Hawaiian Electric: The Yield on the Far Side of Patience

An Updated Valuation | The Royalty King Report 01/07/2027

In Proud partnership with The Solstice Laboratory — the physics of markets, quantified. Read The Entropy Trap to discover what physics knows the economics doesn’t.

The Royalty King Report

Hawaiin Electric Industries Inc | HE

The Investment Case Recapped.

The setup in HE provides a rare chance to own a perpetual asset which enjoys a monopoly position providing electric power to the state of Hawaii at a double digit yield on cost for the patient investor.

Such an opportunity has only presented itself as a result of the Maui wildfire disaster in 2023 which, long-story-short, resulted in HE settling to pay $1.99 Billion and its stock tanking in reaction to the news.

The reader can get up to speed here:

What’s New Since Then?

A good deal, and nearly all of it positive. In April 2026 the company made the first of four equal annual payments of roughly $479 million and the rating agencies noticed: Moody's lifted the utility’s credit to Ba1 and the holding company to Ba2, one notch below investment grade.

More important for what the business earns, the company filed a rate rebasing in March 2026 which should add $170 million of additional annual revenue, a 5.3% consolidated increase phased across 2027 and 2028 and then locked to 2032. Simply put: rebasing here refers to an increase on the equity base on which HE can earn its allowed return - think of it as an increase in total potential future revenue base.

The quarter’s return on rate base was softer, coming in at 6.5% vs its allowed max of 9.5% but overall the story is turning ever more positively.

