The Royalty King Report | XP Inc. (NASDAQ: XP)

Brazil's Financial Disintermediation Engine — A Croupier Collection Candidate

The Royalty King Report

Buy-Side Research For The Croupier Collection

A new wave of investment interest in Brazil appears to be gathering momentum since 2025. Among the driving factors resides one most curious — Brazil is one of only two major nations in the entire globe currently offering a positive real interest rate (the other is Mexico).

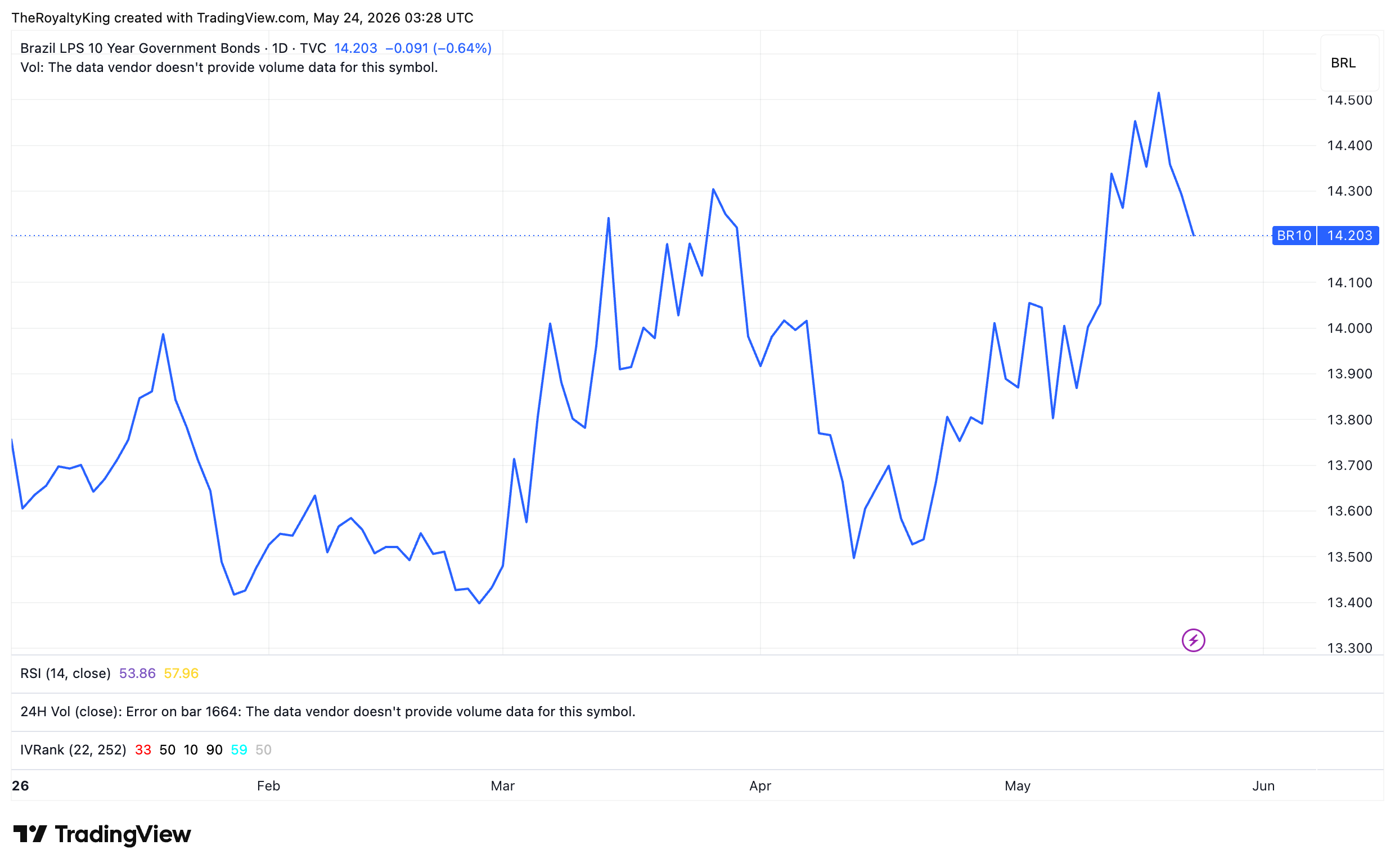

With an official inflation rate of 4.14% and the Brazilian 10 year yielding 14.29% that’s an unprotected real yield of circa 10% while an indexed bond, or Tesouro IPCA+, guarantees an inflation protected yield of 7.8% - albeit denominated in Reais.

