Dundee corp - 55 Cents on the Dollar

Walter Schloss, the fall and rise of the House of Goodman, and why Dundee Corporation is buying its own stock at half price | TRK research

In Proud partnership with The Solstice Laboratory — the physics of markets, quantified. Read The Entropy Trap to discover what physics knows the economics doesn’t.

“…He knows how to identify securities that sell at considerably less than their value to a private owner… He simply says, if a business is worth a dollar and I can buy it for 40 cents, something good may happen to me. And he does it over and over and over again.”

—Warren Buffet on Walter Schloss

All the disciples of Benjamin Graham agree that his central investing tenant could be boiled down to buying $1 of value for a lot less than $1. While they all differed slightly in their applying of his ideas, the common starting point was a prospective investment’s balance sheet — an analysis of which could determine whether something might be trading at less than its book value (BV) calculated simply as:

Assets - liabilities.

For one disciple in particular, Walter Schloss, this was often where the analysis ended. He famously paid little respect to earnings, very much in contrast to The Oracle Of Omaha yet he went on to boast one of the best records on Wall St and amongst his group of Graham-Newman alumni.

His approach was so simple, yet he outperformed the index over the spans of decades and put up over 30% annually during the vicious inflationary decade of the 1970s. As he saw the world:

“…those companies with large book values in relation to market prices offer the stock holder the greatest rewards…”

The rise of value investing’s popularity has meant that ex-Japan, there really aren’t many, if any true net-net opportunities available in public markets and this has been the case for some time. There are however, some attractive opportunities to buy high quality at a discount to its BV.

Where Net-Nets are really more of a short term liquidation strategy focused on buying opportunities for less than their net current assets, book value takes into account the longer term assets like property, plant and equipment and future projects that, whilst current non-cash generating, will eventually contribute to company earnings.

I actually consider the discount-book approach a superior approach as it’s simpler to perform and is far less reliant on a liquidation event or inflection catalyst in earnings. When applied to companies with no net debt and an ability to grow the business’ book value, a patient investor can expect to earn a healthy rate of return over time. A proven example is Urbana Corp which I wrote about recently

At time of writing, I find myself in the rather unusual position whereby 3 of my largest holdings currently trade at at a significant discount to their Book Value (BV) and have no net debt and produce cash.

