TRK Report | Japan Exchange Group, Inc. (8697 JP)

Owning the Repricing of a Re-Emerging Market

Another One to The Croupier Collection.

Recent market action has served as a reminder of something investors tend to forget during long, orderly trends: volatility is not an aberration — it is the market’s native state. When assets as large and liquid as Microsoft or gold can experience 8–10% daily swings, it behooves investors to focus less on being “right” on direction, and more on business models positioned to benefit from trading activity itself, regardless of price direction.

As my friend James Davolos is fond of saying, “business models matter” and perhaps the most resilient models centre themselves on collecting a fee on volumes.

The exchange model exhibits this by collecting fees on the volume of transactions taking place in their given domain. Regardless of whether prices rise or fall, the exchange clips the ticket on volume, turnover, listings, delistings, restructurings, and even on products reflecting volatility itself.

This is why some of the most experienced macro investors have consistently gravitated toward exchanges as a preferred form of exposure, particularly in emerging markets undergoing transition. Both Rick Rule and Jim Rogers have spoken over the years about their preference for owning the infrastructure of markets rather than the markets themselves, at least initially. The logic is simple: when capital floods in, the exchange benefits; when capital exits, the exchange still benefits; and when markets restructure or reprice, the exchange often benefits most of all.

Japan now fits squarely into this framework.

Long dismissed as a stagnant, fully priced, post-growth economy, Japan is instead revealing the characteristics of a ‘re-emerging’ market. After a multi-decade balance-sheet reset, the country is experiencing a slow yet persistent rise in governance reform, shareholder accountability, foreign participation, and corporate activity. Importantly, these changes do not require heroic GDP growth to matter. They require capital to move, incentives to realign, and markets to re-engage.

In that environment, particularly in a country and culture with which I am unfamiliar, the safest way to gain exposure is not by attempting to select future winners within the market, but by owning the platform through which the entire market operates and likely undergoes a repricing.

That platform is the exchange.

