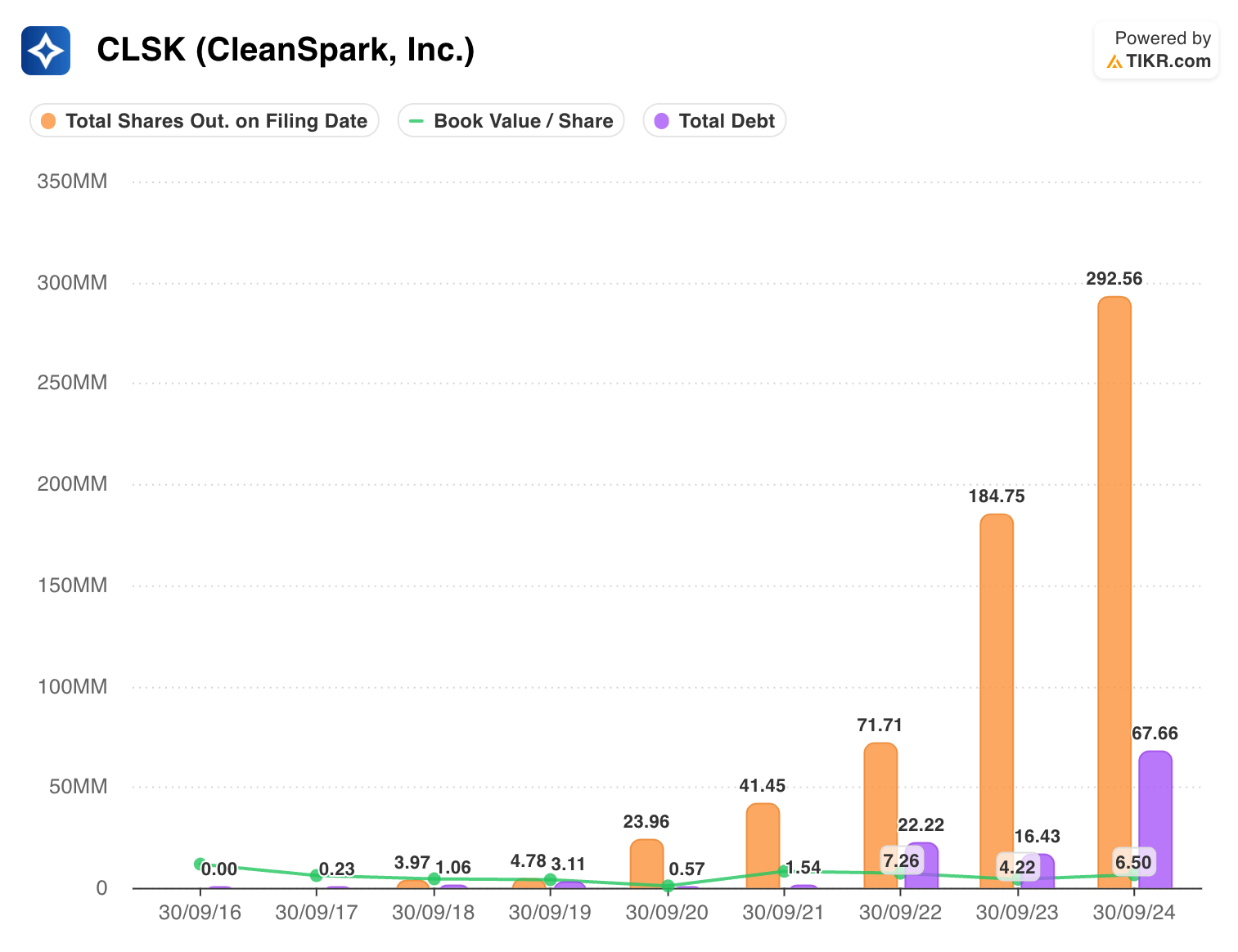

Evaluating the well known BTC miner, CLSK, shows they have been successful in adding BTC to their balance sheet. However, when juxtaposing the BTC acquired to the share dilution and debt taken on by the company, it becomes clear that the underlying model relies on dilution. Dilution of share ownership might also be considered a form of inflation, which begs the question : how much of an inflation hedge such a business model can truly be?