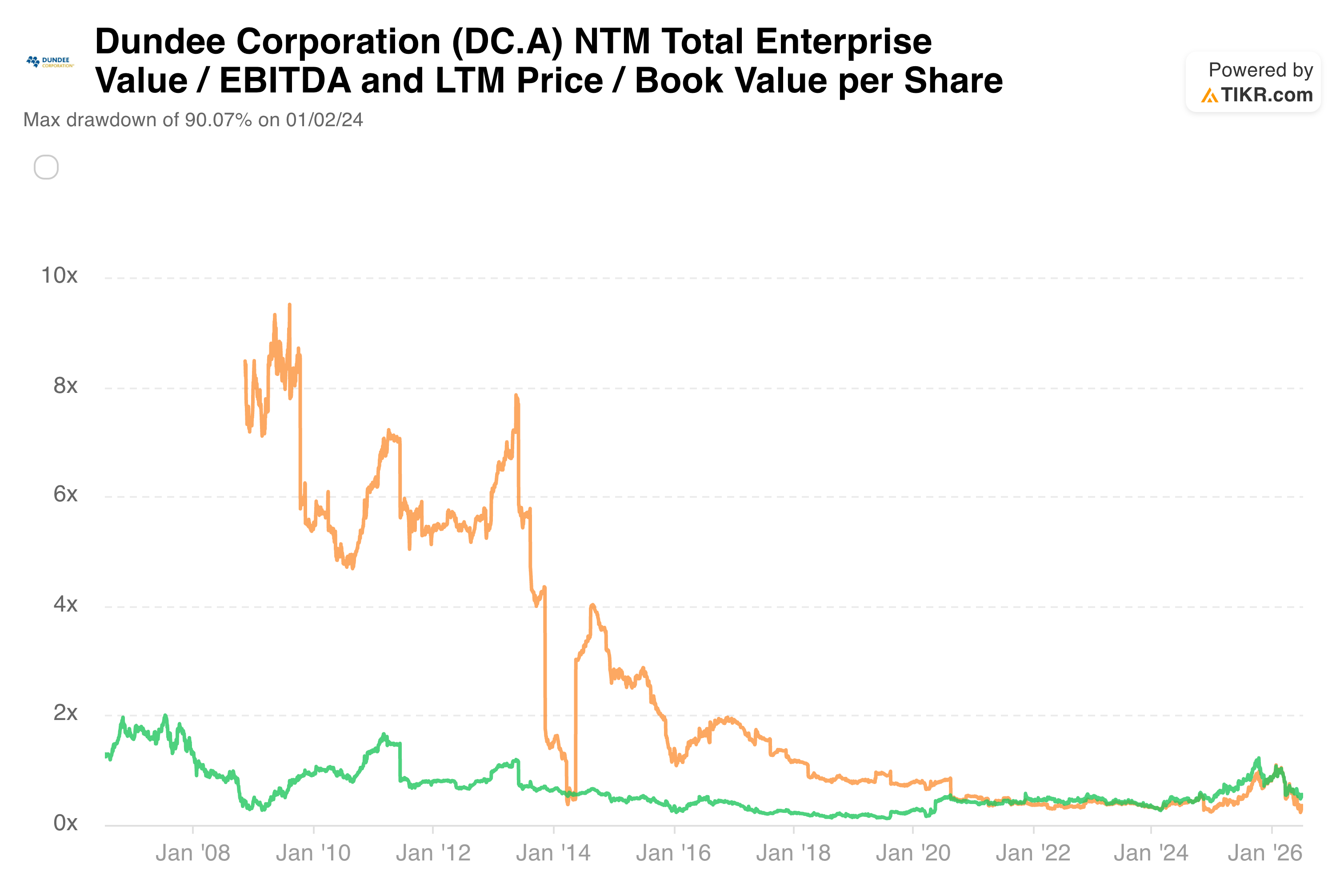

These 3 musketeers are: FRMO, Urbana and Dundee Corporation (DCA) which is the focus of today’s piece and is currently trading at less than half its book value and less than half its 2026 EBITDA!!

HISTORY

To understand why Dundee trades where it does, one must understand what the name meant in 2011 and how it had been considerable hampered by 2019.

The rise.

Ned Goodman was a Montreal kid who trained as a geologist before adding an MBA and a CFA, a combination that basically didn't exist in 1960s, which became his edge: he could read a drill report and a balance sheet.

In 1967 he co-founded Beutel, Goodman & Company from which an impressive amount of talent sprung: namely Seymour Schulich of Franco-Nevada fame. Ned’s big breakthrough came via financing International Corona Resources, the junior that drilled off the Hemlo gold camp in Ontario in the early 1980s and then spent most of a decade in what would became a legendary litigation case LAC Minerals v. Corona. Interestingly, Corona won the Williams mine back from LAC on a breach-of-confidence claim that's still taught in law schools today.

Fast-forward to 1991 and Corona was organized into a vehicle named Dundee Bank Corp. Through the 1990s and 2000s the crown jewel was DundeeWealth, the public wrapper around Dynamic. Dynamic in the late 2000s was arguably the hottest fund family in Canada with one of Ned’s sons, David, running it.

In 2007 the Bank of Canada was caught holding asset-backed commercial paper and had to be sold to Scotiabank in the crisis yet in late 2010 Scotia bought all of DundeeWealth in a deal worth roughly $2.3 billion and closed in early 2011. Dundee Corporation walked away with a mountain of cash and Scotia paper, plus it retained a piece of: Dundee Realty (which became DREAM) Dundee Capital Markets, and the Dundee Precious Metals position that Jonathan Goodman (another son) had converted from a closed-end fund into an actual operating gold miner.

Ned at that point was routinely called Canada's Buffett, had a business school named after him at Brock, and had roughly a billion dollars of redeployable capital and total credibility. It’s unlikely he knew it at the time, but this was to be the zenith.

The fall.

Ned had a macro conviction: fiat debasement, the death of the US dollar, hard asset inflation (sound familiar?) etc. Post-2011 he allocated heavily but into operating businesses in fields outside his original specialty in mining + finance. Dundee bought into numerous and varied businesses, which included: Casinos, agriculture, hydrocarbon exploration and even biotechnology just to name a few. At one point the org chart had something like a hundred entities.