Japan as a “Re-Emerging” Market

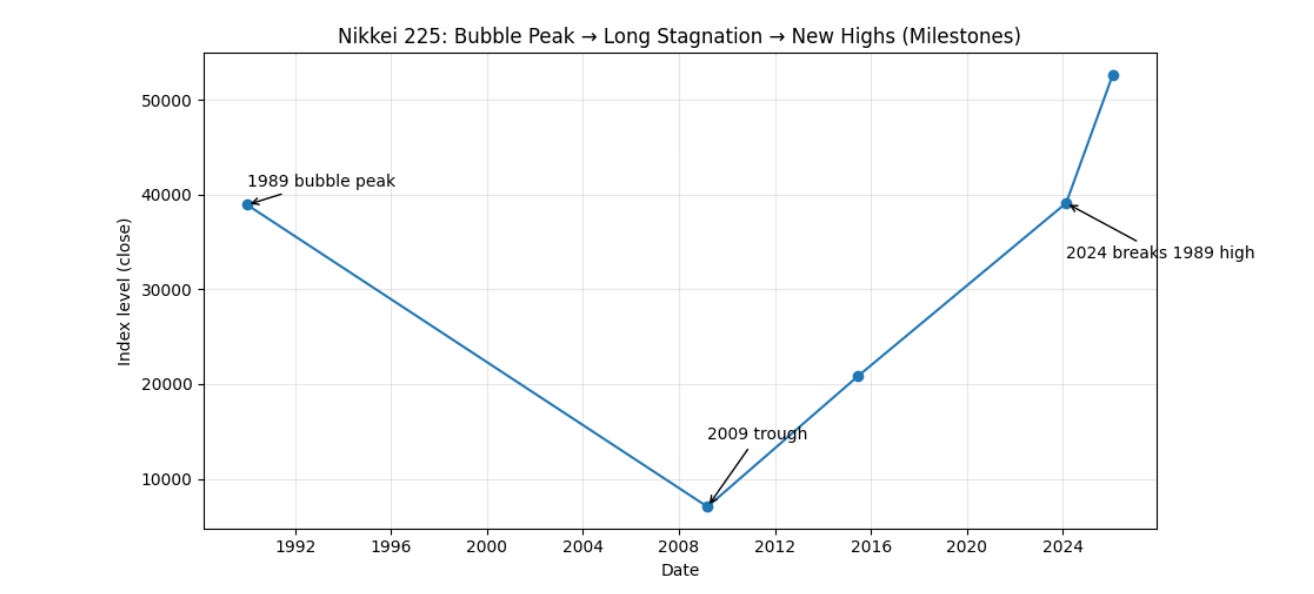

Japan’s economy has been famous for its decades-long stagnation. The most telling evidence is not economic growth, but time. Japan did not reclaim its 1989 equity market capitalisation peak until 2024, a 35-year reset with few historical parallels.

During this period, Japan’s relevance in global equity benchmarks collapsed. At the height of the asset bubble, Japanese equities represented approximately 37% of global market capitalization, more than double the country’s share of global GDP. Today, Japan accounts for roughly 4.9% of global equity indices, despite remaining the world’s fourth-largest economy.

What differentiates the current environment is that reform is no longer discretionary. Over the past decade, governance changes have been enforced in what has historically been a very opaque corporate environment. A few to note:

Companies with explicit shareholder return targets expanded from roughly one-third to two-thirds of the market

Shareholder Transparency (2025-2026): Amendments to the Companies Act aim to uncover beneficial owners behind nominee accounts, strengthening the Large Shareholding Reporting Rule to ensure better transparency on ownership.

Takeover Bid (TOB) Rule Enhancements: Rules are being amended to require, for example, the justification of offer prices in M&A deals to better protect minority shareholders.

These appear to constitute a structural rewiring.

Royal Rumination: What if Japan is not “cheap” because growth is weak; it is under-owned because its capital markets spent decades prioritising stability over returns and now that is being reversed?

Why Not Just Buy The Index?

If Japan is being structurally repriced, broad equity indices are an inefficient way to capture that process. Not only because exchanges usually outperform an underlying index as explored in these two pieces:

but also because the Nikkei or ETF: EWJ doesn’t really represent Japan’s domestic economy as well as one might expect.

EWJ holds only 183 companies out of nearly 4,000 publicly listed Japanese firms. Of those holdings, the top 50 account for roughly two-thirds of the fund, leaving the vast majority of the domestic corporate ecosystem underrepresented.

Therefore, perhaps 95% of Japan’s listed companies are effectively not represented in the index.

This matters because index construction systematically biases exposure toward large, multinational exporters, whose revenues, and capital allocation decisions are often more reflective of global conditions than domestic reform. Yet the aforementioned changes currently reshaping Japan are occurring across the system, not merely within the largest constituents.

As a result, index exposure might more accurately capture Japan’s past, rather than its present transition. The repricing is broader than the index, yet the index cannot expand to reflect it without first being pulled forward by the very activity it excludes.

Japan Exchange Group Inc. TYO: 8697, JPXGY

When a market is being structurally rewired, the most reliable way to gain exposure is not by attempting to select beneficiaries within the system, but by owning the infrastructure through which the entire system must operate.

This is why JPXGY becomes the preferred expression of the Japan thesis, at least from The Royalty King’s point of view.

JPXGY is not a bet on which companies improve governance fastest, nor on which sectors lead the next cycle. It is a royalty on Japan’s capital re-engagement itself. As Japan transitions from a market defined by inertia to one defined by participation, JPXGY monetizes the change regardless of direction, sector leadership, or narrative.

Historical Context: Why Japan Is Different

Japan occupies a unique position in economic history. It is the only country to transition from feudal society to industrial economy to global power without being colonized.

It is also notable that Japan was a primary contributor to the legendary long-term performance of the original Templeton fund.

Templeton allocated aggressively to Japanese equities through his global funds, long before Japan entered global benchmarks.

Outcome:

Over roughly 20 years (1960s–1980s), Japanese equities compounded at approximately 15–20% annualised

Japan became the single largest contributor to the long-term performance of the Templeton Growth Fund.