THE ROYALTY KING’S REPORT: MESABI TRUST

Royalty Research Series: Mesabi Trust | MSB

Executive Summary

Formed in 1961, Mesabi Trust is one of the purest commodity-linked financial assets available to public investors. It is also possibly the ‘cleanest’ example of the capital-light Royalty model with a pecuniary interest in a hard asset.

Since 2000, Mesabi Trust has produced over $509 million in cumulative net income while its market cap at the start of the period was only $39 million. Investors consequently recovered the entire equity value in five years. All further net income to an investor henceforth has been enjoyed for free, resulting in the holy grail of investing arithmetic: infinite ROI.

More astonishingly still, if such a feat is possible, is that an investor who invested in 2000 was doing so on the presumption of ~ 500 million tons of ore reserves. With the annual production level consistently around 4 million tons per year one would naturally expect the reserves to have waned to the vicinity of 400 million tons 25 years later. Yet, as it stands today, the reserves are estimated much higher at some 800 million tons.

This provides a superb illustration of the Royalty business:

No sustaining capital

No operating risk

No Dilution risk

No management risk

High-ROE, high-margin cash flow

Embedded volume and price optionality

Inflation tailwinds (royalties rise with nominal revenue)

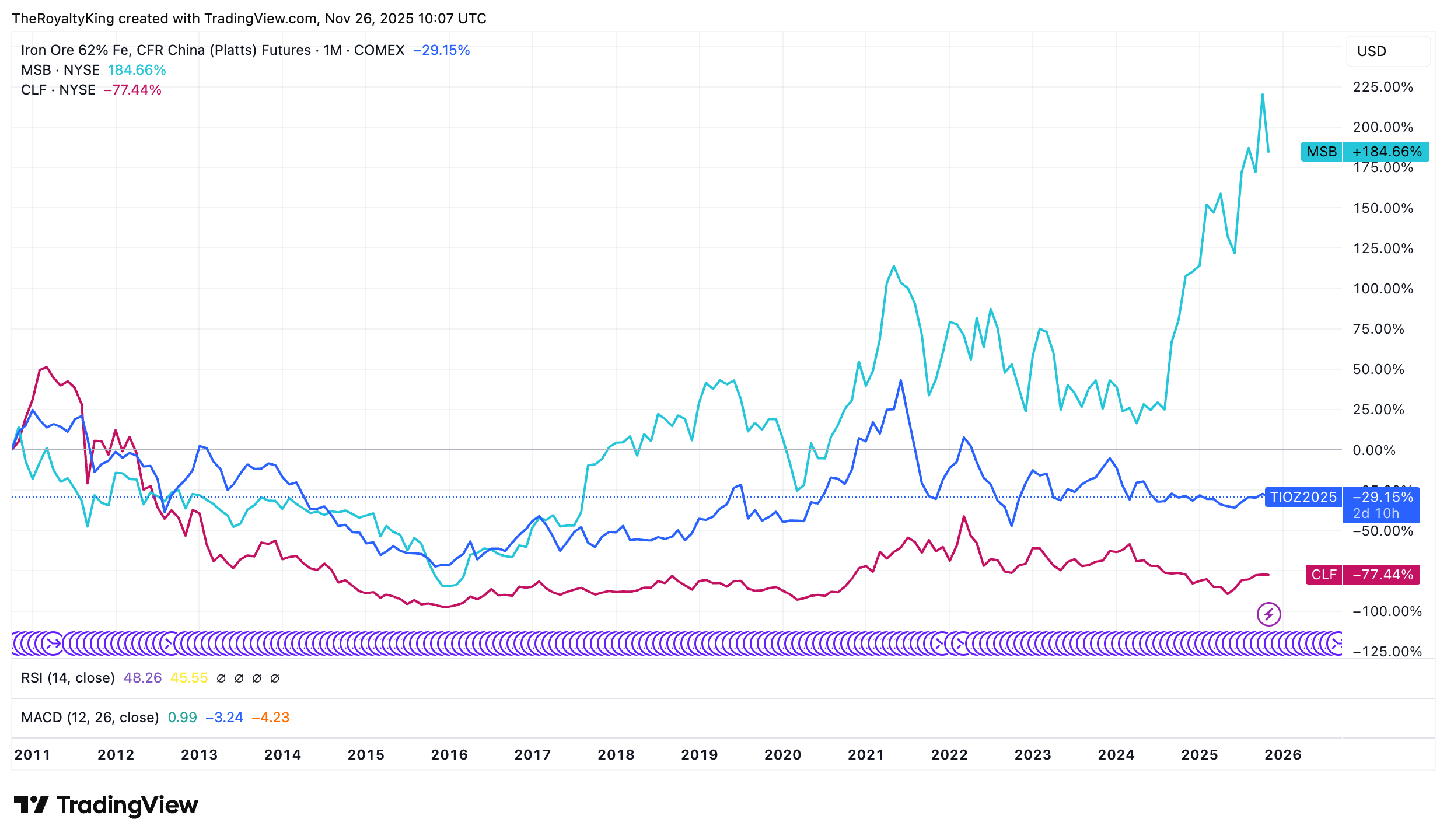

The superiority of the business model becomes apparent when comparing the performance of the royalty trust to the producing Co. CLF, and the base commodity itself.

Despite this record, the market continues to undervalue Mesabi because it misclassifies royalty trusts as short-lived wasting assets tied strictly to a single mine cycle. The reality is that the underlying ore body has hundreds of millions of tons of reserves, supporting decades of future royalty production, with practically zero operating expenses.

