Wheaton Precious Metals

WPM — TSX / NYSE | The Royalty King Report | March 29, 2026

If you prefer printing and reading a physical copy (as I do) then check out this word document.

Executive Summary

Wheaton Precious Metals provides high-quality, low-risk exposure to precious metals through its streaming portfolio — approximately ~67% gold, ~33% silver by revenue, giving investors meaningful silver optionality alongside gold exposure. All production figures are expressed in Gold Equivalent Ounces (GEOs), which converts silver and other metal production into a gold-equivalent weight using prevailing spot prices.

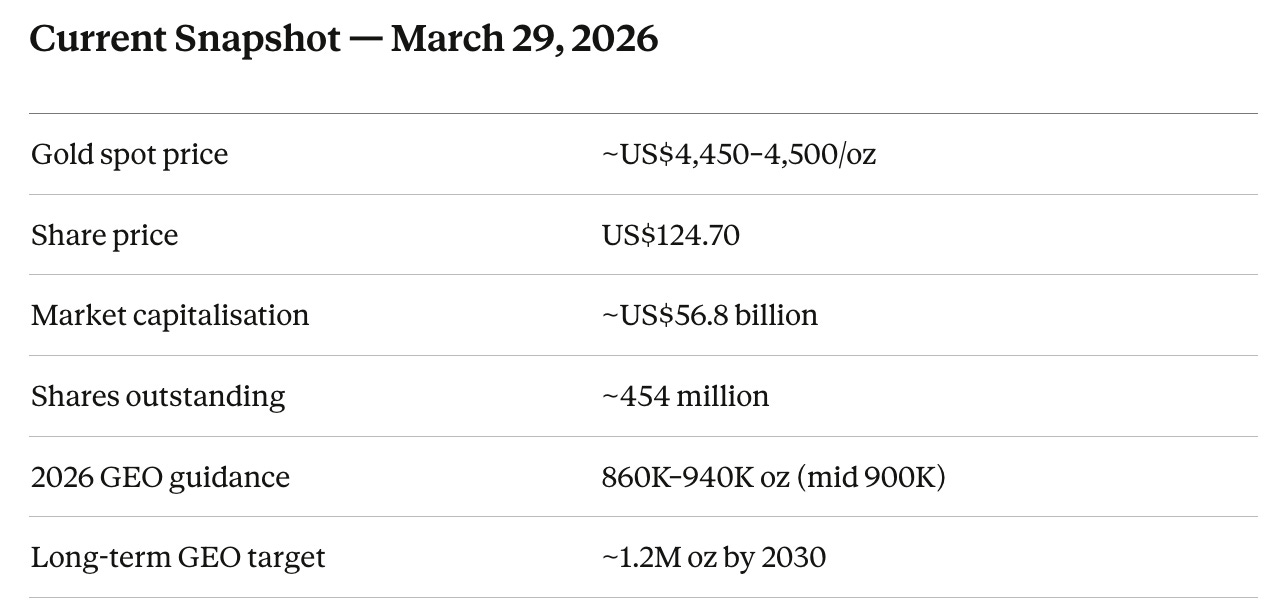

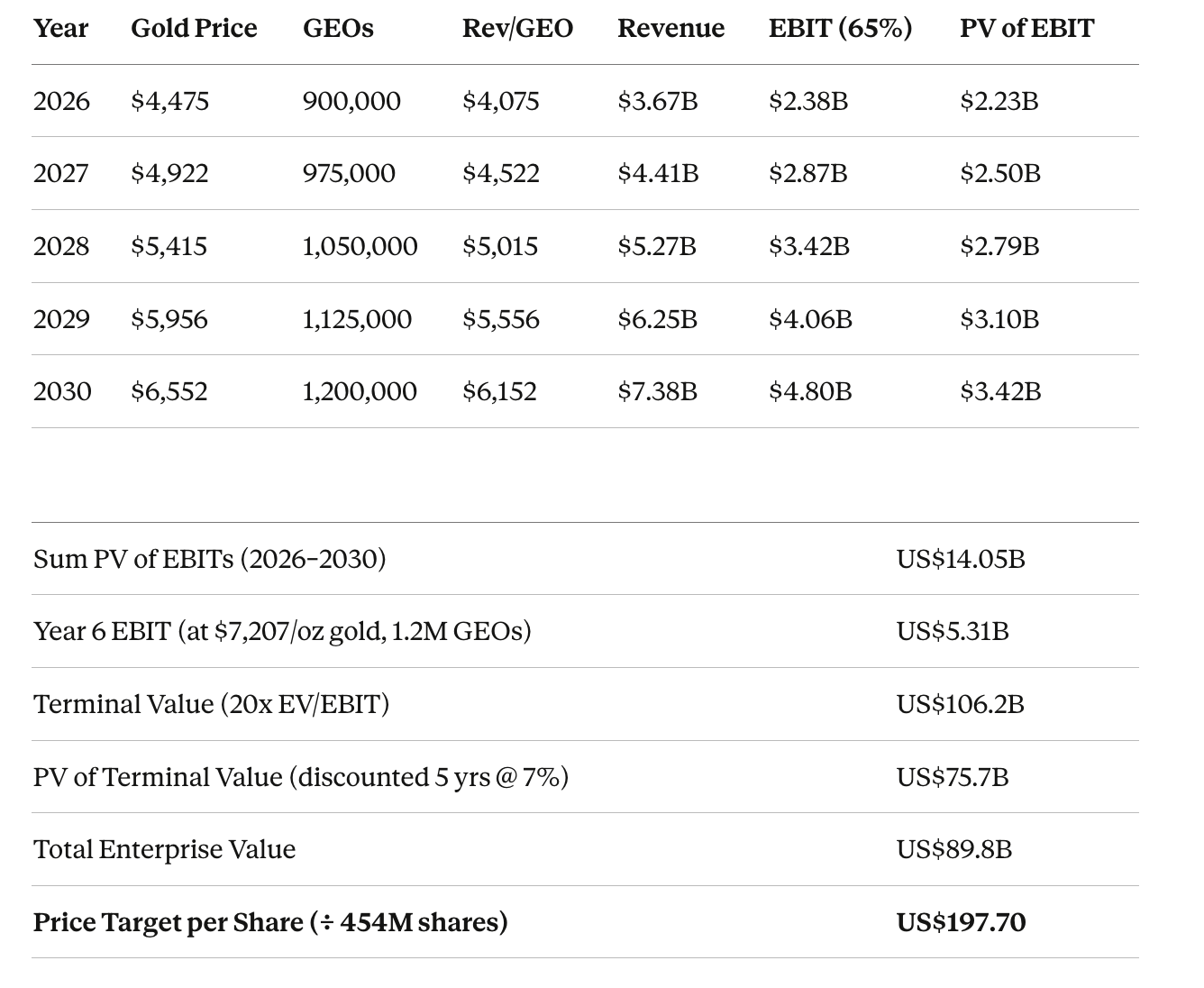

At the current gold spot price of approximately US$4,450–4,500/oz, my estimated price target is US$140–160. In my base case with gold reaching US$6,000/oz by 2029 and sustaining elevated levels thereafter, the 5-year DCF produces a price target of US$197.70, implying 58.5% upside and an ARR of 11.1% per annum from the current share price of US$124.70.

The streaming model delivers high margins due to fixed low delivery costs, no direct mining capex, and strong operating leverage to metal prices. Incremental revenue at higher gold prices flows almost entirely to free cash flow. WPM's ~33% silver revenue mix means GEO figures will fluctuate with the gold/silver ratio, and a rising silver price relative to gold provides an additional tailwind to reported production.