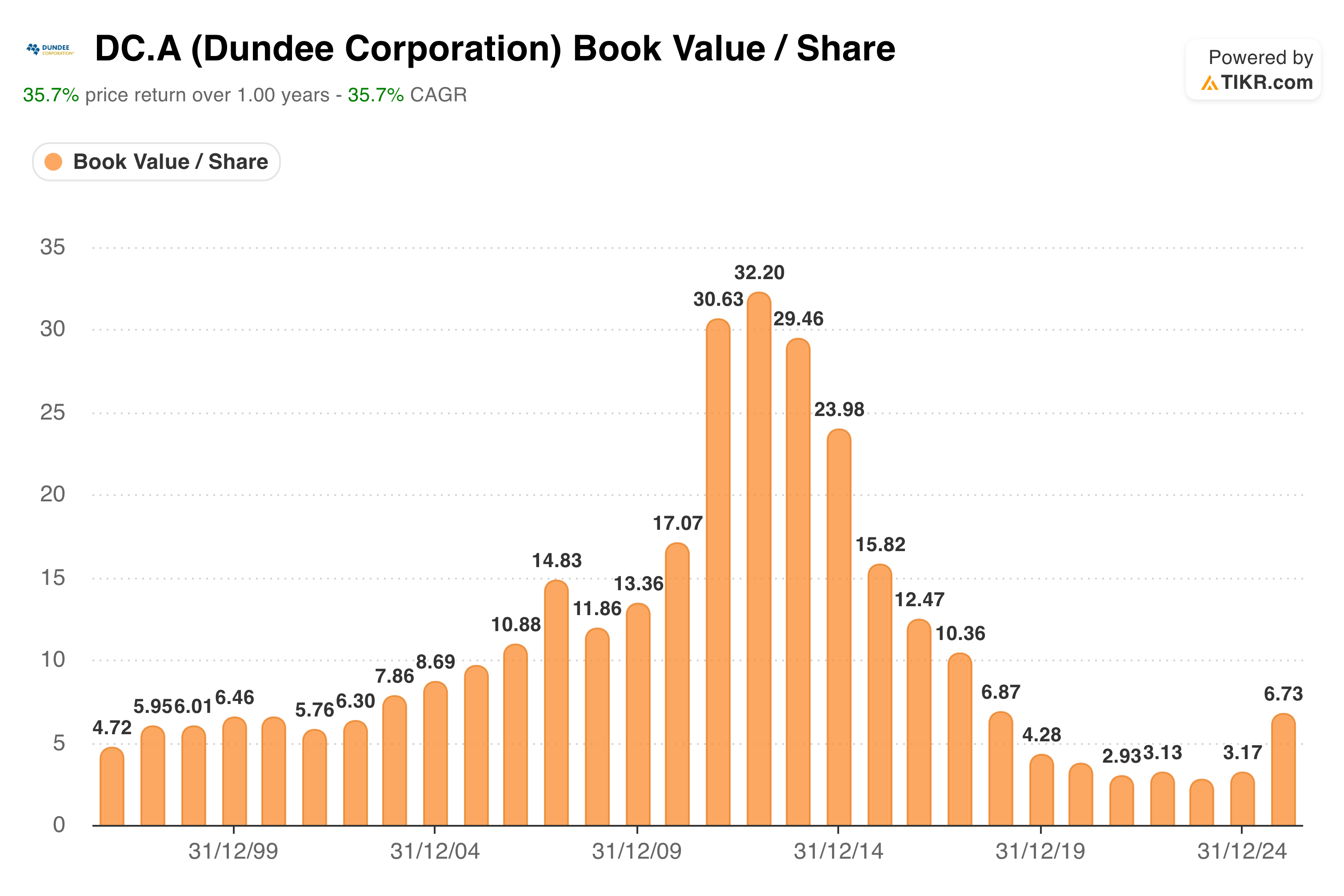

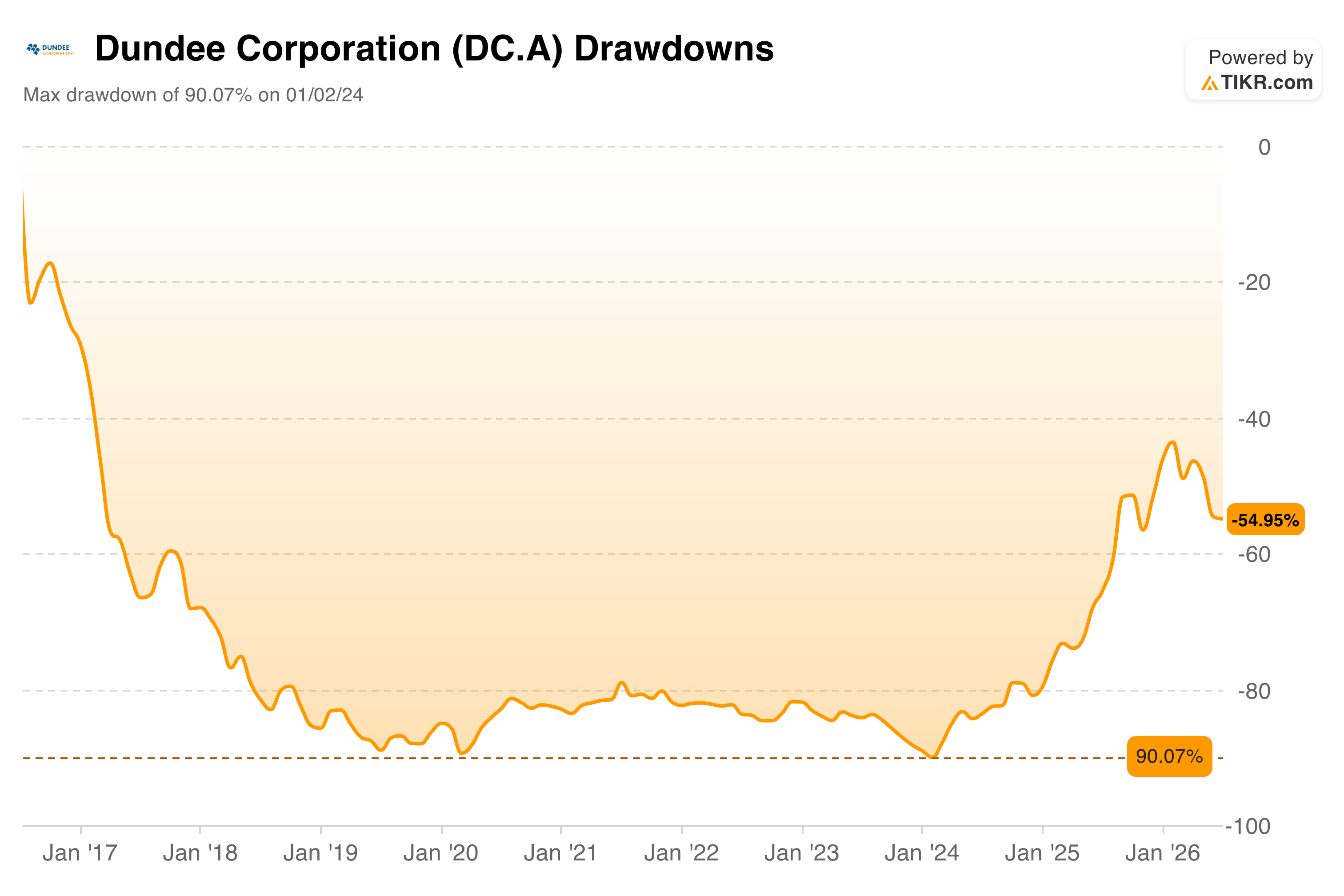

Having tempted fate, almost all of it went wrong at once. The businesses consumed capital, management attention was spread across industries nobody had experience in, and the 2014–15 commodity bear market hit the resource book simultaneously. Ned's health forced him to step back around 2013–14; David took the CEO chair and initiated an unwinding of the assets. Book value, which had been in the high teens per share, ground down toward the low single digits; the stock, which traded north of C$17 in 2014, bottomed under a dollar by 2019–20.

Ned died in August 2022, and the obituaries had to hold both truths: one of the greatest capital allocators Canada ever produced, with a final act that destroyed most of a fortune. I can’t help but re-iterate the importance of business models here as it appears the good times at Dundee coincided with financing mines — the bad with operating them.

Don’t Call It A Come-Back — The rebound.

Jonathan Goodman was named CEO in 2018 and he channeled his inner Javier Milei by ruthlessly cutting anything the was non-core Afuera!

The last of the failed ventures was finally sold in 2025 and now the company resembles that of the ‘90s. Which is why I’m now interested and invested.