The Market Darling

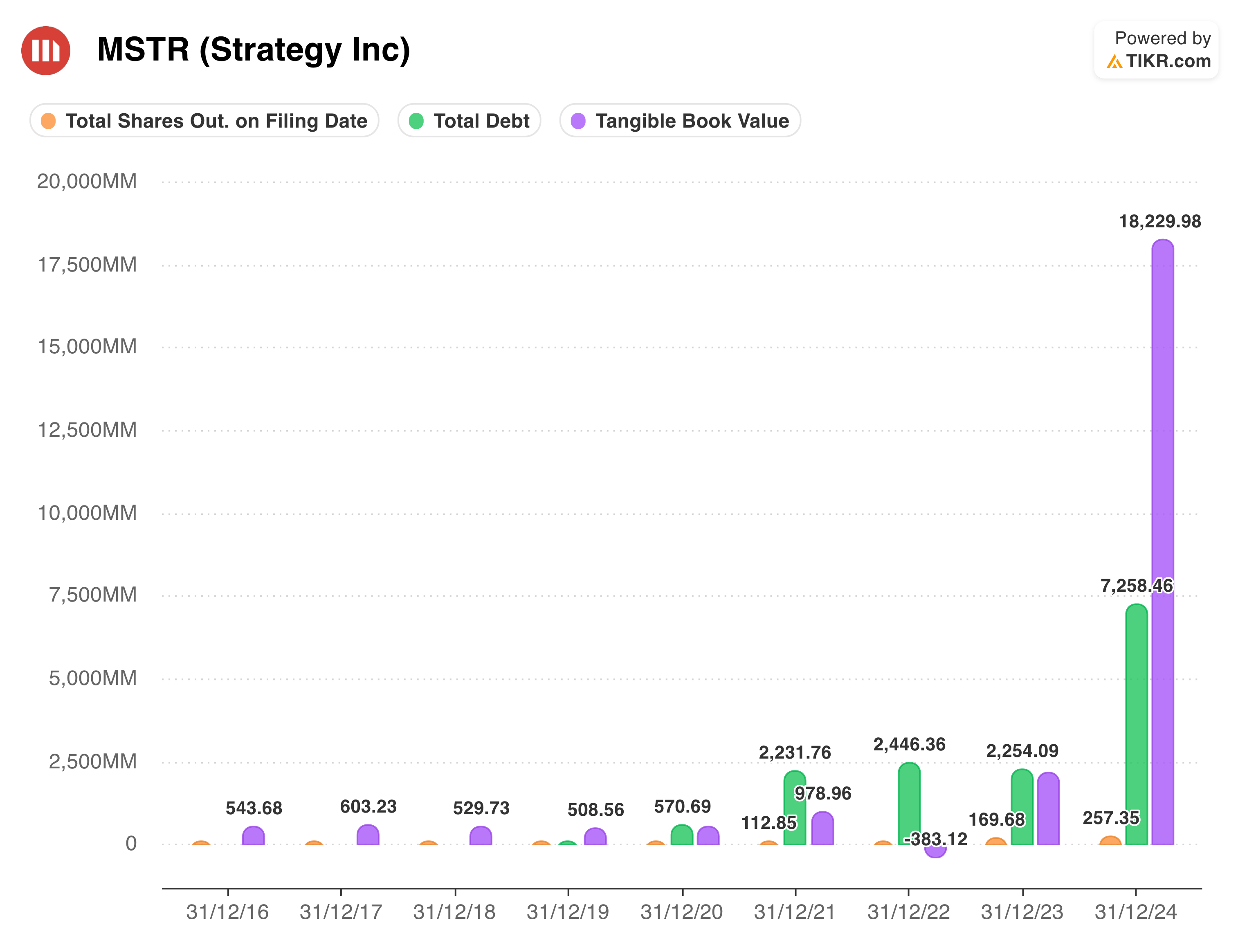

MicroStrategy (MSTR) has achieved growth in BTC holdings primarily through a clever kind of capital-markets alchemy via issuing debt or equity at premiums and using those proceeds to acquire more Bitcoin. Ingenious, perhaps. But not organic.

Its success is conditional upon the continued benevolence of the equity markets and newer investor participation in the operation. Given that new investors are not in infinite supply this is unsustainable and whilst the structure is favourable to existing shareholders every time new BTC is acquired, is is clearly less so for newer incumbents. The strategy now has expanded to debt financed acquisitions and yield products. It’s quite fascinating to watch MR Saylor adapt to the market.

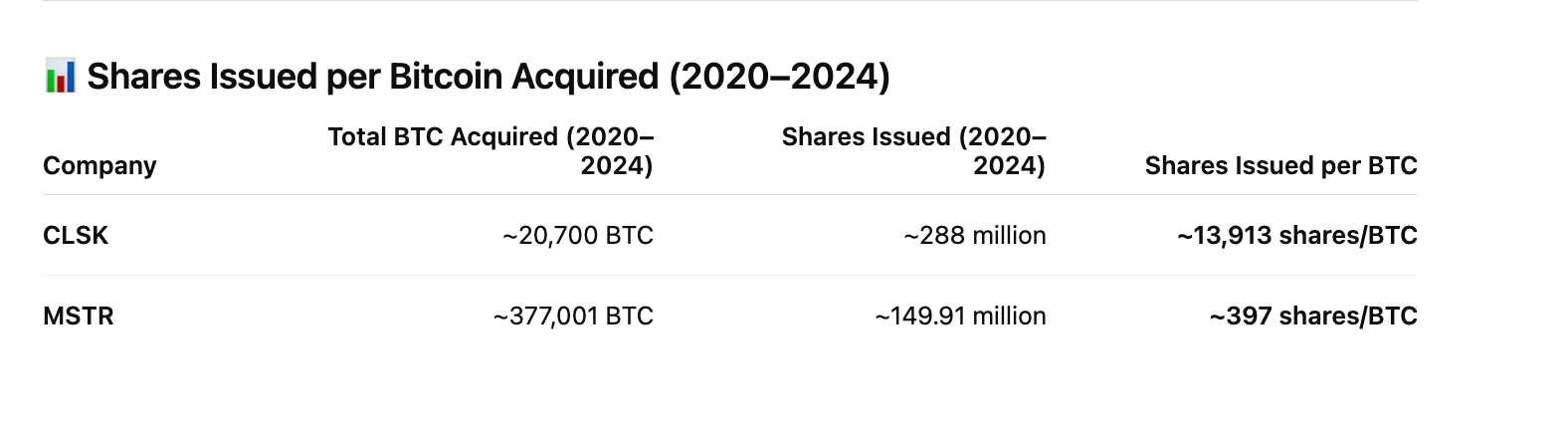

Comparing the two head-head.

So who, then, are the true Bitcoin treasuries - the ones that actually organically create coins from mining and compound the coins held on the balance sheet on a per share basis?

Let’s look closely at the two companies that, in my view, best embody this philosophy and what their balance sheets reveal about the future of the “debasement trade.”

It’s hard to believe they don’t have more press, especially when they just reported achieving an annualised return on capital of 80%..