Price Target Scenarios

The standard PE multiples and even run-rate DCFs are not particularly good valuation methods for Royalty & Streaming companies however in the interests of brevity and simplicity I’m going to bend the rules here and use a modified DCF given we have good line of sight for WPM’s production profile over the next 5 years. Applying a terminal multiple will attempt (probably poorly) to account for the long mine life Wheaton enjoys and the ‘right tail’ optionality.

This methodology likely does not fully represent the full life-of-mine value of the royalty portfolio or the out-of-the-money optionality — both of which represent additional upside not captured in these figures. The numbers are deliberately conservative.

5-Year DCF Build — Base Case

I’m underwriting:

Production ramps linearly from 900K GEOs (2026) to 1.2M GEOs (2030).

Gold price grows at 10% per year from a US$4,475/oz base.

Delivery cost fixed at US$400/GEO. EBIT margin 65%.

Discounted at 7%.

Terminal value applied at end of Year 5 using 20x NTM EV/EBIT on Year 6 projected EBIT.

Terminal value dominates total EV — this is typical for long-duration royalty businesses where the value of decades of future royalty cash flows sits beyond the 5-year forecast window. The DCF is intentionally conservative: OTM royalties converting to production, new stream acquisitions, and silver outperformance represent additional upside likely not captured at only a 20x Exit multiple.