Don’t forget to grab your ticket to the Rule Symposium below.

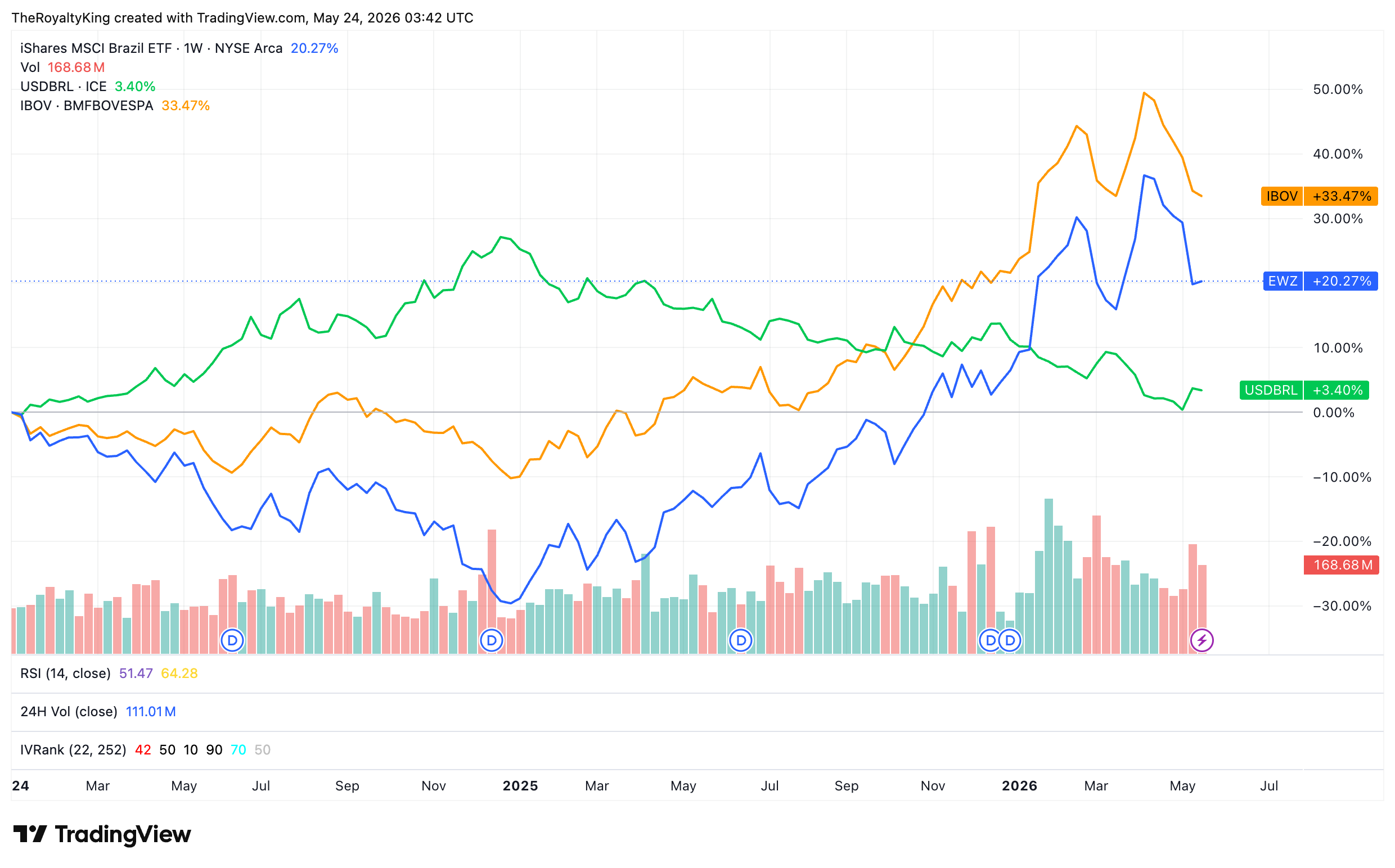

Brazil has featured many times and in various ways in this publication. Towards the end of the year 2024 I was particularly vocal about what I considered a highly compelling set up for those with a 2 year+ time horizon. The reasons were simple in that; a) The stocks had sold off heavily thanks to Government policy leading to a brutal drop in the local currency and b) Such circumstances were highly likely to improve in the event of a change of government in Brazil if only one had the foresight and patience to wait until the October of 2026.