The balance sheet is now clean, the company is earning again from core operations. There’s still time for a rebound to end the decade successfully, the question is, can Jonathan rise to the occasion and seal victory like Enzo Fernandez did two days ago for Argentina in the world cup?

Valuation

Uncle Rick is a long term friend and co-investor with the Goodmans and he taught me that the easiest money to be made is when something goes from being hated, to merely tolerated.

The base investment case therefore would be DCA simply re-rating to fair value of its assets, implying a 100% upside from today’s price of $3.61 CA.

The more interesting question is, what might it be worth in success mode?

This is very much a Walter Schloss situation.

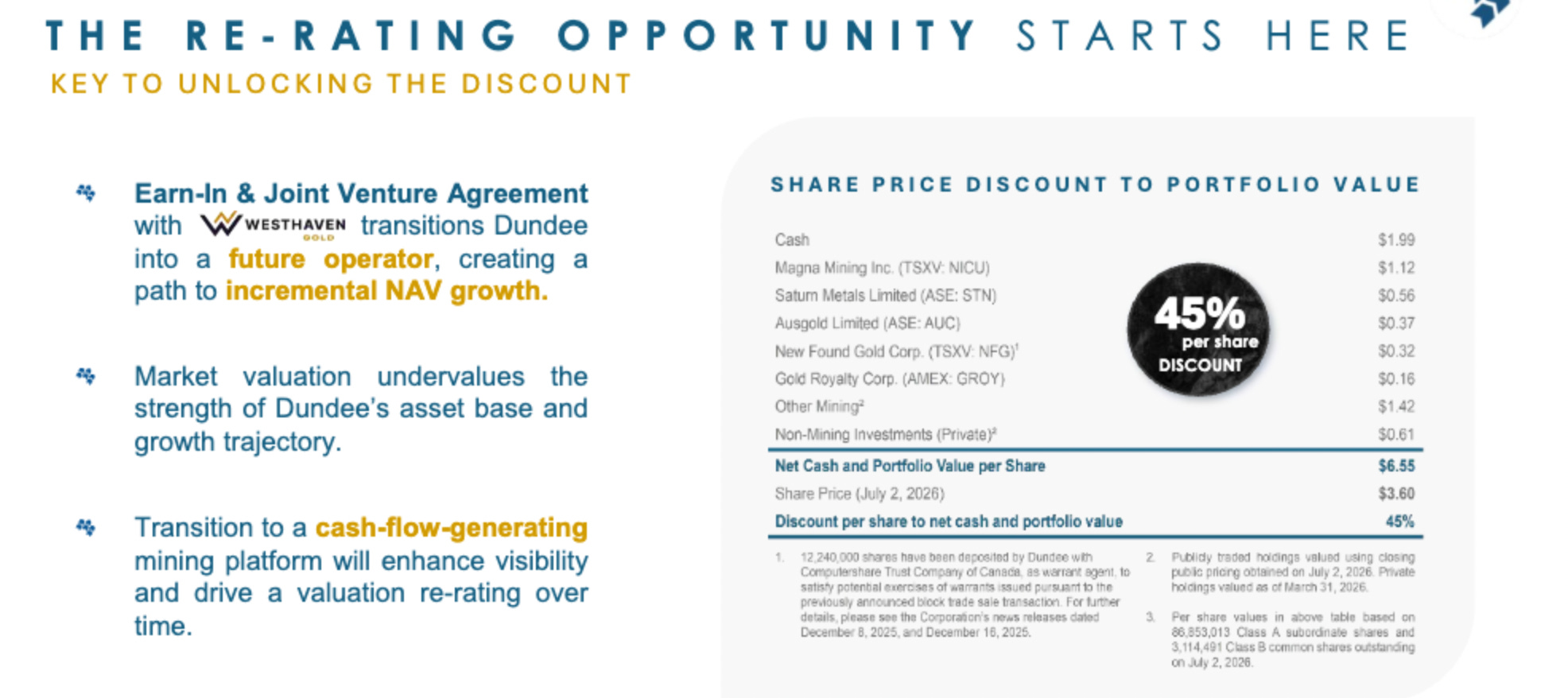

The company holds approximately C$194 million in cash. Its portfolio of mining equities are a mix of public and private assets purportedly worth ~$6.55 per share.

Against a C$3.61 price, that is 55 cents on the dollar.