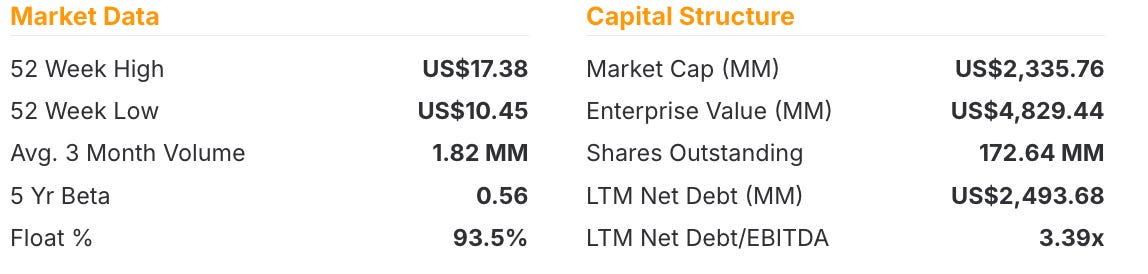

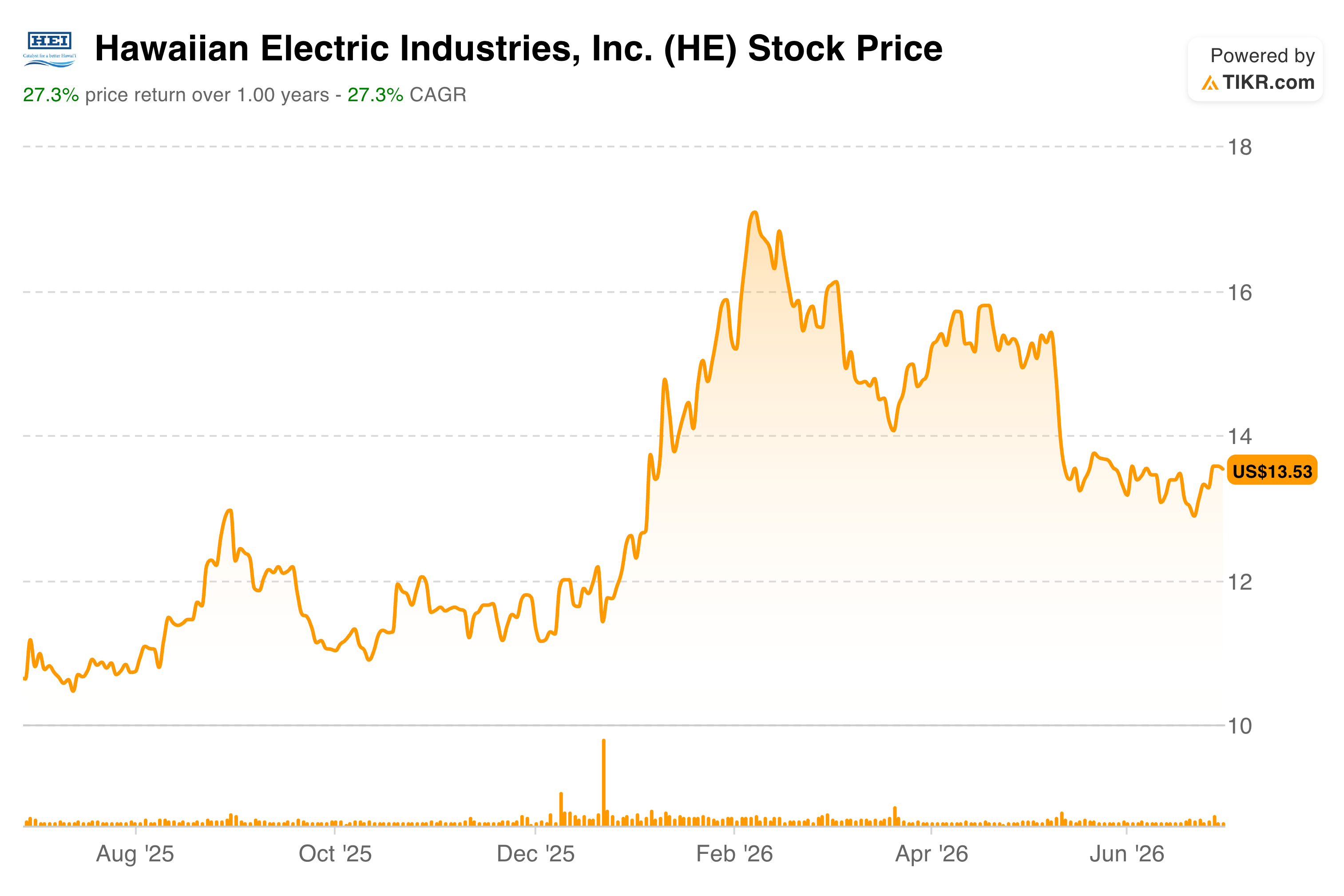

In fact, readers might be surprised to learn that HE’s stock price has actually risen over 27% on a year-on-rear basis.

A note before we continue: this month I'm comping one reader a full 12-month premium subscription. Entry is simple — restack this article, or share it on Notes or X. Every share is an entry. Full mechanics at the bottom of the piece.

Macro - Economic Considerations

A strong dollar — which I expect in the short term— tightens conditions worldwide and hits the big, low-yielding names hardest. The broad market looks expensive, yields are near lifetime lows.

So where to hide? In something boring and cash-generative, with customers who show up no matter what. A regulated utility fits: in a downturn people delay certain purchases but they don’t unplug from the grid. The catch is that the payoff in this case is deferred. HE pays nothing today. It’s a high-yield idea whose toll is patience, not dollars. That’s the whole thesis and not only is it insulated from a weak economy but also from inflation as it has a regulated allowed return on equity which enables it to pass-through any increase in its input cost (which is largely diesel) for power generation.

Monopoly Moat

Hawaiian Electric supplies about 95% of the state's electricity across grids that are physically isolated island by island; there’s no neighbouring utility to import from, no way to replicate the wires, no way to abandon them. This enviable position is why I refer to their assets as perpetual because they would remain of the utmost strategic importance even in the event of a bankruptcy. A litigation cloud is a thing that lifts. A monopoly is a thing that does not. Looking past the fog of the near term and valuing the opportunity looking 3-5 years out is the modus operandi. It’s easier to visualise the opportunity through the looking-glass of the equity yield curve.

