Miami International Holdings - Many Happy Returns

Reviewing A Main Holding In The Croupier Collection

Don’t forget to grab your ticket to the Rule Symposium below.

*Author’s note* Newer readers can get up to speed on the thesis behind my launching a seperate portfolio for financial exchanges and like businesses under the section ‘The Croupier Collection’ (TCC) in the home page. This whitepaper I wrote with Hugo Navarro is recommended reading.

The Croupier Collection is built on the premise that the best long-duration equity is a business that: earns a toll on human financial activity, is indifferent to direction, structurally sticky, and capable of compounding that toll as the underlying activity grows. By this framework, MIAX is an excellent candidate.

Executive Summary

MIAX is a multi-asset exchange operator. It earns a toll on every options contract, futures trade, and equity transaction that crosses its platform. It operates a variety of U.S. options exchanges, a futures exchange and clearing house, the Bermuda Stock Exchange, and — here’s one most have never heard of — The International Stock Exchange in Guernsey.

I bought Miami International Holdings (MIAX) direct stock, adding to my inderect ownership through various private partnerships, around its IPO in August 2025 at $23.00. I continued to add to my position over the following months, bringing my average cost basis to approximately $30.00. At the current price of ~$52.78, that’s a 76% unrealised gain in under a year acroos the holdings in Crassus Investments and TCC.

This belongs in the Croupier Collection for the same reason the CME Group and CBOE et al. are represented: the house always gets paid.

The differentiating factor relative to mature peers (CME, Cboe, ICE) is timing. MIAX is at the stage CME was in the early 2000s in terms of its growth runway. Investors who bought CME in 2003 at equivalent growth-adjusted multiples generated 70× returns over the last 23 years.

Compared the SPX index which went ~10.6x over the same period and one can’t help but be astonished that an unsung asset class could trounce what is commonly considered the economic bell-weather, sporting an alpha of 9.4% of annualised performance and yet witness such alpha be almost ubiquitously ignored by the broader investing public.

Interestingly, in the case of MIAX it appears that they are gaining market share against the incumbents.

Today’s piece is intended to be an informal commentary on earnings with a full valuation update available for premium members.

Q1 2026 Earnings - TheRoyalty King’s Remarks

Gross revenues grew 13%. Cost of revenues grew 2.5%. Operating income more than doubled. That is the exchange model working exactly as designed.

The keys to this model are volume, product proliferation and market share.

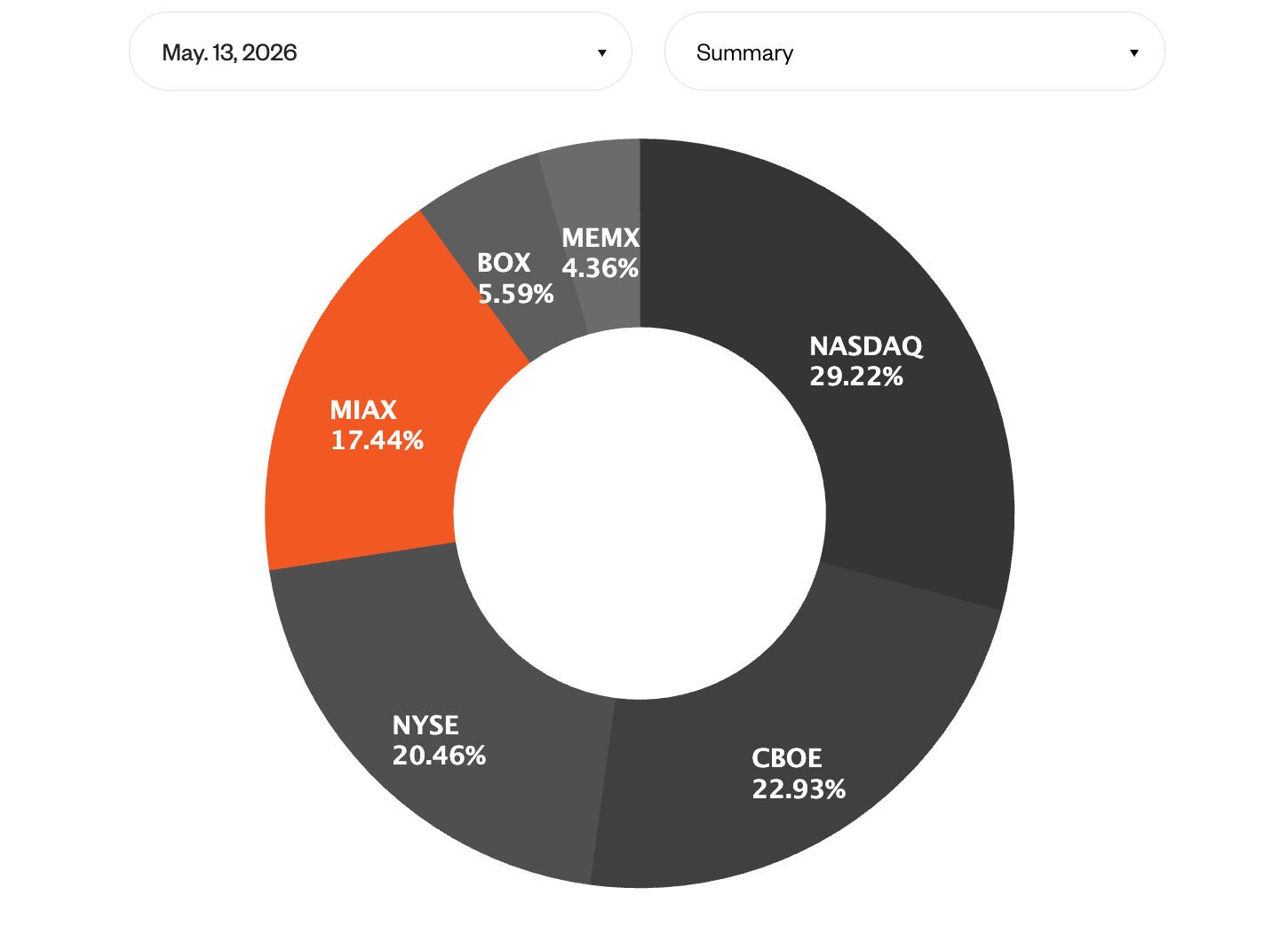

The increase in net-sales was primarily driven by their strong and growing options franchise with MIAX now holding over 17% of the US options market at time of writing.

MIAX options reached anaverage daily volume of 10.9 million contracts in the first quarter of 2026, a 26.6% year-over-year (YoY) increase!

Another noteworthy occurrence was the 90% sale of MIAXdx in January to a JV initiative of Robinhood Markets. Retaining 10% of the equity reminds me of a classic move out of the prospect-generator model.

Watch out for the addition of the Bloomberg index and its associated derivatives which shall be hosted on MIAX and promises to be a potential boon for the company.

All in all, MIAX showed revenue growth, margin expansion and market share gain and I couldn’t be happier with their performance since coming public.

Valuation

Given MIAX’s blistering entry onto the scene as the American exchange with the most growth potential on its — for now— small Market Capitalisation, what might a future share of MIAX be worth?