Flávio Bolsonaro—son of former President Jair Bolsonaro—has closed a 23-point runoff deficit against the incumbent president Lula in four months, tying him in the March Quaest poll at 41%–41%. Prediction markets, which are often more reliable than polls, give him a 41% implied win probability versus Lula's 36%.

With Bolsonaro running on a campaign of fiscal conservatism the market would likely reward Brazilian stocks with a re-rating in the event he is victorious in October.

Rather than speculating on who will win the election, perhaps a more interesting question for investors is “how to gain investment exposure to Brazil’s promising growth story through vehicles that can survive and thrive regardless of who’s in government?”

That question can be answered simply via: Exchanges, brokerages and clearing houses who enjoy what I’ve dubbed positional or structural alpha.

The major Brazilian exchange is the Brasil, Bolsa, Balcão (B3), which is also likely to be the pre-eminent exchange exposure to Brazil, however foreign investors will need to apply for special trading permissions to purchase the shares.

Requiring no such extra step, is the subject of today’s piece and IMHO one of the most promising, quality business models in all of Latin America today. The business is best thought of as a combination of an exchange platform and ancillary wealth management and brokerage services. Or, if you prefer, Brazil’s version of Charles Schwabb. It is a financial marketplace that has compounded client assets at a 20%+ CAGR since 2020 while maintaining 30% EBT margins and is currently trading at an astonishingly cheap NTW free cash-flow yield of 29%.

The XP Story

XP inc. (for X-Perience) was born in Porto Alegre, May 2001 when founders Guilherme Benchimol and Marcelo Maisonnave set about addressing a conspicuous gap in the market: accessible, low-fee investment options for individual investors were scarce.

They began with an initial capital of around R$15,000, ($2,100 USD) and Benchimol personally contributed by selling his car and securing loans to fund the early stages of the venture. You love to see a good old fashioned bootstrapping as these owner-operator types tend to to outperform management of the ‘installed’ university-MBA types.

In the early days the company actually focused on financial education, creating courses and by 2006, the company ventured into asset management. In 2009 it expanded into insurance brokerage and in 2019 it successfully IPO’d on the NASDAQ at an implied Market Capitalisation of $14.9 Billion USD.

Quite the impressive journey for two Port Alegre lads who started with pocket change and a sold car!

Executive Summary

XP is a toll road on Brazilian financial disintermediation. It does not bet on markets, but rather collects a spread from R$1.53 trillion of client assets distributed through 18,300 advisors that competitors cannot easily replicate.

It operates across four segments: Retail (73% of revenue), Corporate Banking (17%), Institutional (7%) and miscellaneous (3%) that have the ability to feed each other and such a flywheel has enabled them to compound AUM at over 20% per annum since 2020.