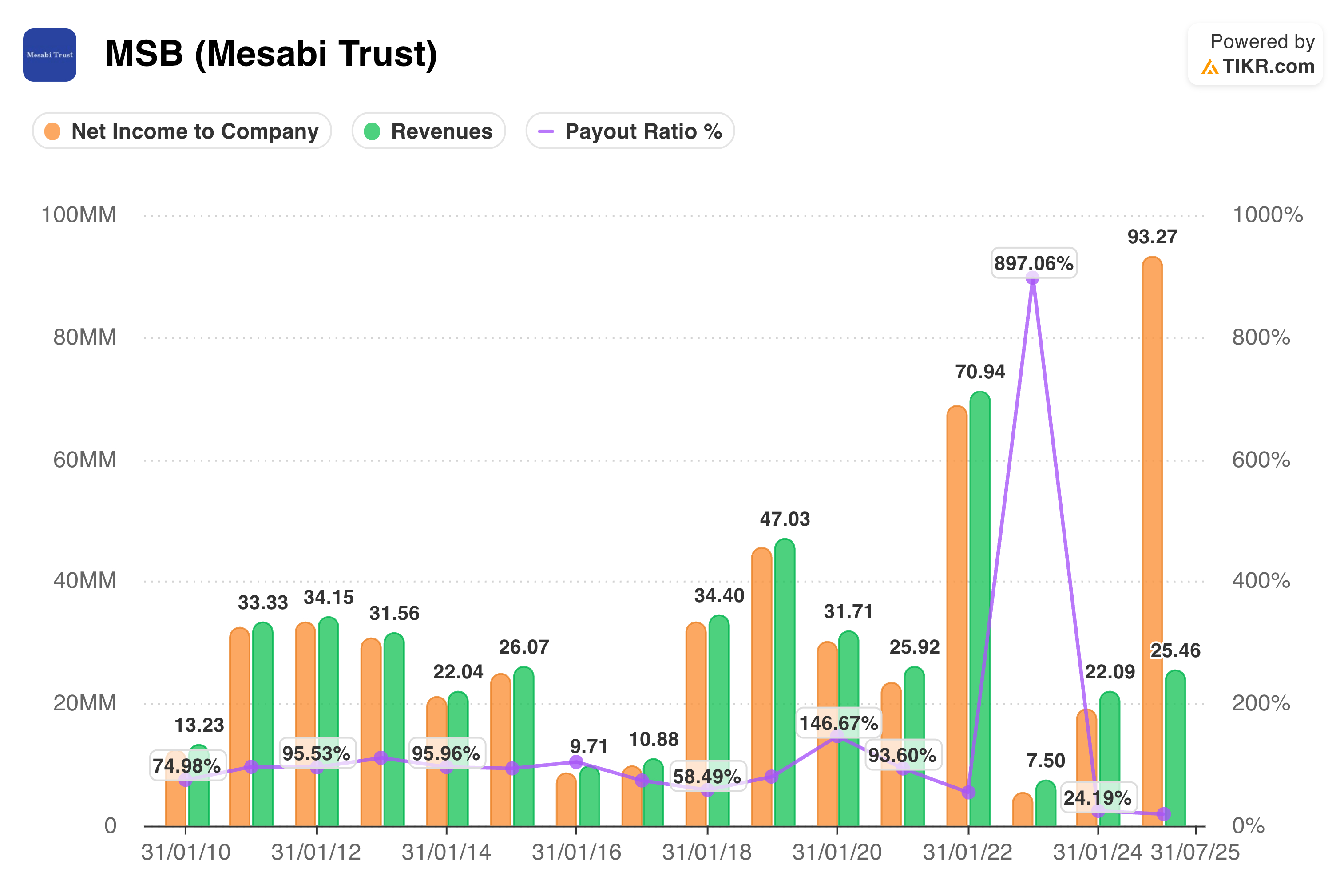

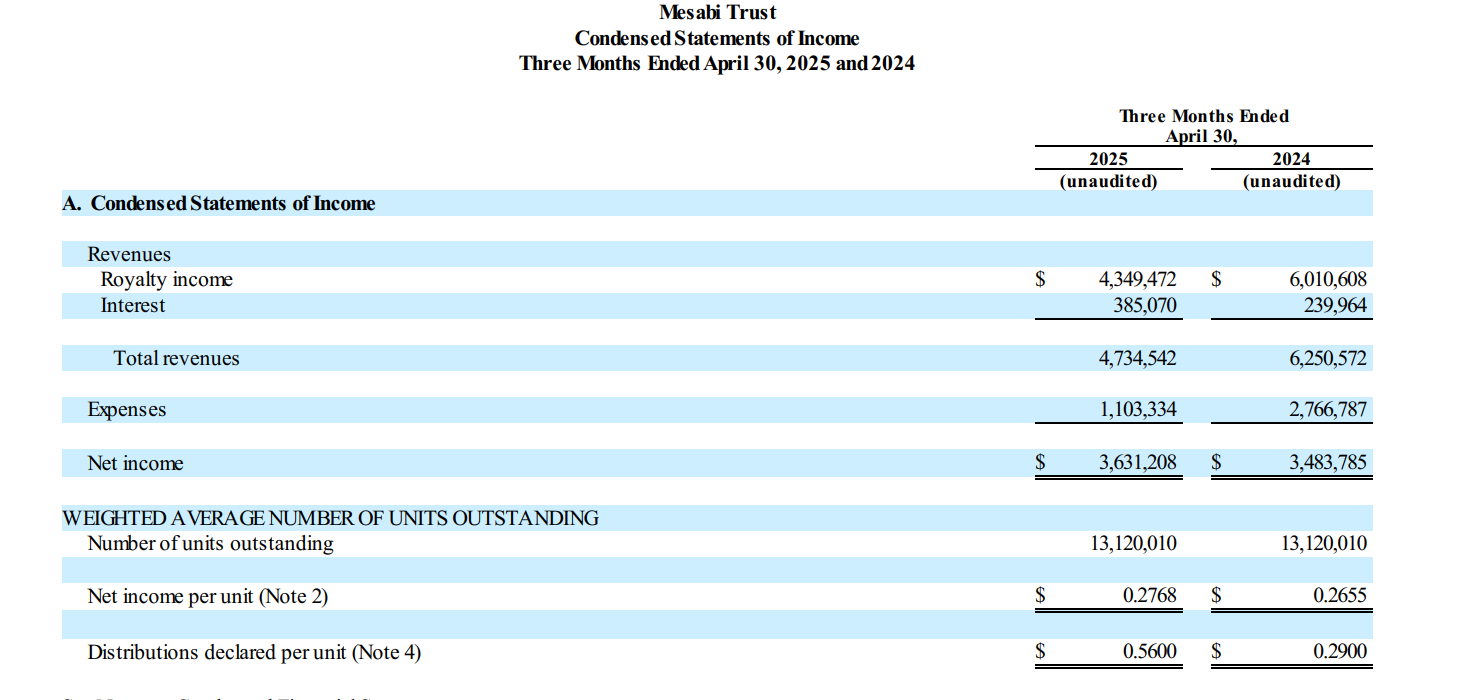

Recent distributions, especially the $93.3 million, $72 million of which was awarded from arbitration following a dispute with the parent of the operating Co: Cleveland Cliffs, demonstrate that Mesabi’s income claims remains extremely strong.