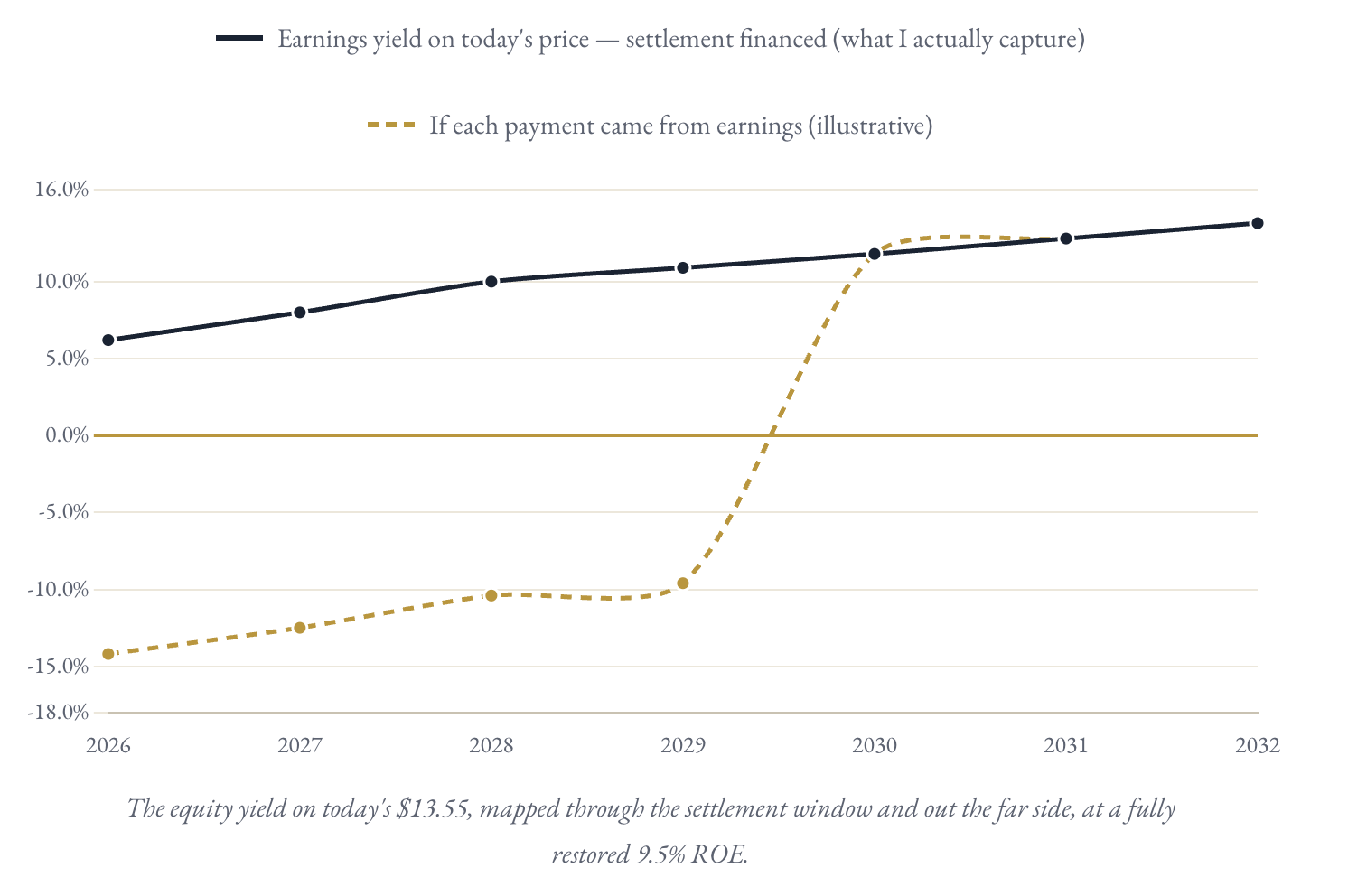

The Equity Yield Curve

The idea is elegant: Just as the bond market has a yield curve that ordinarily slopes upward, paying you more for the risk of a longer wait, so too does equity — only the equity curve is far steeper. Go out three years+ and you routinely find implied rates of return of 30% and beyond. Why should that be? Because the professionals who run most of the world's money are judged on a twelve-month clock. A reward that is four years away, to those managers, has little utility because it will not feature into the calculation of their yearly bonuses. The equity yield curve is simply a picture of that collective aversion to time. It is a map of the discount the crowd hands you for being willing to wait when they are not. Hawaiian Electric’s peculiar regulated returns and knowable rate base makes it a good candidate to run through the equity yield curve lens.

So let me draw the curve for HE specifically, underwriting the utility at its full allowed 9.5% return on equity and updated rate base. The four settlement instalments run through April 2029; the last one clears, and the curve inflects.