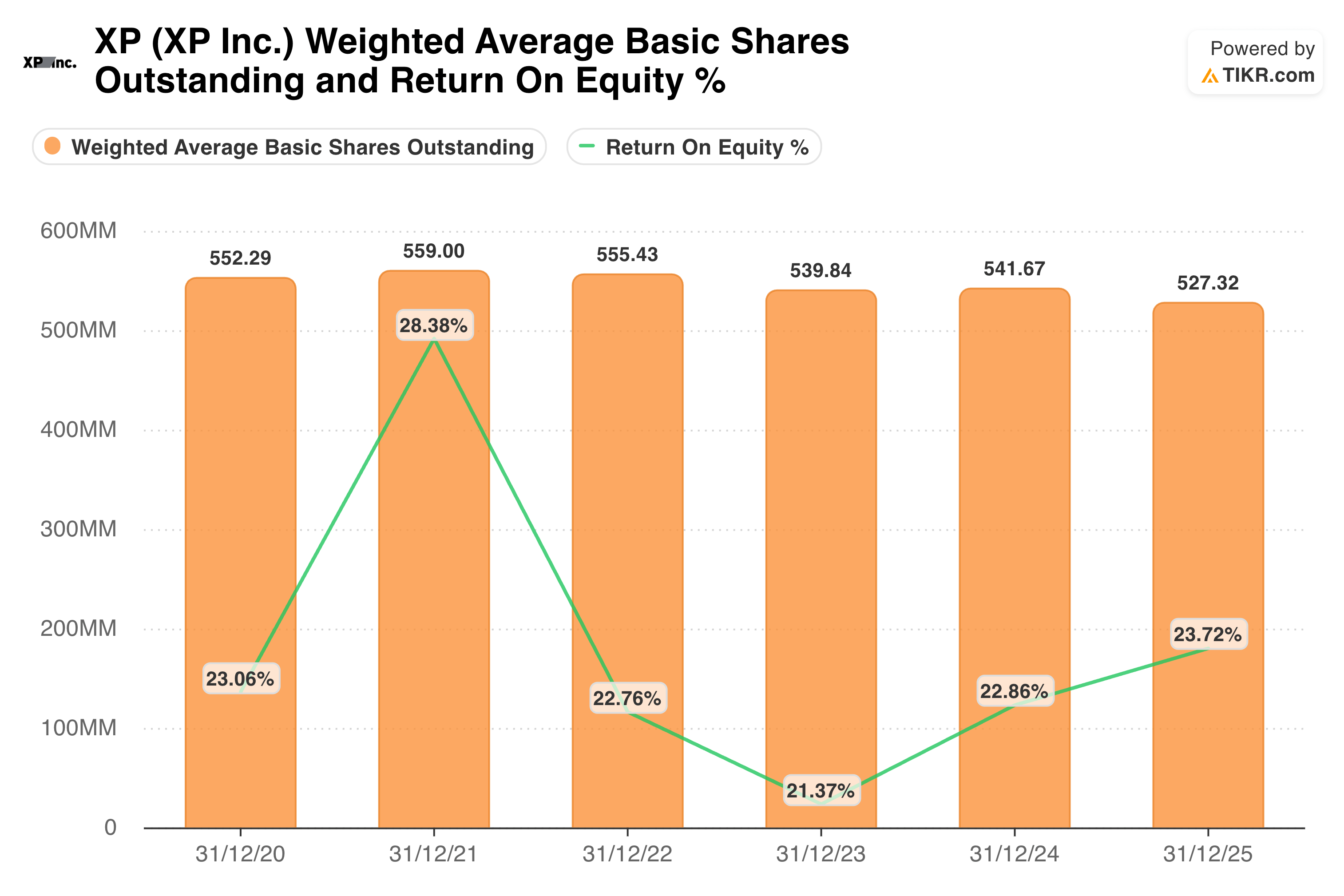

Over the same period it has also reduced its share count by ~1.3% per annum and has exhibited a return on equity (ROE) of over 21% in each year. A trend which is likely to continue.

Investment Thesis

XP is a croupier of Brazil's financial casino, collecting a fee on R$1.5 trillion of client assets at a structurally stable 22% ROE. It is available today at half its 2019 IPO price despite tripling the business. Its current 3x NTW FCF multiple is too cheap for a business of this quality with much potentially lucrative optionality embedded for free.

A price target of $20 is placed as a bear case with a bull case showing $81 should things go right in Brazil over the next 3 years.

Price targets are the analyst's own model outputs, not guarantees — they are subject to material uncertainty across currency, macro, political, and competitive variables, and should not be relied upon as the basis for any investment decision.

Business Model

XP is not a bank in any traditional sense. It is an open-architecture financial marketplace and analogous to what Charles Schwab became in the United States.

The five incumbent banks in Brazil have historically charged among the highest spreads and management fees in the world. XP's original value proposition was simple and extremely effective: give Brazilian retail investors access to better products at lower cost and distribute the relationship through an independent financial advisor (IFA) network that bypassed the bank branch entirely.

Two decades later, that proposition has evolved into a self-reinforcing ecosystem: Retail (73% of revenue) covers both investments and financial services, Institutional (7%) serving asset managers and banks, Corporate & Issuer Services (17%) operates as an investment bank and Other (3%) captures the trading results.

Interestingly, each segment feeds the others; corporate issuances end up on the retail platform, while institutional order flow improves retail liquidity and a growing card and credit book deepens client stickiness. This is not an easy eco-system to replace or compete with.

The advisor network is the distribution moat that matters most and the hardest to replicate. With approximately 14,000 IFAs spread nationwide plus internal advisors and wealth services teams, XP has effectively built a franchised distribution army that holds client relationships independent of the XP brand itself. This type of initiative is wonderful for creating compounding. An analogy might be drawn to Abacus life (ABX) —another holding in the croupier collection— and their acquisitions last year which turn them towards a vertically integrated fee-generator model.

In contrast to ABX however, whose current model centres exclusively around acquiring and packaging life insurance policies, XP offers a wide range of products and services from retail banking to large corporate lending and insurance.

Valuation

For A full valuation and methodology of how the price targets are calculated become a premium member today.