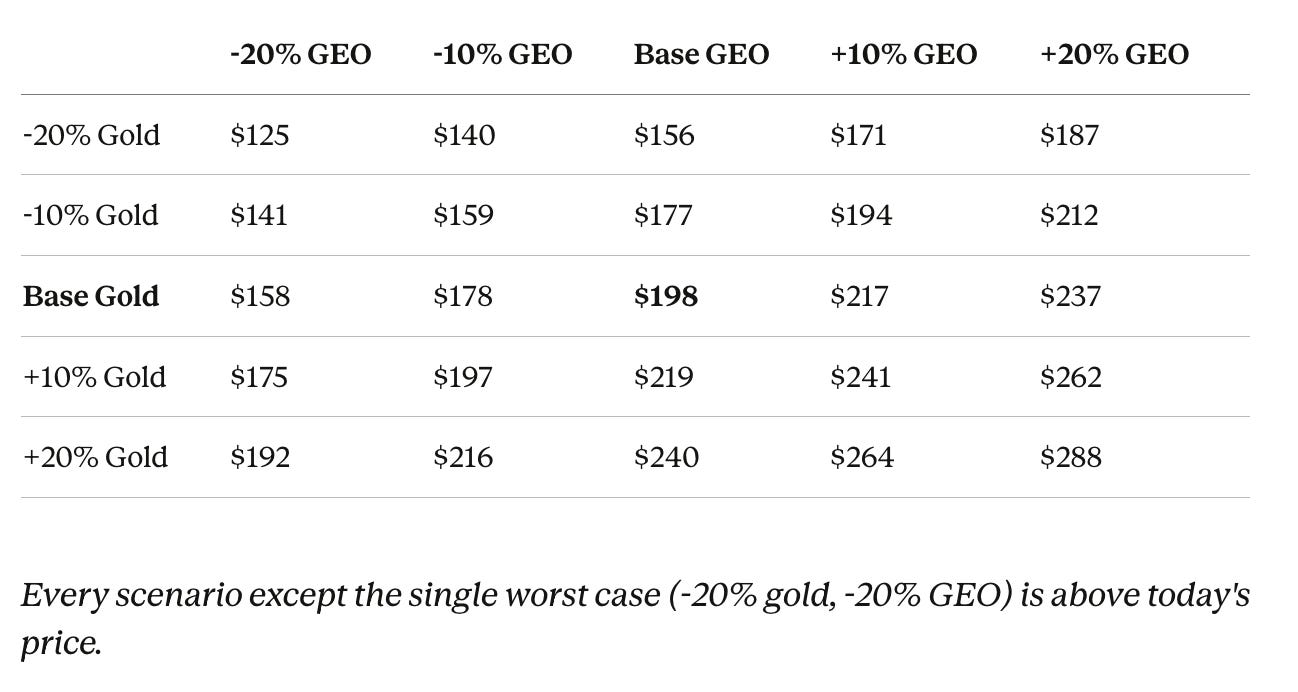

Sensitivity Analysis

Price target (US$/share) across a range of gold price and GEO production outcomes. Base case sits at centre.

Primary Upside Drivers at US$6,000/oz Gold

Margin expansion. Incremental revenue at higher gold prices flows almost entirely to free cash flow due to fixed streaming delivery costs. Operating leverage is exceptional.

Production growth to 1.2M GEOs by 2030 supported by Antamina expansion, Blackwater, Platreef, Goose, and other pipeline assets — approximately 50% growth from current levels.

Silver outperformance. WPM’s ~33% silver revenue exposure means a rising gold/silver ratio reversal — typical in late-cycle precious metals bull markets — would provide a meaningful GEO and revenue tailwind above and beyond gold price gains alone.

Accretive stream acquisitions. A high-gold-price environment creates opportunities for WPM to deploy capital into new streams at attractive terms.

Market re-rating. As the market recognises significantly higher intrinsic value, P/PT compression reverses i.e the same re-rating dynamic that has defined every previous precious metals bull cycle.

Investment Considerations

Key Risks

Production shortfalls or delays at partner mines

Short-term gold price volatility (mitigated by bullish outlook)

Minor dilution from future stream acquisitions (historically low impact)

Premium valuation vs peers limits downside margin of safety

The Royalty King’s Remarks

WPM currently trades at a meaningful discount to the modeled price target. Buying at today’s price of US$124.70 and reaching the base case price target of US$197.70 by end-2030 implies an annualised rate of return of 11.1% per annum ex-dividend, while the higest success mode modeled implies ~19% ARR.

In a US$6,000/oz gold environment by 2029, WPM offers compelling re-rating potential as the market is forced to mark up intrinsic value. The combination of production growth to 1.2M GEOs, sector-leading margins, and no operational risk makes this a core holding for my expressing a long-term bullish view on gold.

WPM is a high-conviction way to capture upside from sustained higher gold prices with lower volatility than direct mining investments. It is a core holding in both the Crassus Investments & Royalty King portfolio.

Want More Leverage on This Thesis?

If you want to go beyond the stock and access the options trades I have on WPM including: specific strikes, expiries, and position sizing, that level of detail is available inside Machina Capitalis. Members get my live options book, real-time trade alerts, and monthly strategy calls covering royalty and streaming positions across the portfolio.

Until Next Time,

— Benjamin

This is an illustrative price target. Not financial advice. For paid subscribers only.

General Disclaimer: This document is an illustrative scenario-based price target using a 5-year DCF and exit multiples. It is not a full life-of-mine model and does not capture out-of-the-money optionality value. All figures are estimates only. Actual results will vary with realised production, metal prices, new stream acquisitions, and market discount rates.

Not Financial Product Advice (ASIC): The Royalty King and its publications do not constitute financial product advice as defined under the Corporations Act 2001 (Cth). The information contained herein is general in nature and has been prepared without taking into account your individual investment objectives, financial situation, or particular needs. The Royalty King does not hold an Australian Financial Services Licence (AFSL). Before making any investment decision, seek independent financial, legal, and taxation advice from a licensed AFS licensee.

Conflicts of Interest: The author may hold a direct or indirect interest in securities mentioned in this document, including Wheaton Precious Metals Corp (WPM). This does not constitute a recommendation to buy or sell.