INVESTMENT CASE

The trust is simply an entity set up to hold the royalty rights and receive payments. It has no employees, no management nor is it permitted to undertake any business activities outside the trust’s mandate for receiving payments. Ergo, it is neither subject to shareholder dilution nor management mis-allocation of capital. It’s payments are a function of production volume*price for iron produced on its acreage. This structure is key to explaining its revenue growth without commensurate expenses - there are no expenses! (Save de minimus filing and administrative charges).

It is a rare example of a true inflation beneficiary whose performance inclusive of dividends has outperformed even gold’s run over the last 15 years - not bad for a stock involved in a cyclical, industrial commodity.

Additionally, situated inside the USA makes it a beneficiary of any Tariff policy and an indirect beneficiary of the National Security Spending contracts awarded to Cleveland Cliffs. CLF states its first of such contracts is valued at $500 million over 5 years.

The valuation section will show a model for the trust’s likely range of income in detail. In brief, conservative assumptions at today’s price and volume put net income at ~$30 million annually or a 7.5% yield protected from inflation. Upside optionality on increase in price and volume thanks to the trusts sliding scale royalty is embedded for free as of today.

OPERATIONS

In Mesabi’s case that asset is a single Iron Ore deposit, the Peter Mitchell Mine located in Babbitt, Minnesota, at the eastern end of the Mesabi Iron Range.

Unlike miners, who must constantly reinvest, manage labor, battle cost inflation, and cycle through debt Mesabi is a zero-capex trust. which receives a contractually defined royalty on iron ore shipped from Cleveland-Cliffs who operate the mine.

It does NOT:

Mine

Operate

Employ workers

Maintain equipment

Borrow

Reinvest

Mesabi is a financial conduit: it collects cash and distributes it.

This makes it closer to a natural resource bond with equity upside than an operating business.

Reserves & Life-of-Mine

While the trust itself does not publish reserve estimates, Cliffs’ independent 2021 TRS lists:

Proven ore: 303M long tons

Probable ore: 519M long tons

Total: 822M long tons crude ore

Production volumes at today’s level imply its life of mine could continue for another 100 years or more.

History & Cash Flow Through Cycles

If one examines the historical prices for iron ore in the period above it is important to note that the trust maintain positive earnings paid out to shareholders while the commodity itself experience a sharp decline culminating in a nadir of $40/t in 2016 or a 70% brutal drawdown.

A Tale Of Two Business Models - Earnings Power

The most common objection to royalty and streamers by far is the price. Although it’s usually mistakenly referred to as valuation - which will be explored in the next section.

Royalty assets have the unusual quality of paying for themselves many times over, despite appearing optically expensive at the outset.

Before continuing however it’s important to remark on putative earnings vs shareholder’s earnings.

