The Toll-Booth to the Asian Century

The Royalty King's Report: Hong Kong Exchanges & Clearing - A Royalty On Economic Activity In Asia + The London Metals Exchange

A clear tendency toward royalty and streaming companies has long shaped the identity of this publication. The preference for them expressed here is hardly accidental. Their attraction lies in the architecture of the model itself: a structure that participates in rising volume without the encumbrances of capex, operating leverage, or the cyclicality that turns producers into price takers. This eventually and inevitably turns said producers into wealth destroyers given that, to paraphrase the great Doomberg, the real price of most commodities drifts downward over time. A business that thrives in spite of that tendency is, by definition, unusual.

It is now time to explore another business model that deserves equal esteem yet has received far less attention here: securities exchanges and clearing houses.

In brief, I view them as royalties on the entire economic activity of a nation or economic sub sector.

Today’s report begins with broad remarks on exchanges as a category, then moves to the rationale for using them as primary vehicles for “emerging market” exposure. In reality, many of these markets are only emerging in Western perception because when observed through the lens of economics they collectively represent the majority of global trade. Asia is the core focus, while South America will be left for future pieces as it is my second home and already well understood territory.

Premium readers will then find a more formal research report on Hong Kong Exchanges & Clearing (HKEX), an instructive case study that illustrates how exchange businesses capture economic growth more reliably than individual equities or index ETFS.

Just as previous work has shown the superiority of the royalty model relative to capital-intensive operators, this new series will illustrate how exchanges offer a purer, more reliable means of owning a nation’s economic activity. This compounds quietly, almost imperceptibly, over time as it provides asymmetric exposure to economic activity without constant operational reinvestment. Consequently this model outperforms index investing in almost all historic examples.