The floor. Roughly C$2 per share of the C$6.30 is cash. That is the sub-basement. For the shares to be worth less than that, management would need to spend the cash destroying value — which is precisely what the old Dundee did and precisely what the new one has spent seven years proving it will not.

The base case requires no imagination at all: the assets are simply worth what they are stated to be worth, the discount closes, and the shares double. I do not need the discount to close to be interested, but it is worth being honest that this is the entire base case — a re-rating, nothing more.

Success mode is where it gets interesting, because there are three engines and they compound on each other.

The first driver is the buyback. Every share Dundee retires at C$3.61 removes a C$6.30 claim from the register, roughly C$2.70 of value transferred, silently and permanently, to the holders who remain. The company is doing to its own stock what Walter Schloss did to the market for five decades: buying dollars for half price, over and over and over again.

The second is the portfolio developing. Magna faces a Levack restart decision in the second half of this year. Saturn's Apollo Hill and Ausgold's Katanning are both marching toward development milestones. New Found Gold is ramping up. None of these need to work for the base case. Any of them working feeds the third engine which is growth of the assets leading to compounding of the BV.

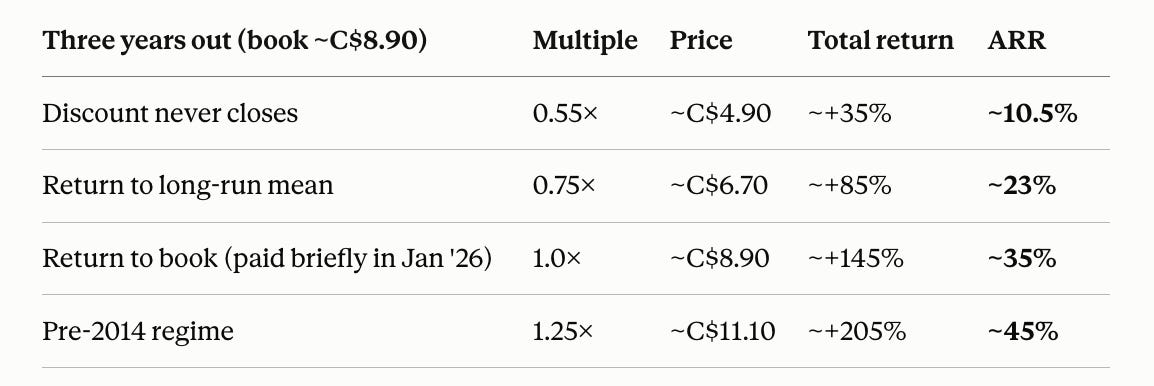

Putting modest numbers together. Suppose book value compounds at 12% for three years and buybacks alone contribute half of that, so this assumes only mild success from the portfolio. Book reaches roughly C$8.90 per share near the decade’s end.

Remarkably, if the market never changes its mind and DCA remains hated yet continues to execute well, the combination of buybacks and portfolio compounding still produces a double-digit annual return. The re-rating is a kicker, not the cornerstone of the thesis.

Schloss paid little attention to earnings, held no meetings with management and really only cared about a large book value in relation to the market price, a clean balance sheet, and time. Dundee today offers all three: 57 cents on the dollar, no debt at the parent, and a management whose principal capital-allocation activity is exploiting the very discount you would be buying. If a business is worth a dollar and I can buy it for 57 cents, while the company itself buys alongside me at the same price, something good may happen to me.

I hope it happens more than once.

Until next time.

— Benjamin

PS: I write this publication for readers willing to look past a twelve-month clock. The best way to find more of them is through you. So this month, one reader will receive a free 12-month premium subscription simply for sharing this piece. If the winner is a current subscriber, their subscription will be comp’d for a year.

How to enter — each action counts as one separate entry:

Restack this dispatch on Substack Notes

Share it on Notes with a comment — a line on what stood out, agreement, disagreement, all valid

Quote-share on X, tagging @TheRoyaltyKing

Disclaimer: This publication is intended solely for documenting my personal journey with trading and investments for income and travel purposes. I am not a certified financial advisor nor am I a financial professional and none of the content provided should be construed as investment advice. It is essential to conduct your own thorough research and consult a registered financial service provider for appropriate guidance. I cannot guarantee the accuracy or completeness of the information presented. Any actions taken based on the information shared in any of my work are done at your own risk and discretion. The author may hold positions in the assets mentioned.