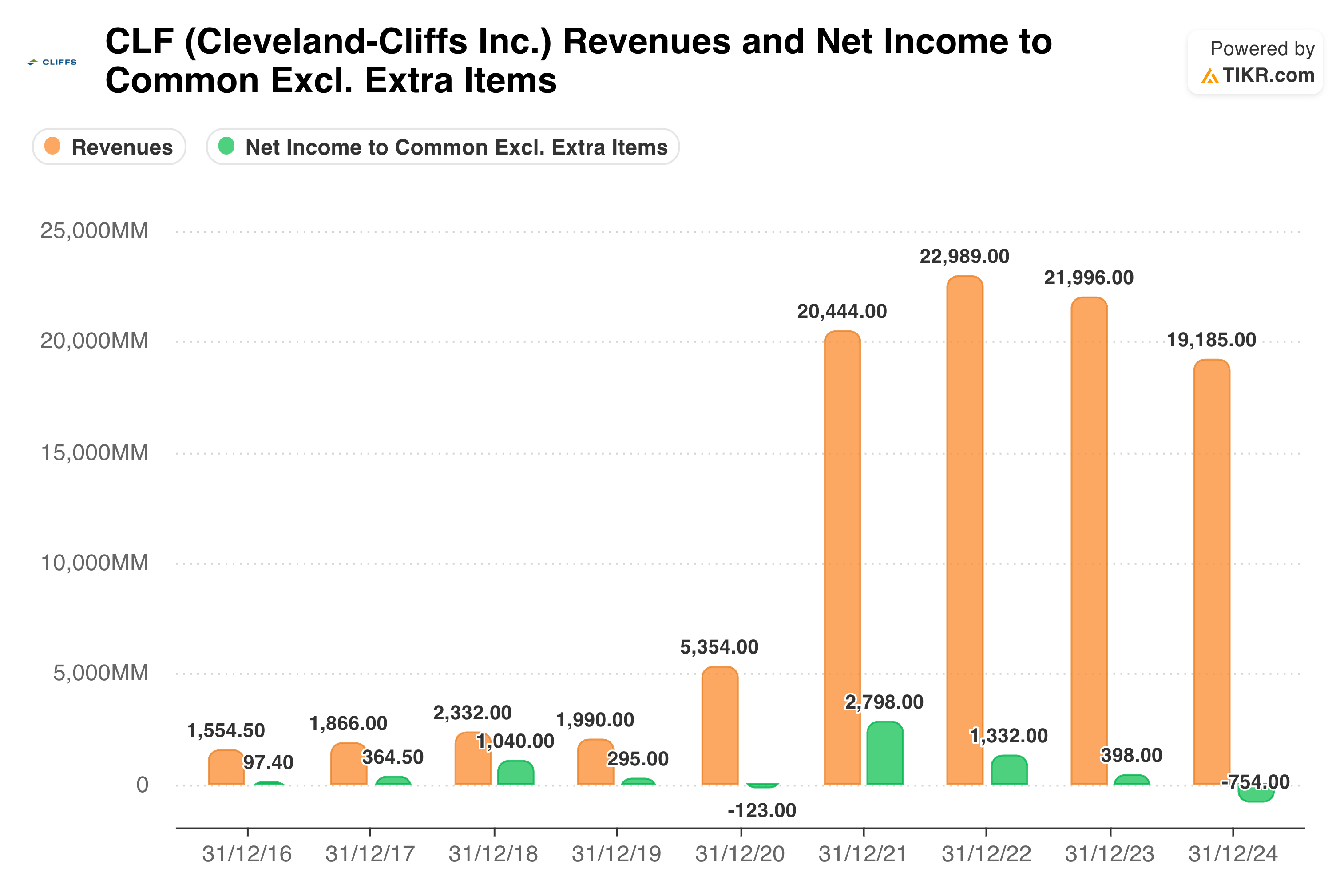

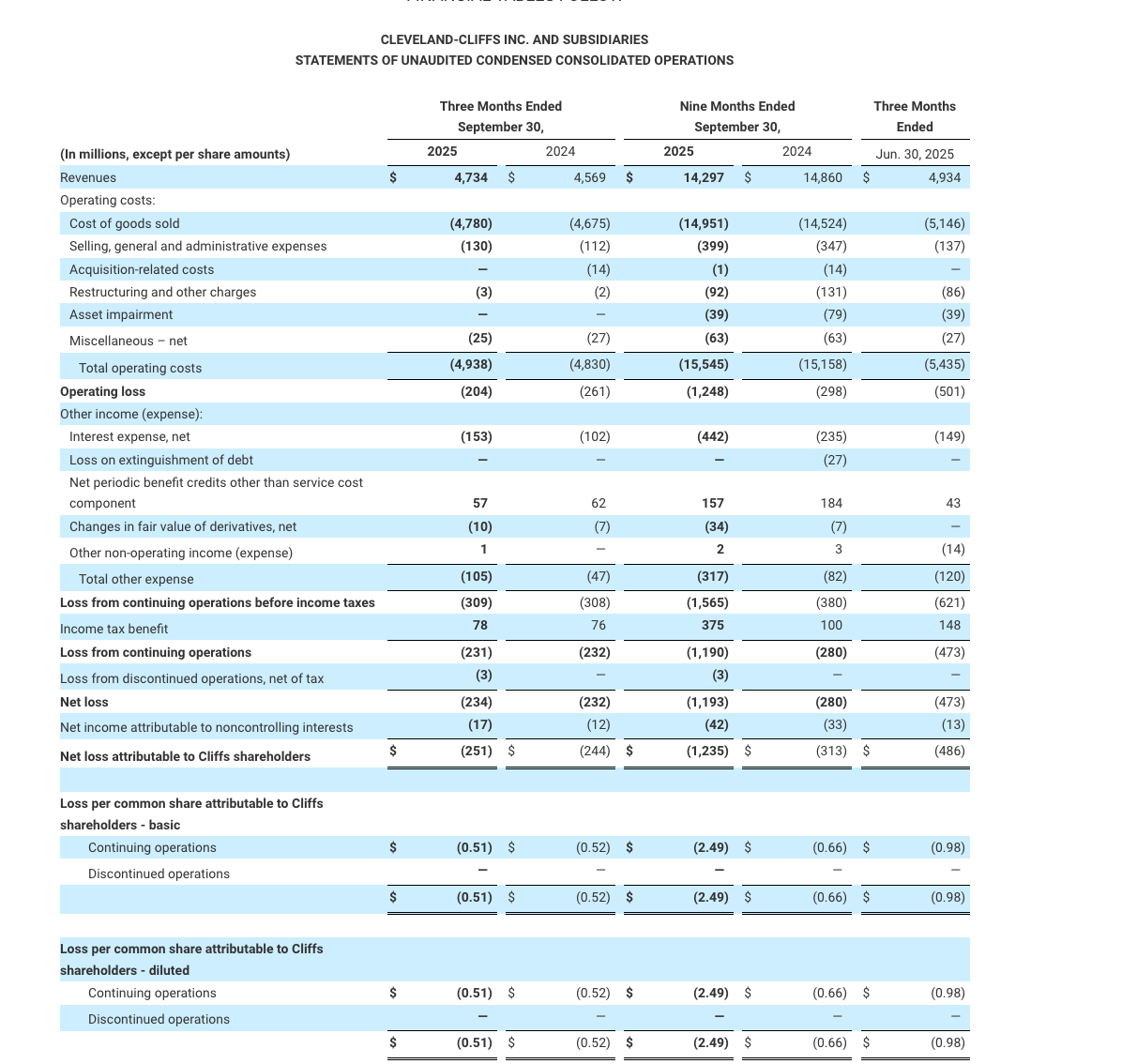

An operator company might report a hypothetical $8 of earnings and ostensibly trade at 8x earnings or a P/E of 8 for a stock price of $64. However, secondary sources cite that such business models frequently require retaining 75% of said earnings to simply continue operations, thereby leaving only $2 to be distributed to shareholders and as such it might be more appropriate to say the OP CO. is trading at 32x available earnings.

In this case of CLF, in the most recent year where net income was positive (because there are years when it is negative) the conversion of Revenue to net income was an anaemic (the pun proves irresistible when speaking of an Iron company) 1.8%.

This is to say that quantitative analysis as to putative earnings used in PE comparisons fails to tell the whole story and should be overlayed with a qualitative consideration of the underlying business model itself.

Comparing the distance between the top line and the bottom line in the case of these two companies speaks volumes.

Versus

In a world of monetary inflation and rising nominal commodity prices, royalty assets quietly compound because they have no mechanism through which inflation can injure their economics. They possess revenue, never cost.

Risks

Any disruption to production or weakening price environment will result in lower royalty payments for the obvious reason that said payments are a product of Volume * Price.

Disputes have arisen at times between the operator and the trust in regards to payments. Mesabi has won arbitration hearings and been awarded any royalties the Op Co has attempted to repudiate plus damages and the agreement actually provides Mesabi with the senior claim on the asset territory itself meaning, should the operator bankrupt, Mesabi retains their interest which is simply inherited by the incumbent.

The main risk is volatility of distributions, not permanent impairment.

Valuation

Such an asset can be valued by considering its likely future cash distributions using a Net Present Value (NPV) calculation.