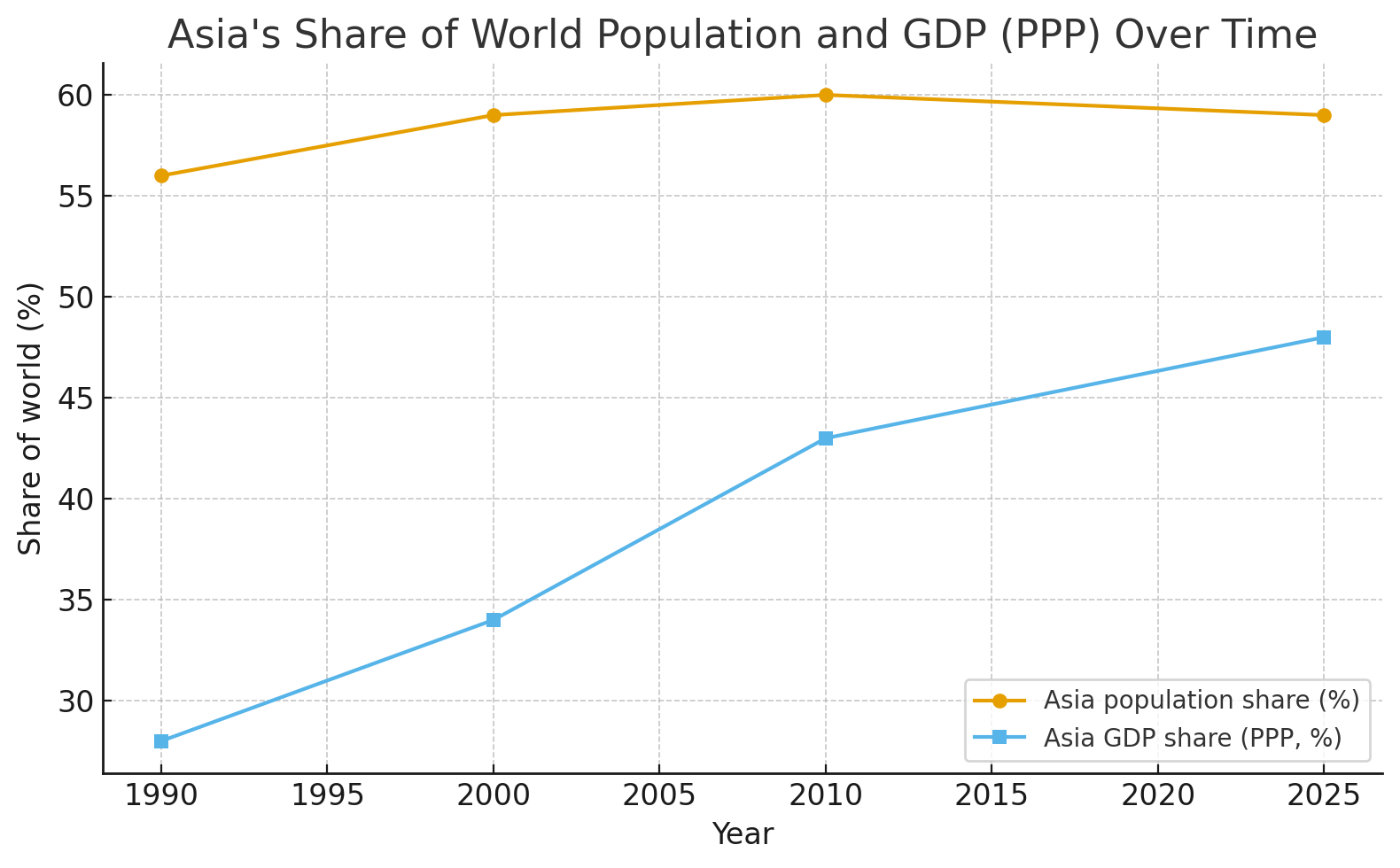

A conspicuous gap remains in the portfolios I manage: meaningful exposure to Asia. It is an omission difficult to justify when the region accounts for roughly 4.8 billion people or about 59% of the world’s population with a collective GDP of $41.5 trillion. Measured on a purchasing-power parity (PPP) basis, that figure rises to nearly $94.7 trillion, or close to half of global economic output. A region of that scale cannot be treated as peripheral; it is, in many respects, the economic centre of gravity.

For years, I’ve intended to gain deliberate exposure to Chinese and the broader Asian economic expansion, but without anchoring that exposure to the fortunes of any single company. The fate of Alibaba underlines how swiftly a dominant firm can become vulnerable to forces entirely outside an investor’s control. Nor is the risk of being “Gazprommed” overstated; in periods of geopolitical tension, it remains a non-zero probability.

Many investors express their Asian allocation through tech-heavy ETFs. That approach, however, concentrates exposure precisely in the sectors most subject to margin pressure, regulatory variance, and capital intensity. The preference here is for a structure that reflects the entire underlying economic activity, not just one sector and which does so through a capital-light, high-margin model.

Hence the conclusion: exchanges and clearing houses. They provide exposure to a region’s economy without requiring a thesis on which companies will win. Much like royalties outperform operators across a commodity cycle, exchanges often exceed the returns of the very indices built upon their listings.

They achieve this through a simple structural truth: an exchange monetises activity and product expansion, not outcomes.

Every listing, every trade, every derivative contract, every margin call, every settlement (regardless of profit) passes through the same tollbooth. Market expansion, volatility, foreign participation, derivative growth, and even modest fee adjustments all accrue disproportionately to the exchange. Their related indices, in contrast, suffer cyclical noise and charge fees whose long term impact is significant to any value that might be expected to accrue to a shareholder on a per share basis.

Put simply, rather than pay fees, the preference is to collect them.

A non-exhaustive list of the advantages which compound quietly in these businesses:

Rising trading volumes

Growth in listings and IPO cycles

Expansion of derivatives markets

Volatility spikes that increase turnover

Foreign capital inflows

Indirect participation in GDP growth

Pricing power embedded in fee structures

High operating leverage on fixed infrastructure

Indices, by contrast, do not benefit from volatility or turnover nor do they reliably reflect the full breadth of a nation’s economic output. Exchanges do a much better job. They are, in many respects, the purest and most durable way to participate in Asia’s (or any other region’s) economic ascent without the fragility of stock-specific risk.

Consequently, exchanges will serve as the preferred vehicle for gaining exposure to Asia. The portfolio already holds the majority of the major venues discussed earlier, with the exception of LSEG, as well as the Philippine and Hellenic exchanges. In addition, the Mexican exchange: La Bolsa Mexicana de Valores has been included for some time. Upon arriving in Buenos Aires next week, a local account will be opened expressly to acquire shares of Argentina’s national exchange, BYMA, a business that remains almost implausibly cheap in terms of valuation.

The focus today, however, is Hong Kong Exchanges & Clearing (HKEX), a particularly instructive example of how an exchange can function as a gateway to an entire region’s economic momentum.